Labcorp (NYSE:LH) Reports Sales Below Analyst Estimates In Q1 Earnings

Healthcare diagnostics company Labcorp Holdings (NYSE:LH) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 5.3% year on year to $3.35 billion. Its non-GAAP profit of $3.84 per share was 2.8% above analysts’ consensus estimates.

Is now the time to buy Labcorp? Find out in our full research report.

Labcorp (LH) Q1 CY2025 Highlights:

- Revenue: $3.35 billion vs analyst estimates of $3.41 billion (5.3% year-on-year growth, 1.9% miss)

- Adjusted EPS: $3.84 vs analyst estimates of $3.73 (2.8% beat)

- Adjusted EBITDA: $525.6 million vs analyst estimates of $577.1 million (15.7% margin, 8.9% miss)

- Management slightly raised its full-year Adjusted EPS guidance to $16.05 at the midpoint

- Operating Margin: 9.7%, in line with the same quarter last year

- Free Cash Flow was -$107.5 million compared to -$163.6 million in the same quarter last year

- Organic Revenue rose 2.1% year on year, in line with the same quarter last year

- Market Capitalization: $19.21 billion

"Labcorp delivered solid performance in the first quarter of 2025," said Adam Schechter, chairman and CEO of Labcorp.

Company Overview

With over 600 million tests performed annually and involvement in 90% of FDA-approved drugs in 2023, Labcorp (NYSE:LH) provides laboratory testing services and drug development solutions to doctors, hospitals, pharmaceutical companies, and patients worldwide.

Sales Growth

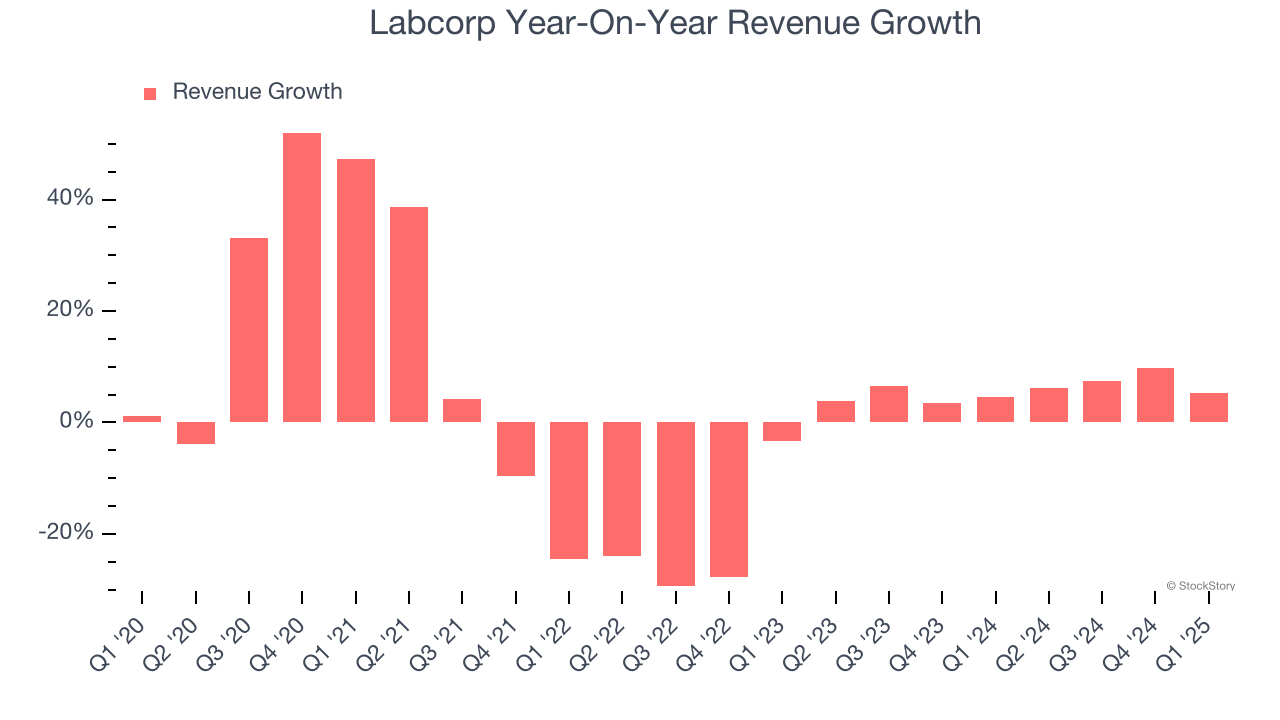

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Labcorp’s 2.6% annualized revenue growth over the last five years was tepid. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Labcorp’s annualized revenue growth of 5.9% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Labcorp’s organic revenue averaged 3.1% year-on-year growth. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Labcorp’s revenue grew by 5.3% year on year to $3.35 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months, similar to its two-year rate. This projection is above the sector average and implies its newer products and services will fuel better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Labcorp has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14.1%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Labcorp’s operating margin decreased by 15.8 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.6 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Labcorp generated an operating profit margin of 9.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Labcorp’s EPS grew at a decent 5.9% compounded annual growth rate over the last five years, higher than its 2.6% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

Diving into the nuances of Labcorp’s earnings can give us a better understanding of its performance. A five-year view shows that Labcorp has repurchased its stock, shrinking its share count by 13.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Labcorp reported EPS at $3.84, up from $3.68 in the same quarter last year. This print beat analysts’ estimates by 2.8%. Over the next 12 months, Wall Street expects Labcorp’s full-year EPS of $14.73 to grow 11.9%.

Key Takeaways from Labcorp’s Q1 Results

It was encouraging to see Labcorp beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed and its organic revenue fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $230.01 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10