Is AtriCure (NASDAQ:ATRC) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that AtriCure, Inc. (NASDAQ:ATRC) does use debt in its business. But is this debt a concern to shareholders?

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

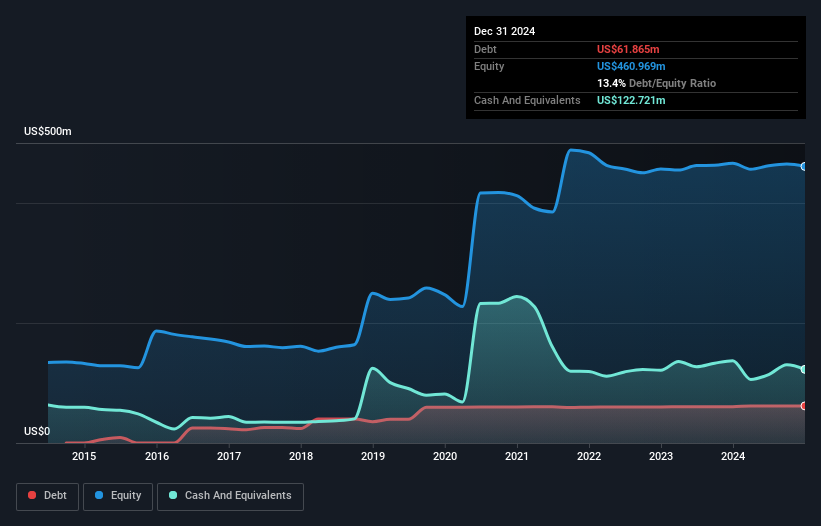

What Is AtriCure's Net Debt?

The chart below, which you can click on for greater detail, shows that AtriCure had US$61.9m in debt in December 2024; about the same as the year before. But on the other hand it also has US$122.7m in cash, leading to a US$60.9m net cash position.

How Strong Is AtriCure's Balance Sheet?

According to the last reported balance sheet, AtriCure had liabilities of US$73.4m due within 12 months, and liabilities of US$74.9m due beyond 12 months. Offsetting this, it had US$122.7m in cash and US$60.3m in receivables that were due within 12 months. So it can boast US$34.7m more liquid assets than total liabilities.

This surplus suggests that AtriCure has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, AtriCure boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine AtriCure's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts .

View our latest analysis for AtriCure

In the last year AtriCure wasn't profitable at an EBIT level, but managed to grow its revenue by 17%, to US$465m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is AtriCure?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that AtriCure had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$11m and booked a US$45m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of US$60.9m. That kitty means the company can keep spending for growth for at least two years, at current rates. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for AtriCure you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking to trade AtriCure, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10