In the AI era, CPUs, long overshadowed by GPUs, may be quietly embracing an explosive growth cycle of their own.

According to Zhuifeng Trading Platform, on May 5, UBS Global Research released an in-depth research report covering the U.S. semiconductor industry. Faced with intensive investor inquiries regarding how agentic AI will impact the server CPU market, analyst Timothy Arcuri and his team conducted extensive industry expert interviews, combined with bottom-up and top-down dual analytical models, and drew a clear conclusion:

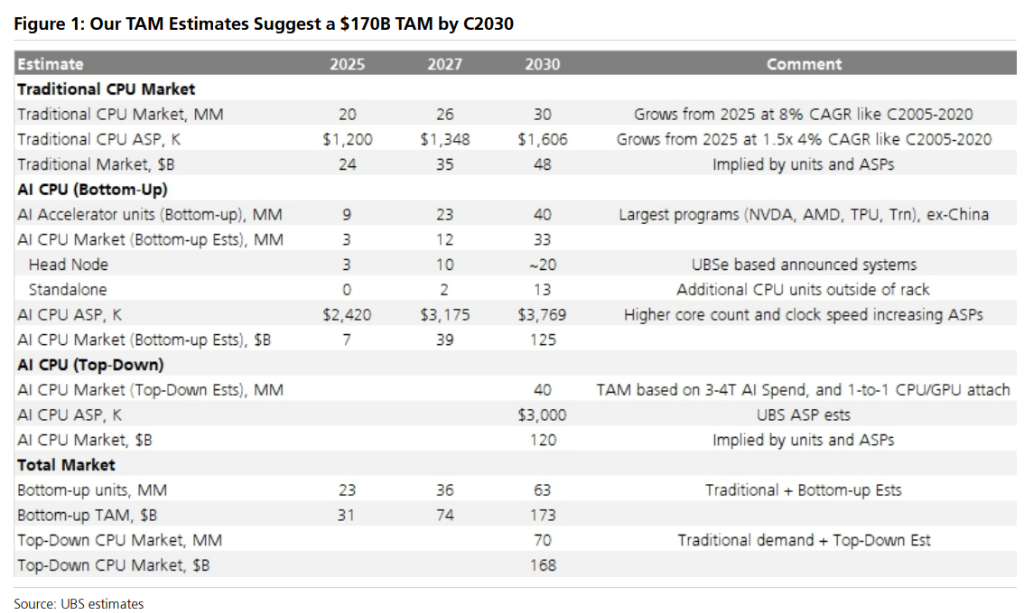

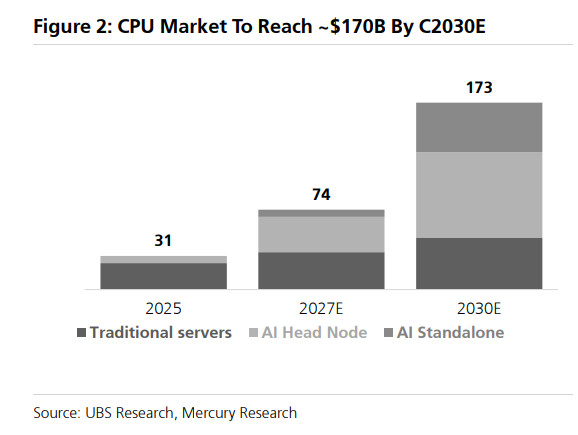

The market has severely underestimated the value of CPUs in the AI era. The Total Addressable Market (TAM) for server CPUs is projected to grow from approximately $30 billion in 2025 to around $170 billion by 2030, representing a nearly fivefold increase over five years.

Over the past two years of the AI boom, GPUs have seized all the limelight. However, as AI evolves from simple conversational generation to task-autonomous Agents, the computing power bottleneck is quietly shifting.

Agentic AI Reshapes Computing Landscape: From GPU Dominance to CPU Revival

To understand the breakout of the CPU market, it is essential to distinguish the workload differences between agentic AI and traditional AI.

In traditional AI training and basic inference phases, GPUs have been the absolute mainstream. If we liken AI computing power to a factory, GPUs are the tireless workers on the production line, while CPUs act as managers responsible for task allocation. Under the traditional model, a single CPU manager can easily oversee multiple GPU workers.

Agentic AI has rewritten the rules of the game. Beyond text generation, agentic AI undertakes task orchestration, tool invocation (such as code execution in sandbox virtual machines), file retrieval and more. This has led to an exponential surge in workload for CPUs.

Analysts obtained striking data from industry expert interviews:

Shift in Workload Focus: Industry experts pointed out, "Traditional AI workloads allocate 70%-80% of computing resources to GPU-based inference; in agentic AI inference, the ratio is reversed, with 70%-80% of workloads shifting to CPUs."

Sharp Rise in Core Allocation: In conventional AI training, each GPU is typically paired with only 8-12 CPU cores; basic inference requires 16-24 cores. By contrast, agentic AI demands 80-120 CPU cores per GPU. This means that for the same GPU, the required CPU core count in AI Agent scenarios is 5 to 10 times that of traditional training scenarios.

Pressure from Concurrent Tasks: "A single Agent and its derived sub-Agents may occupy 1-4 CPU cores, and a single complex task can generate 10 to 100 sub-Agents."

This fundamental logical shift has broken the previous computing architecture of prioritizing GPUs over CPUs, unlocking enormous incremental space for the CPU market.

A Massive $170 Billion Market

Based on the above logic, the brokerage’s analysts re-estimated the overall TAM of the server CPU market. The result indicates the market will reach approximately $170 billion by 2030.

How is this massive figure calculated? Analysts adopted two cross-verification methods: bottom-up and top-down.

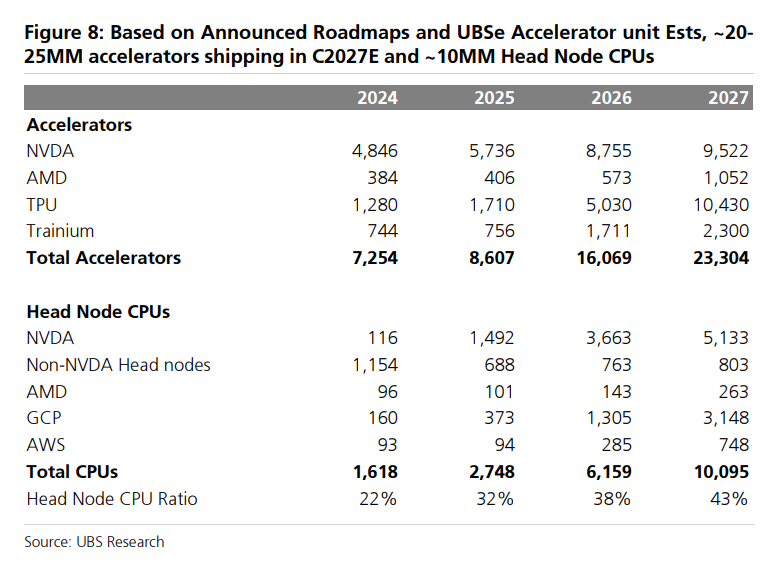

Bottom-up Estimation: Based on accelerator model forecasts from U.S. hyperscale cloud providers, around 23 million accelerators (XPU) and 10 million head node CPUs will ship globally by 2027. Driven by the development of agentic AI, accelerator shipments will rise to roughly 40 million units by 2030.

More importantly, the CPU-to-GPU ratio will gradually converge from the current 1:4 to 1:2 or even 1:1. In addition, AI applications demand chips with higher core counts and higher frequencies, driving a notable increase in Average Selling Price (ASP) of AI CPUs. For instance, NVIDIA’s 144-core Grace CPU is priced between $3,000 and $4,000. Driven by rising both volume and price, the AI CPU market alone will scale up to $125 billion.

Top-down Estimation: Analysts referenced NVIDIA’s forecast that the overall AI TAM will range from $3 trillion to $4 trillion by 2030. It is estimated that around 40 million XPUs will ship in 2030. Assuming the average ASP per XPU rises to $3,000, coupled with a CPU-to-GPU ratio of 1:1 or 2:1, the AI CPU market is projected to range from $120 billion to $200 billion, consistent with the bottom-up projection.

Analysts divide the future CPU market into three core segments:

Traditional Server Market: Maintaining steady growth, with annual shipments expected to reach around 44 million units by 2030.

AI Head Nodes: Bundled with GPU racks, primarily responsible for task orchestration and optimizing GPU utilization efficiency.

Standalone AI Racks: Pure CPU servers dedicated to tool invocation and sub-Agent concurrent task processing for agentic AI.

The market pie is expanding rapidly, and the core focus lies in market share allocation.

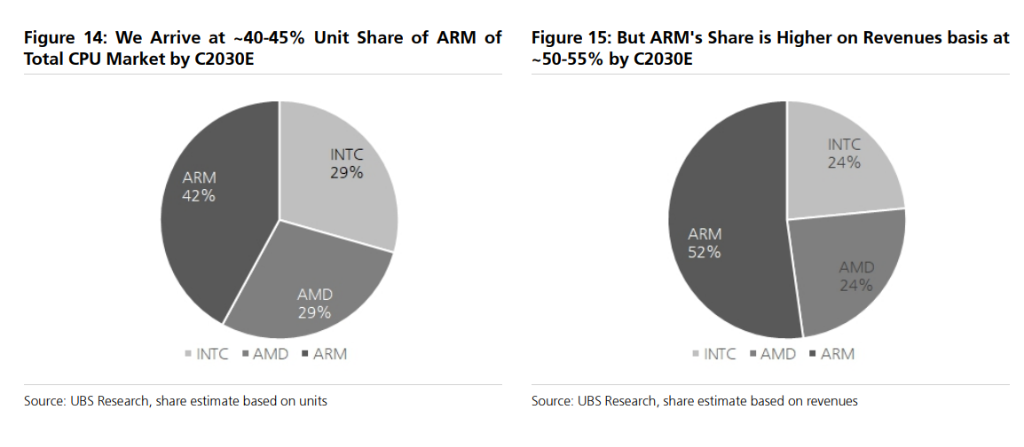

Analysts clearly ranked the players: ARM stands as the biggest beneficiary in the server CPU sector, followed by AMD, then Intel — with all three vendors set to benefit from industry growth.

ARM: Market Share to Surge from 15% to 40%-45%

In 2025, ARM architecture holds approximately 15% unit share in the server CPU market. The report forecasts the figure will climb to 40%-45% by 2030. In revenue terms, thanks to the higher ASP of high-end AI CPUs, ARM’s revenue market share will further reach 50%-55%.

What underpins ARM’s competitive edge?

Citing industry experts, ARM architecture delivers around 30% higher power efficiency and 20%-30% higher memory efficiency, with a compact core design offering clear advantages in latency and cost. Most crucially, self-developed CPUs from leading hyperscale cloud players including NVIDIA Grace, AWS Graviton 5 (192-core) and Google almost universally adopt the ARM architecture.

The brokerage estimates ARM will capture over 75% share of the AI head node CPU market by 2030.

Nevertheless, ARM still faces shortcomings. The report notes ARM is traditionally a single-threaded architecture, with Simultaneous Multi-Threading (SMT) capabilities only gradually developed in recent years. High core count scenarios still suffer from core interference and software compatibility challenges. Furthermore, ecosystem maturity remains to be improved, with full optimization of certain software stacks expected around 2028.

Based on the above assessment, analysts raised ARM’s 12-month target price from $175 to $245. As of May 4, the trading day before the report release, ARM closed at $203.26, maintaining a Buy rating.

AMD: High Core Count & Multi-Threading, the Ideal AI Partner

AMD’s strengths lie in high core count design and robust multi-threading performance, which perfectly match the dual demand of AI Agents for both high speed and high throughput.

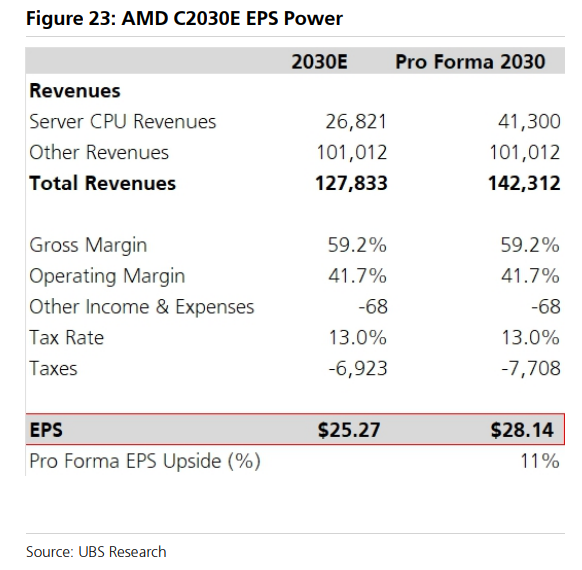

Citing AMD’s Investor Day remarks in November 2025, the company expects the server CPU market to grow from $26 billion in 2025 to approximately $60 billion by 2030, with AI-driven CPUs accounting for roughly 50% of the 2030 market. AMD also targets capturing over 50% of the overall market share.

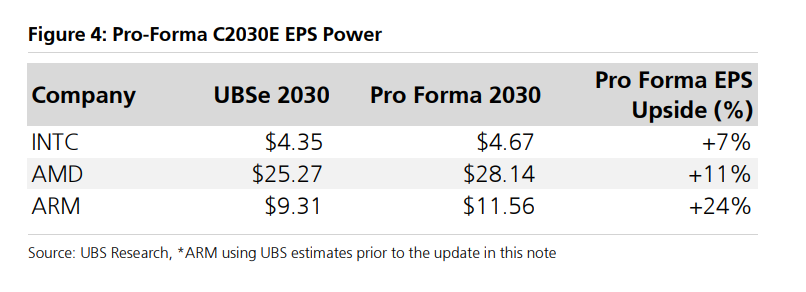

Analysts currently forecast AMD’s Earnings Per Share (EPS) at $25.27 for 2030. If industry development aligns with expectations, the revised 2030 EPS could reach $28.14, implying an upside potential of around 11%.

Intel: Solid Foundation with Mounting Catch-up Pressure

Intel faces a relatively complex market position.

In the traditional server market, the x86 architecture still commands about 85% market share, and Intel retains advantages in specific workloads such as tool invocation and storage optimization. However, in the AI head node segment, Intel’s presence is being rapidly eroded by ARM.

UBS pointed out that Intel is pinning its hopes on the Coral Rapids product line to narrow the gap with AMD and ARM, yet AMD and ARM hold a more favorable market positioning in the high-end AI CPU space for now.

Intel nevertheless possesses a unique growth driver: PC spillover effect. As AI Agents shift more computing tasks to local end devices — a strategy already adopted by Anthropic’s Claude Code — the PC upgrade cycle is set to accelerate, bringing tangible benefits to Intel.

The brokerage estimates Intel’s revised EPS upside potential for 2030 at roughly 7%, the lowest among the three chip giants.

Not All CPUs Are Equal: The Trade-off Between Latency and Throughput

The report further unpacks an easily overlooked detail: AI Agent workloads do not simply favor CPUs with the highest core counts.

Hyperscale cloud providers face a fundamental trade-off in hardware selection:

High Core Count CPUs: Deliver high overall throughput and energy efficiency, but feature lower clock frequencies and higher latency, with limited software scalability to fully utilize hundreds of cores.

Low Core Count & High Frequency CPUs: Boast low latency and fast response, ideal for head node roles in orchestration, scheduling and GPU efficiency optimization.

In real-world deployment, hyperscale cloud vendors widely adopt a layered architecture of head nodes + large-scale compute nodes: head nodes undertake low-latency orchestration and control, while compute nodes execute high-throughput parallel computing tasks.

This means vendors offering a broad SKU portfolio covering diverse core counts, frequencies and power consumption tiers are more competitive than those focusing solely on a single flagship configuration.

UBS also emphasized that cloud hyperscalers prioritize transactions per watt rather than peak performance in procurement decisions, with memory configuration regarded as the top design priority.

Cloud vs Edge: An Unresolved Variable

Analysts also highlighted a key uncertain factor: the division of computing workloads between cloud and edge terminals.

Early AI Agent deployments relied almost entirely on the cloud, yet an increasing number of system architectures are shifting computing workloads to local devices. 5 to 10 parallel tasks can run directly on local files and data, cutting latency and reducing cloud computing costs.

According to expert estimates cited by UBS, the expansion of local edge execution may reduce the CPU capacity required for cloud AI Agent workloads by around 25%.

This implies the multiplier effect of AI Agents on data center CPU demand may narrow from the initial 5-8 times to roughly 4 times. Meanwhile, PC CPU demand will rise synchronously, benefiting both AMD and Intel.