CVX or XOM: Are Either of These Oil Giants a Buy for 2025?

ExxonMobil XOM and Chevron CVX, two giants in the energy world, stand as the cornerstones of the U.S. energy industry, commanding market capitalization of $499 billion and $279 billion, respectively. Their influence is immense, shaping not only the sector but the broader energy landscape.

These titans drive the exploration and production of oil and natural gas, refine and market petroleum products, and lead in chemical manufacturing. Together, they embody the scope and power of energy innovation.

Let’s dive into each company’s strengths and challenges to determine whether either stock is worth adding to your portfolio for 2025.

Stock Performance

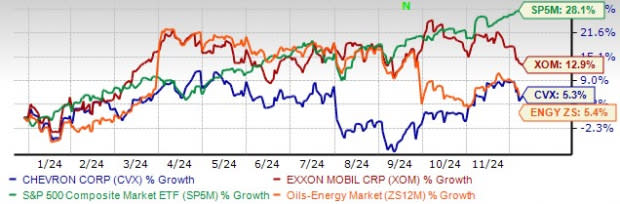

The year so far has tested the resilience of energy giants, and while ExxonMobil and Chevron have both faced headwinds, Chevron has struggled more noticeably. ExxonMobil shares have climbed nearly 13%, significantly outpacing Chevron’s modest 5% rise. However, neither has managed to keep pace with the S&P 500’s impressive 28% surge in 2024, and Chevron’s underperformance extends beyond the broader market, trailing even its sector peers.

XOM, CVX Year-to-Date Stock Performance

Image Source: Zacks Investment Research

Idential Earnings Surprise History

ExxonMobil and Chevron share a comparable track record when it comes to earnings performance, surpassing the Zacks Consensus Estimate in three of the last four quarters while falling short in one. However, ExxonMobil edges ahead with a four-quarter average surprise of 2.9%, standing in contrast to Chevron’s slight dip into negative territory at -0.5%.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Production Growth Amid Challenges

In recent years, ExxonMobil and Chevron have faced mounting challenges in replacing reserves as access to untapped energy resources is increasingly constrained. For companies of their scale, expanding oil and natural gas production has long been a demanding endeavor.

Through the first nine months of 2024, ExxonMobil delivered an impressive 14.4% production growth, averaging 4,243 thousand oil-equivalent barrels per day (MBOE/d), up from 3,709 MBOE/d a year earlier. Meanwhile, Chevron reported a 10% rise in output, reaching 3,334 MBOE/d, fueled by strategic growth initiatives.

ExxonMobil’s surge was powered by its operations in Guyana and the Permian Basin, renowned for its efficiency and cost-effectiveness. Chevron’s uptick reflected contributions from its PDC Energy acquisition, key Gulf of Mexico projects, and a robust Permian Basin performance.

Despite challenges in resource replacement, both companies are leveraging strategic assets to drive production gains.

Valuation

Chevron edges out ExxonMobil in valuation, but the gap isn't vast. With a forward price-to-earnings (P/E) ratio of just over 14, ExxonMobil's shares are priced slightly higher than Chevron's, which hover around a 13X multiple. While both stocks are trading at a premium relative to their subindustry, Exxon's higher valuation makes it more vulnerable to downside risk, especially if energy demand weakens or oil prices remain under pressure.

Image Source: Zacks Investment Research

Consistent Dividend Payers

When it comes to dividends, Chevron and ExxonMobil stand out as powerhouses in the energy sector. These two diversified oil giants boast a remarkable track record, earning their place among the exclusive Dividend Aristocrats — S&P 500 companies that have increased payouts for over 25 consecutive years. Even during the peak pandemic, both firms prioritized maintaining their dividends, cutting costs elsewhere to uphold this commitment.

In February, Chevron increased its dividend by 8% to $1.63 per share ($6.52 annualized), offering investors an attractive yield of approximately 4.15%. Meanwhile, ExxonMobil raised its payout to 99 cents per share ($3.96 annualized) last month, delivering a yield of around 3.51%.

Image Source: Zacks Investment Research

Chevron not only outshines ExxonMobil in dividend yield but also surpasses the industry average of 4%. On both relative and absolute terms, Chevron’s dividend performance positions it as the stronger contender.

Net Debt

Dividends are not just about attractive yields — they’re about resilience. A sustainable payout requires more than high returns; it demands a robust financial foundation that can weather challenging times. Central to this is a company’s net debt, calculated as total debt minus cash, which serves as a critical indicator of financial strength.

Between the two energy giants, Chevron carries a significantly higher net debt of $21.1 billion compared to ExxonMobil’s $9.9 billion. This disparity highlights ExxonMobil’s comparatively stronger balance sheet, positioning it to better sustain its dividend payouts even in adverse market conditions.

Capital Expenditure & Cash Flows

ExxonMobil and Chevron are ramping up their investments, but ExxonMobil is taking the lead in both spending and performance. In the first nine months of 2024, ExxonMobil’s capital and exploration expenditures surged 7.9% year over year to $20 billion, outpacing Chevron’s 5.6% increase to $12.1 billion.

Cash flow from operations — a key indicator of financial strength in the oil and gas sector — tells a similar story. ExxonMobil generated $42.8 billion so far this year, a slight uptick from $41.7 billion in 2023. In contrast, Chevron’s operational cash flow dipped, bringing in $22.8 billion compared to $23.2 billion during the same period last year.

Both companies, however, have managed to maintain solid free cash flows. ExxonMobil posted $26.4 billion, while Chevron generated $10.7 billion, thanks to their ability to cover shareholder distributions and capital expenditures with cash flow from operations.

Looking ahead, Chevron plans to reduce its 2025 capital expenditure by about $2 billion from this year’s budget. Meanwhile, ExxonMobil envisions annual capex and exploration expenses of $22 billion to $27 billion between 2025 and 2027, with projected 2024 spending between $23 billion and $25 billion.

Overall, ExxonMobil's higher investment and stronger cash flow underscore its aggressive approach to growth and stability.

Financial Health

ExxonMobil ExxonMobil and Chevron stand tall as two of the most well-managed players among global oil majors, consistently setting the bar with industry-leading financial returns. Both companies maintain enviable financial health, backed by strong balance sheets and exceptional financial flexibility.

Their ability to manage cash reserves and maintain a balanced debt-to-capitalization ratio underscores their resilience. While both excel in this regard, ExxonMobil holds a slight edge with a lower debt-to-capitalization ratio of 13.3% compared to Chevron’s 14.1%, further solidifying its position as a financial powerhouse.

Image Source: Zacks Investment Research

Accretive Acquisitions by CVX and XOM

Chevron and ExxonMobil are redefining the competitive landscape with game-changing acquisitions that solidify their dominance in the energy sector.

Chevron’s $7 billion acquisition of PDC Energy is already surpassing expectations, delivering synergy benefits above initial guidance. With 75% of PDC’s shale inventory boasting a low breakeven cost of under $50 per barrel, Chevron has enhanced its cost-efficient production capacity. This acquisition, which supports a steady output of 400,000 barrels per day, strengthens Chevron’s cash flow and ensures profitability even in challenging market conditions.

On the other hand, ExxonMobil’s $59.5 billion purchase of Pioneer Natural Resources has significantly expanded its footprint in the Permian Basin. The deal has doubled ExxonMobil’s production capacity in the region to 1,300 MBOE/d, with output surpassing 1,400 MBOE/d in the third quarter of 2024.

Then there’s also the question of the Hess Corporation HES deal. Chevron’s $53 billion buyout faces legal complications, with ExxonMobil disputing the transaction due to alleged right-of-first-refusal claims on Guyana assets. This arbitration could extend through the end of 2025, creating uncertainty over Chevron’s access to the valuable Guyana assets.

Conclusion: Not the Right Time to Buy

ExxonMobil and Chevron each excel in key areas, reflecting their stature as global energy giants. ExxonMobil takes the lead in stock performance, cash flow and debt management, showcasing a robust financial foundation and aggressive growth strategy. Meanwhile, Chevron shines with its higher dividend yield and valuation metrics, making it an attractive option for income-focused investors.

Both companies face near-term challenges, including commodity price volatility and macroeconomic uncertainties, which may limit their immediate growth potential. While their long-term prospects remain strong, the current environment suggests caution for new investments.

Both ExxonMobil and Chevron are formidable multinationals, but the timing isn't right for fresh buying. Overall, the outlook is largely neutral for the stocks, aligning with their current Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX) : Free Stock Analysis Report

Exxon Mobil Corporation (XOM) : Free Stock Analysis Report

Hess Corporation (HES) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10