「Stablecoin Pioneer」 Founder: 7 Years Ago, How I Went All in on Stablecoins

The world's second largest stablecoin giant, Circle, is set to list on the NYSE tonight and commence trading. Following the 2021 debut of the United States' largest cryptocurrency exchange Coinbase, this marks the emergence of the cryptocurrency industry's second largest native U.S. stock-listed company. Four years ago, Coinbase's listing coincided with Bitcoin's peak, and now, four years later, amidst a full crypto market cycle, Circle's listing unveils a new narrative for cryptocurrency — stablecoins.

Simply put, a stablecoin is the tokenization of the U.S. dollar, pegged to the value of the dollar, where 1 token equals 1 dollar. For a detailed explanation of stablecoins, you can refer to "The Fed Figured Out Stablecoins Three Years Ago."

Since the beginning of this year, stablecoins, along with the concept of Real World Assets on the blockchain, have noticeably diverged from previous years. The favorable U.S. stablecoin policy, the Hong Kong stablecoin policy in China, Wall Street's focus on RWA projects represented by financial behemoth BlackRock, and the participation of various institutional investors in the stablecoin space have rapidly propelled the concepts of RWA and stablecoins into the spotlight. Previously viewed with less optimism, Circle's IPO valuation has skyrocketed from around $5.4 billion to approximately $7 billion, spurred by investments from BlackRock and prominent investor Cathie Wood.

In the Bitcoin whitepaper, Bitcoin was defined as: a peer-to-peer electronic cash system. However, today's Bitcoin has evolved into a financial asset, unlikely to be used for payments. The only digital asset suitable for a peer-to-peer electronic cash system is stablecoin; this is where the true potential of stablecoins lies.

Jeremy Allarie, the founder of Circle, foresaw all this seven years ago.

Below is The Block's account of Jeremy's story.

The "Shovel Salesman" of the Web 1.0 Era

In 1990, I began my journey with the Internet and what truly captured my interest was the firsthand experience of the power of an open network, distributed systems, decentralized architecture, open protocols, and open-source software, which I often refer to as the "DNA of the Internet."

During that time, I was also observing the dissolution of the Soviet Union, which profoundly impacted me with its structural transformation. I delved deeper into technology, becoming more convinced than ever that the Internet would change the world.

By 1994, the first graphical web browser technology had emerged. At that time, I suddenly realized that we finally had a software that could display content, applications, and various things on a web page, giving rise to the concept of the "Web as an Application Platform."

So, my brother and I, along with some partners, co-founded Allaire Corporation and released ColdFusion, which was the first commercial web programming language.

Although Perl existed at the time, and people were writing dynamic page logic in C on web servers, ColdFusion truly simplified web application development—just with an idea and about a thousand dollars, you could create an interactive web application that could be used in a browser.

By 1995, this was already a significant breakthrough. With the rise of websites, e-commerce, and online content, we caught this wave. Allaire also developed a comprehensive set of tools, and millions of developers worldwide were using our software.

As the market continued to mature, we successfully took the company public in early 1999.

It was a bit "unconventional" at the time because we had a profitable IPO—that was during the Internet bubble period when most companies were going public while still in a loss-making state. But we were more like the "pick and shovel sellers" of the Internet 1.0 era, providing foundational tools for the entire industry.

After the IPO, we merged with Macromedia, a giant in developing Internet and content creation tools at the time. I became the CTO of this new company post-merger and began driving the application of Flash. It was a very powerful software then, enabling more complex multimedia presentation and interactive experiences on websites.

The "Armchair Political Economist" Falls Down the Crypto Rabbit Hole

Going back to my initial encounter with the Internet, I was originally studying international political economy, focusing on various economic systems, political institutions, and being particularly interested in macroeconomic issues of the international economic system. Then, I got excited about the Internet and was deeply fascinated by the transformative information dissemination and software distribution brought by these open networks.

During my time at Macromedia, as early as March 2002 (yes, 2002, not 2022), we incorporated seamless video playback capability into the Flash Player, making video playback ubiquitous on the Internet.

For the first time, anyone could easily embed video into a browser. The explosive growth of YouTube was built on top of this technology—it was initially based on the Flash Player.

Later on, I founded another company called Brightcove. Brightcove's concept was still based on the Internet's fundamental genes: open network, open protocol, distributed system.

My idea at the time was—could any company, any media organization directly publish video and TV content on the Internet? It was 2004, just the beginning of broadband, just the beginning of Wi-Fi, no smartphones yet, but people were already talking about the future of "connected devices."

One thing was very clear to me—I could see a future with a large number of connected devices, with Wi-Fi, with mobile broadband, and video distribution would be completely liberated.

So we built an online video distribution system—a sort of "online TV platform."

This was an extension of the capabilities of the Internet: it became increasingly rich, more faithfully realizing what people imagined in the early days of Web 1.0, finally coming true in the Web 2.0 era, and Brightcove's business was also very successful, eventually going public in early 2012.

Why Create Circle?

When the 2008 financial crisis occurred, it triggered the academic thinking I had in my early years, turning me into an "armchair political economist." I began avidly reading various materials on the nature of money, central banks, the international monetary system, and fractional reserve banking. As I wondered "what's going on?" I also started thinking: is there a better monetary system? Is there a better way to build an international financial system?

Of course, this wasn't the kind of thing where you wake up one day and say, "I'm going to start a company that will disrupt the global monetary system." It was 2009, 2010, and there wasn't a realistic path to achieve these goals at that time, I was just continuously researching.

But by 2012, shortly after Brightcove went public, I came across cryptocurrency, and from then on, I plunged down the rabbit hole.

Jeremy Allarie during the Brightcove era

Coming from a technical and product background myself, when I approached this field from a technical perspective, I saw some staggering things: this was a genuine technological breakthrough.

Some computer science challenges have been solved, and these solutions are incredibly powerful. For the first time, I synchronized the Bitcoin blockchain on my laptop and conducted a peer-to-peer transaction through it — directly over the internet, a transaction entirely reliant on open protocols. That moment for me was like the first time the Mosaic browser opened a web page — I thought, 'Wow, this is the true missing piece of internet infrastructure!'

Next, as my co-founder and I delved deeper into our research, especially within the tech community at the time, we encountered many discussions:

Aside from Bitcoin, could other types of digital assets be issued on such networks? Today we call them 'tokens' or 'digital assets.' Given my background in virtual machines and programming language development, I naturally got involved in the discussion:

How can these digital assets be made 'programmable'?

How can 'programmable money' be achieved?

How can smart contracts be built?

At that time, these things were still just concepts on napkins, with some whitepapers just emerging, but we were very clear that all of this would happen; it was only a matter of time.

So we intertwined all these ideas with another question: How to build a more secure, more open financial system? These thoughts converged in my mind, becoming the only thing I could think about; I became almost obsessed and eventually decided to found Circle.

Our vision was whether we could create an HTTP-like protocol for 'money'? Could we create an internet-native open protocol for the dollar? This protocol would be open, programmable, and so on.

This was our vision ten years ago, and now it has become a reality, serving as a true 'killer app' for the crypto space. While building this system took a long time, it has now reached significant scale, albeit still in its early stages.

The Rise of USDC

In the spring of 2018, the crypto market experienced a significant pullback, followed by a severe winter across the industry, with almost the entire market seeing a steep decline. Our products that were supposed to generate revenue and profit either became barely breakeven or started losing money, leading us to burn cash at an alarming rate.

By 2019, at the deepest point of that winter, fundraising had become extremely challenging. Simultaneously, our operating costs had spiraled out of control, and our cash was running out — without action, we were facing bankruptcy.

It was at this time that we officially launched USDC in October 2018.

A Bold Bet

In 2019, DeFi protocols began widespread adoption of USDC, and the market saw early signs of PMF. Although the market was still highly volatile at that time, from a technical perspective, Ethereum had matured enough to truly support these use cases. With tools like MetaMask and other related products, developers could finally start using these tools effectively.

Even though the transaction volume was still small at that time, the developer community had a very high acceptance of USDC. We saw this and realized that this was our company's original vision, this was our core, this was what we really wanted to do.

So, in a very short time, we quickly sold off three business units—sold off the Poloniex exchange, sold off the Circle Trade OTC business, sold off the retail-facing Circle Invest product, and also shut down and liquidated our previously launched payments app.

By selling off these assets, we obtained much-needed funds and thoroughly restructured the company. Some employees were transferred to these divested businesses, and the company as a whole underwent significant restructuring.

By the fall of 2019, we found ourselves on the brink of bankruptcy once again, but at the same time, USDC began to show early signs of vitality in the market. So we made a decision—to go all-in on USDC. We decided to dedicate all our energy to it, build a complete platform around it, and drive its widespread adoption.

This was akin to a "bet-the-company" decision, as at that time USDC itself had not generated any revenue, and the company as a whole had little to no revenue. But I firmly believed at that time that the era of stablecoins had arrived, that they would ultimately become a core part of the global monetary system, and that stablecoins were the most suitable monetary architecture for the internet age.

We had the right product at that time, and as long as we persevered, we would find the right path and create something valuable. So we went all out to drive it forward.

This was the first true significant challenge in the development of USDC. While we had faced many hurdles before, this moment was a make-or-break moment for the entire company. Although USDC had already shown early growth momentum, it was not yet enough to support a scaled-up company.

We redirected all of the company's resources toward USDC, putting all of our funds into it. I remember very clearly that we officially announced this strategy in January 2020, with the Circle website homepage undergoing a complete transformation into a giant billboard promoting "Stablecoins are the future of the international financial system." The only clickable button on the page was "Get USDC." Everything else was removed.

Then on March 10, 2020, we released a Circle platform upgrade, completely overhauling the USDC account system and introducing a new set of APIs to facilitate seamless integration of banking, card networks, and other payment systems for developers to enable USDC deposits and withdrawals. The entire platform was built around USDC.

Just three days later, on March 13, the world went into lockdown due to the COVID-19 pandemic. Interestingly, USDC had already started growing back in February 2020, before our official release. I believe this was because Asian market users had already recognized the severity of the pandemic and began to react early.

During that time, a very complex interweaving of events occurred: many people, due to a lack of trust in their national financial systems, began to move funds into digital dollars; at the same time, various governments globally implemented large-scale emergency stimulus policies, attempting to inject liquidity into the markets to prevent an economic depression.

As a result, you saw a highly coordinated ultra-loose monetary policy globally, leading to a massive influx of funds into the markets. People were sitting at home with government stimulus checks, pondering, "How should I use this money?"

During that period, the world also experienced a significant turning point—a sudden acceleration of society's digitalization process.

The concept of the Metaverse became popular from that point onwards, and overnight, everyone went digital. All digital products experienced explosive growth. From Zoom (which almost became the iconic company of that time), to at-home fitness company Peloton, to e-commerce, online retail, digital payments, online marketplaces—almost every digital industry experienced a five-year growth acceleration in that phase.

Simultaneously, the adoption of blockchain technology and the digital asset market also entered an explosive phase.

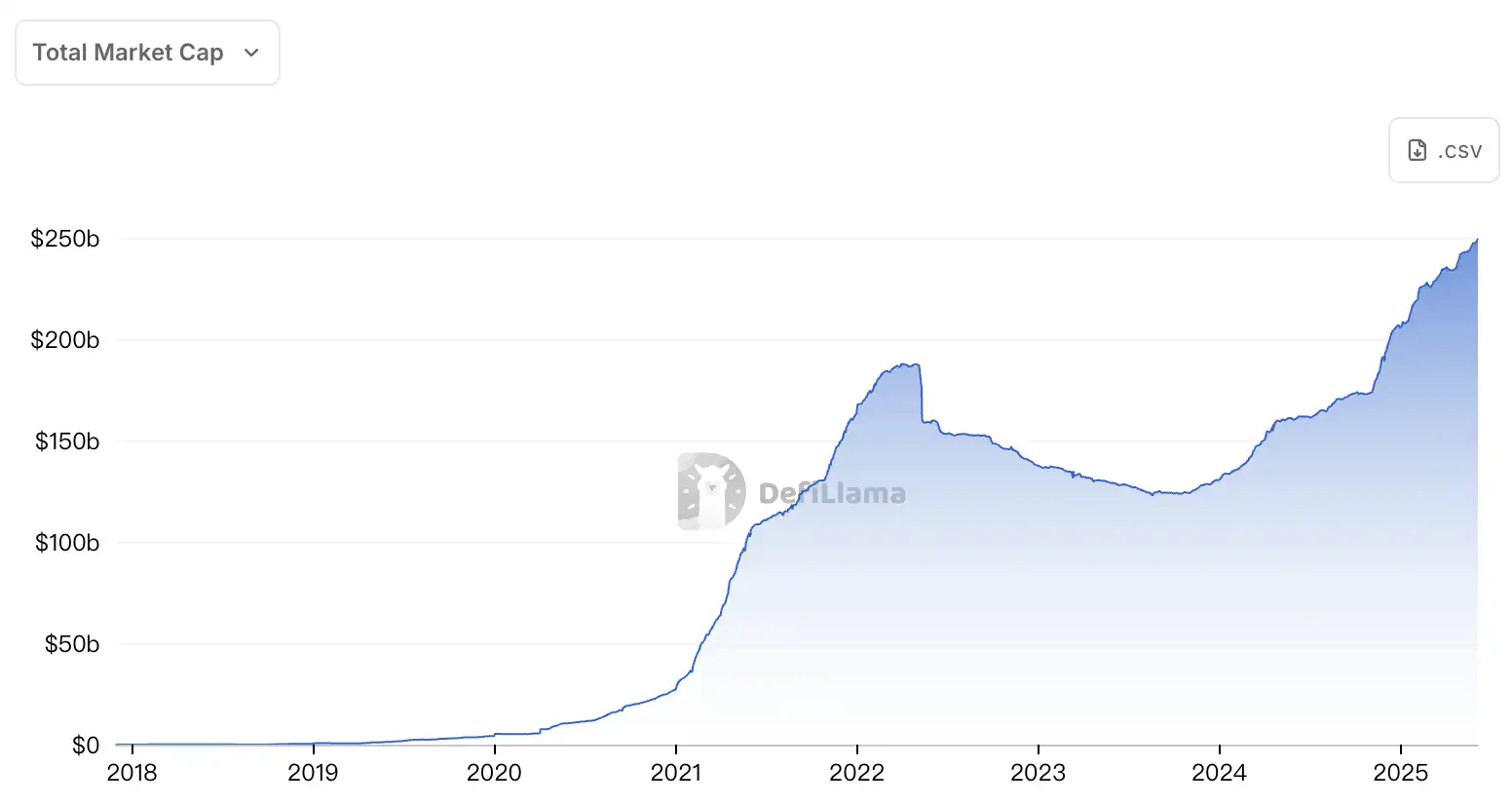

The summer of 2020 was dubbed the "DeFi Summer," and USDC, starting with a $400 million circulating supply in early 2020, skyrocketed to $40 billion within a year, experiencing a dramatic and explosive growth.

Stablecoin Market Cap Growth Curve

The Preconditions for Stablecoin Mass Adoption

Over the years, and even just a year or two ago, people often asked: "How can this thing achieve true mass adoption?" My consistent response in the past has been: we need to address three key issues. Of course, here "we" refers not only to Circle but to the entire industry, requiring collective efforts to drive forward.

The first issue is infrastructure, which refers to the blockchain network itself.

My mental model of a blockchain network is: they are like the "operating system of the internet." What we need is a high-performance, high-throughput operating system-like blockchain network. Over the past few years, great progress has been made in this area. We are now in the era of "third-generation blockchain networks" — high-performance Layer1 public chains and Layer2 scaling solutions.

This means that higher transaction throughput can be achieved, and the cost of a single transaction is extremely low, possibly less than a cent, or even less than a penny.

Coinbase CEO Brian Armstrong previously mentioned "transaction times less than one second, costs less than one penny," and we have indeed basically achieved this state. The progress of these high-performance networks is also driving growth throughout the ecosystem. By reducing unit costs, marginal costs, and increasing transaction speed, it’s like moving from the dial-up internet era to broadband internet, transitioning from Web1.0 to Web2.0.

The second issue is network effects. Stablecoins like USDC are actually a network-based product platform, where developers build applications on it. The more applications that are onboarded, the stronger the utility of the entire network. The more users holding the stablecoin, the greater the network's utility, creating a positive feedback loop.

At a certain stage, developers may even realize that if their product does not support USDC, they may already be falling behind in the competition. So, after the infrastructure upgrade is completed, this network effect between users and developers truly begins to take effect.

Next is the third issue, the so-called improvement in "usability," which is actually closely related to infrastructure upgrades. Remember a couple of years ago when, if you wanted to use a stablecoin, you had to first go to a platform to purchase it, then install a browser extension wallet, buy Ethereum to be able to use the wallet, pay expensive fees, transfer ETH to your self-hosted wallet, and the whole process took seven to eight minutes, not to mention being particularly cumbersome, the entire process was completely illogical.

At that time, if someone said, "Who would want to use this thing?" it was completely understandable.

But now, you can directly access the wallet system through a web interface or a mobile app, and the whole experience is as simple as registering for WhatsApp, possibly only requiring a phone number, a facial recognition or biometric code, without needing to remember mnemonics or deal with a bunch of complex settings.

All of these changes are coming together to create a favorable environment, making stablecoins more easily accepted and used.

The final ultimate hurdle is government regulation.

Most excitingly, now on a global scale, from Japan, China Hong Kong, Singapore, to all of Europe, the UK, UAE, and the US, almost all major jurisdictions are gradually introducing relevant laws explicitly recognizing stablecoins as legal tender and integrating them into the formal financial system.

Once these laws are in place, the use of stablecoins will shift from early crypto natives to a broader population. Therefore, by the end of 2025, we believe that stablecoins are likely to become a widely accepted and integrated part of the global financial system.

Of course, we must also recognize soberly that all of this is still in a very early stage. You can look at the current state through Geoffrey Moore's "Crossing the Chasm" theory: we are like in the process of leaping over that "chasm" in mid-air, not yet touching the ground, and still at risk of failure or falling. But I believe we will make the jump.

We can see more and more what I call "FinTech-friendly banks," or "emerging digital banks (neobanks)," institutions starting to natively support the use of stablecoins. For example, Latin America's NuBank, Europe's Revolut, or brokerage apps like Robinhood.

Of course, this also includes large crypto companies like Coinbase and Binance, which together have over 400 million users. To some extent, they have actually become "financial super apps": you can hold balances, receive wages, link cards for spending, and the process of obtaining and using USDC has become very seamless.

Indeed, we are witnessing a trend—people are starting to see the "dollar" as a store of value, but its underlying form is actually USDC.

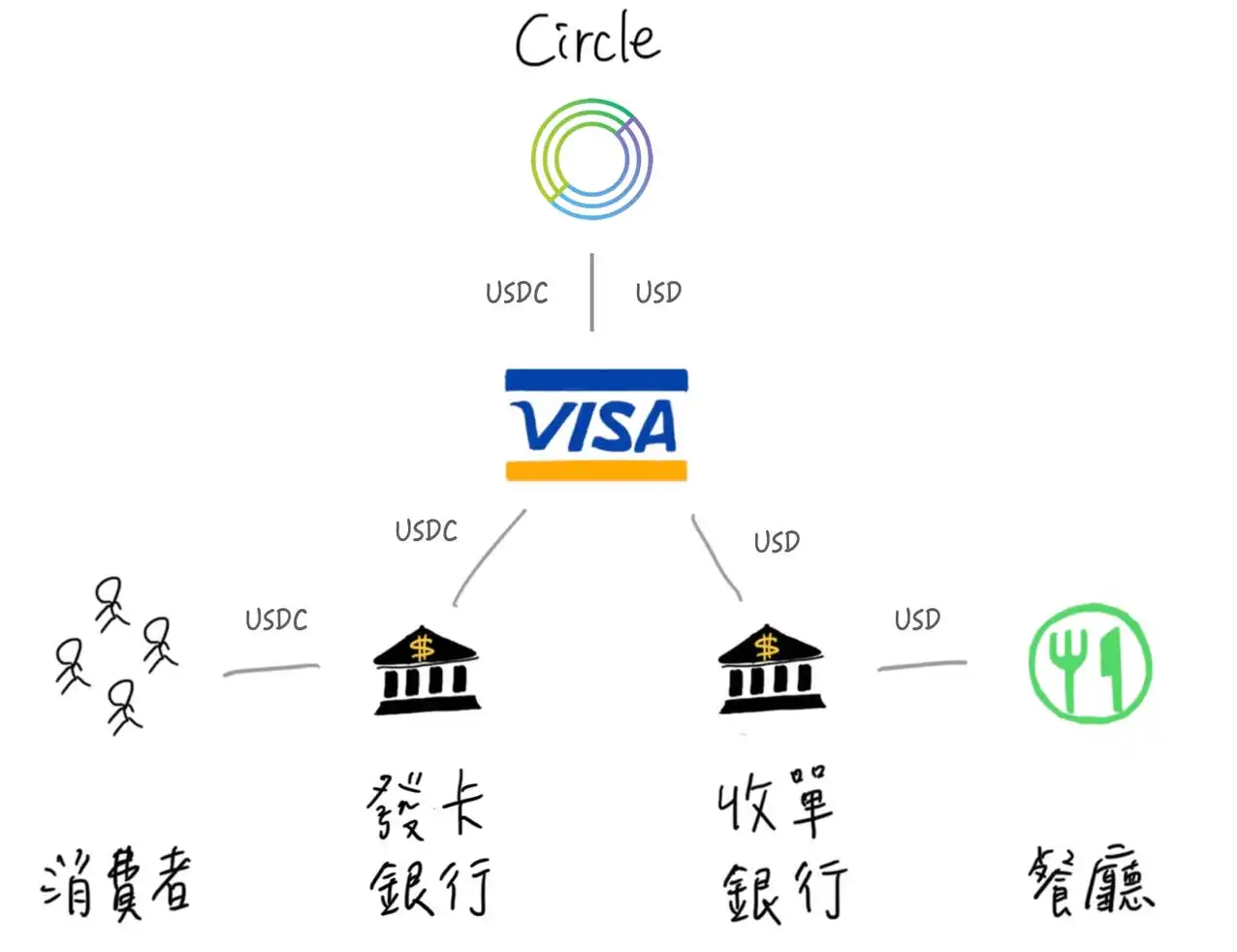

And now we are already cooperating with Visa and MasterCard, both of which have projects allowing card issuers to issue cards: on the surface, they are Visa or MasterCard, but when actually used for consumption, they use stablecoins like USDC.

This model has already emerged in emerging markets in large numbers, where users obtain a physical or virtual card through a new bank-style digital wallet app, and the card is linked to their stablecoin balance. Because many people want to hold dollars, these cards allow them to continue to spend in traditional card networks, but the settlement in the background is done in USDC.

Even for these card issuers, the settlement funds they pay to Visa or MasterCard can now also be settled directly via USDC. In other words, USDC has actually been used as a settlement channel between financial institutions and card networks, which is interesting in itself.

At the same time, we are also seeing changes on the other side—meaning the merchant acquiring side is also joining in, with companies like Worldpay, Checkout.com, Nuvei, and Stripe offering USDC settlement options to merchants.

Earlier this year, we saw a very cool example: Stripe co-founder John Collison, at their annual event, made a "keynote announcement" as usual, and his exact words were something like: "Crypto is back, but this time it's not Bitcoin, it's USDC, the stablecoin."

He demonstrated a new feature in the Stripe Checkout product—this product allows merchants to embed Stripe's payment gateway directly into their website or app. In the demo, USDC was shown alongside credit cards as a payment option, and merchants could choose to accept USDC.

Collison was on stage excitedly showcasing the entire process, and he said, "This is how payments should be." In the demo, they were using the Solana network, with real-time settlement and very low fees.

With the gradual clarification of the legal status of stablecoins, more and more financial institutions will see them as a foundational settlement layer.

For example, a merchant might say, "I am willing to accept USDC because I can receive the funds instantly and save on fees, which is a better option for me."

On the user side, there are also more and more types of end-user products emerging—whether traditional banks, neobanks, or crypto super apps, they are all creating a seamless experience where users can simply scan a QR code to complete a payment.

Another major development I mentioned on Twitter earlier this year was that iOS has started to open up NFC for third-party wallets. This means that Web3 wallets may support "Tap to Pay" in the future, allowing users to directly pay at physical merchant terminals using a wallet with USDC.

Of course, achieving this will require cooperation from various parties, such as payment processors, acquirers supporting on-chain transactions, wallet developers integrating NFC functionality into their product, and obtaining approval from Apple.

However, all of these are already in the works and are expected to see larger-scale implementation by 2025, which is indeed an exciting development.

Favorable Policy Environment Continues

Since day one of Circle's founding, the idea has been to stand at the intersection of the traditional financial system and the new world of blockchain. To achieve this, the U.S. government had already clarified its legal stance back in March 2013:

If you are a company that connects the banking system and the world of virtual currency at the same time, you belong to a "money transmitter," you must register with the federal government, have a comprehensive anti-money laundering program, and must apply for a license in every state with relevant legal requirements.

We are the first company in the crypto industry to start from scratch and obtain a full set of compliance licenses. We are the first crypto company in Europe to obtain an Electronic Money Institution (EMI) license and the first company in New York to obtain the so-called "BitLicense"—the first regulatory license specifically designed for the crypto industry. Nearly a year after that, we were the only ones holding this license.

We have always adhered to the "regulation-first" concept, always choosing the "front door" approach to ensure that we have a good and robust compliance system. By the way, it is precisely because of this compliance foundation that we can achieve another key goal: liquidity.

What is liquidity? It means that you can truly create and redeem stablecoins, connect to real bank accounts, purchase and redeem stablecoins with fiat currency. If you are a suspicious offshore company, no one is willing to open a bank account for you, so you cannot do any of these things. You don't even know where your bank is.

We are the first company to establish high-quality banking relationships and have introduced strategic partners such as Coinbase to mass distribute USDC on the retail side, allowing any ordinary user with a bank account to easily buy and redeem USDC. We also provide institutional-level services. That is to say, from transparency, compliance, regulatory framework to actual liquidity, we have done it all.

On the level of technological innovation, we have also been exploring what the protocol itself can do. We see USDC as a stablecoin network protocol and have been thinking about how to collaborate with developers to promote its integration and application. These fundamental principles are the root cause of how far we have come today, and we are still continuously building, not just for the U.S. market.

In terms of payment-type stablecoins, various parties in the U.S. have actually done a lot of work. The "Stablecoin Tethering and Bank Licensing Enforcement Act," in my opinion, is already quite mature, with bipartisan support in the House of Representatives and active participation from the Senate leadership. We have also seen a high level of government attention, including the White House, the Treasury Department, and the Fed. This issue has been prioritized by the government for several years.

(Translator's Note: On May 19, the U.S. Senate passed the procedural vote for the "2025 U.S. Stablecoin Innovation and Facilitation Act" (GENIUS Act) with a vote of 66-32, aiming to provide federal regulation for stablecoins pegged to the U.S. dollar.)

Many key issues, such as how to ensure financial security and stability while supporting private sector innovation, the role the Federal Reserve should play (establishing a standard for a USD stablecoin), and how to provide a pathway for issuers and regulators in each state, similar to the current "dual banking system" — where you can be a state-chartered bank or a federally chartered bank — are all in progress.

The financial system itself is a highly regulated industry, the energy system is highly regulated, the transportation system is highly regulated, the aerospace system is highly regulated, and pharmaceutical production is also highly regulated. In fact, most critical technologies or infrastructure in society are under intensive regulation.

The software industry has perhaps been an exception in the past thirty years, with minimal regulation. But now, if you are doing something particularly large-scale, cutting-edge, such as artificial intelligence, hardware-integrated autonomous driving, or building a global digital currency system — these areas have begun to intersect with those traditional highly regulated industries, and they have significant potential impact on society, so being regulated in these cases is reasonable.

I do not believe that "innovation should not be regulated." If something becomes extremely critical to society as a whole, then it needs to have a corresponding spirit of contract and a framework of social responsibility, which is the reality of existing institutions. Regulations can be light or heavy — for example, global systemically important banks (G-SIBs) are subject to far more regulation than a local community bank.

So, if what we are doing becomes systematically important in the future, not only will our relationship with the U.S. government change, but our relationship with other governments will also change. Of course, these are far-off things for the future and are not relevant now.

What we are really focused on now is how to realize our vision for an internet-based financial system, how to make "open, programmable, composable money" a reality. We hope that this innovation can truly take root and not be stifled. And to achieve this, policymakers and governments also need to give more freedom for innovation — just as the internet has received in other areas.

Circle's Business Model

I believe Circle is one of the most transparent financial institutions in history. If you observe a bank, insurance company, or any other type of financial institution, you will find that they do not provide real-time public information on their product operations, nor do they disclose the basic data of their balance sheet daily, which is exactly what we have been doing.

This is how it works in practice: First, when we receive USD, before minting USDC, these USD are pre-stored in a reserve account. This reserve fund is established for the benefit of customers, as required by law. Legal and regulatory requirements mandate the segregation of these funds, and only after this segregation is complete can we issue the digital currency instrument, with ownership of the funds belonging to the customers. Therefore, from a legal, regulatory, and operational standpoint, we adhere strictly to these guidelines.

Ensuring Reserve Security

So, what does this reserve consist of? Currently, the reserve is primarily composed of two parts:

Currently, around 90% of the reserve is held in an account called the Circle Reserve Fund. This is crucial. We want anyone interested in USDC to be able to clearly see the composition of these reserves within a regulated structure. Therefore, we have partnered with the world's largest asset management company, BlackRock, to establish the Circle Reserve Fund.

This fund is essentially a government bond fund, or can be understood as a government currency fund, with the sole purpose of holding the reserve assets of USDC. It is issued in a securities form, regulated by the U.S. Securities and Exchange Commission, and has independent auditing and an independent board of directors.

All the assets of this fund are fully transparent and updated daily. If you search "USDC" online, you can visit the BlackRock website and clearly see the face value, purchase time, and maturity time of each government bond. All the bonds mature within 90 days, are highly liquid, and represent stable-priced USD assets.

Additionally, there are assets in the form of "overnight Treasury repo agreements" provided by Global Systemically Important Banks (G-SIBs), which are essentially equivalent to treasury assets.

Therefore, every component of this reserve structure is visible and transparent. Anyone familiar with market liquidity and financial assets will tell you that if we need to redeem all assets within 24 hours, it can be entirely achieved.

Furthermore, approximately 10% of the reserves are essentially held in cash at several Global Systemically Important Banks, colloquially known as "too big to fail" banks. Currently, there are about 50 such banks globally, including institutions like JPMorgan Chase. We have publicly disclosed some of these partner banks. These banks, due to their massive size and stable reputation, essentially have implicit government backing.

In addition, we have built global infrastructure to support institutional customers in creating and redeeming USDC. The reason we can conduct these operations is that we are a regulated company. Banks and regulators worldwide are willing to let us operate in local markets as a result.

We are currently licensed in Singapore and Europe, and are also working to establish compliant distribution channels in Japan and other regions. This means that institutions can open accounts in the Singaporean banking system, Hong Kong banking system, Brazilian banking system, U.S. banking system, and European banking system to mint or redeem USDC.

In other words, as long as you have a bank account in these countries or regions, whether you are an individual or an institution, you can mint and redeem USDC, with the funds flowing directly into the aforementioned reserve structure.

Therefore, from the local banking system's operational perspective, you have the liquidity to mint and redeem; from the underlying reserve asset perspective, you have the most liquid and robust asset backing; and there is also a publicly registered, daily-disclosed reserve fund structure, overlaid with regulatory oversight from global regulatory authorities.

Circle's Future Plans

You may recall that before the iPhone, there were approximately 17 different mobile operating systems on the market: Symbian, Windows Phone, Palm, BlackBerry, and those from NTT Docomo—various systems, with each company trying to onboard developers, push their own mobile OS, and distribute it.

To be honest, the user experience with those systems was terrible, simply not good. You would go to the Mobile World Congress and see a bunch of people showcasing what they had built on Symbian, only to find it was all junk.

So, what I want to say is, in a way, how to ensure reserve security—although those systems were architecturally advanced, the actual user experience was poor.

They were more like an operating system, competing in ecosystems, developer resources, user-friendly features, and so on. But I want to be very clear: we have not yet seen the "iPhone moment" for blockchain.

What we truly need is a blockchain network that not only powers the world of financial transactions.

It should also support social interactions, gaming, content, intellectual property, AI data provenance, AI agent transaction flows, retail-scale applications, mass-market digital tokens, and more—and currently, these are beyond reach. The throughput is insufficient, the system cannot handle it, and the infrastructure is not yet scalable.

In the long run, we need a network capable of processing millions of transactions per second, and this is an achievable goal. At the same time, aspects like software engineers' development experience and user experience are still in the early stages.

Reflecting on my past experiences in platform software, developer tools, and user experience, I feel that we are not quite ready yet. Of course, I agree on one thing—we are very close.

But even if we really had a "click-and-go" blockchain platform, I believe that new layers would continue to be added on top of it, and more networks would emerge.

You can foresee a period where, for example, you are a large Asian internet company with 500 million users, and you now want to introduce digital tokens, stablecoins, and smart contracts for these users. Once you open it up for use, all current infrastructure on the market will collapse immediately—it simply cannot handle such a large volume of traffic.

However, you can imagine that one day, this model will evolve similar to AWS's "Virtual Private Cloud" (VPC), where a new type of "dedicated blockchain" will emerge, forming a network model of chain-to-chain connectivity to support large-scale expansion. This will essentially bring about more "fragmentation," but it also means more infrastructure development.

As Circle, our goal is to ensure that stablecoin network protocols such as USDC, EURC, CCTP (Cross-Chain Transfer Protocol), Gas Fee Abstraction, etc., can be easily invoked in these environments—so that users and developers do not need to worry about the underlying complexity.

So whether the future will support 15 chains or 50 chains, I can't tell you the specific number, but what I can assure you is that we will continue to expand, deploy, and release stablecoin infrastructure to support more blockchain networks.

As for when the "iPhone moment" will truly arrive, or when it will enter the stage of diminishing marginal returns, I do not know.

Speaking of currency, we have already launched USDC and EURC. I cannot say for certain that we will issue more currencies in the future, but what I can confirm is this: on a global scale, stablecoin regulatory frameworks are gradually being established in both emerging and developed countries, and we are seeing more and more high-quality stablecoin projects going live.

I believe that by 2025, you will see an increasing number of fiat currency stablecoins such as the Mexican Peso, Yen, Australian Dollar, British Pound, and others. And Circle does not necessarily need to be the issuer of all these currencies; what we really need is compliant, high-quality local teams to issue these stablecoins using the infrastructure we have built, thereby achieving excellent cross-currency interoperability, allowing apps to easily access and use different currencies.

Issuing each currency is very complex, involving a lot of legal and regulatory issues, as well as considerations of the preferences of local central banks, market acceptance, and so on.

We will also assess the market size, such as how big the market is for this currency, which is also a key point as mentioned earlier.

We sincerely believe that in this "Internet Finance System era," the status of the US dollar will only become more important, and the US Dollar Coin (USDC) will be at its core. So our main focus will undoubtedly remain on this.

At the same time, we also want to establish gateways in various global markets, fostering interoperability. We will continue to drive this initiative forward and are also very supportive of the development of other projects.

However, from a business or ecosystem perspective, we do not believe that we must be the ones to handle all these non-dollar currencies.

From a monetary theory perspective—be it from the central bank's standpoint or a commercial bank's perspective—there is actually a concept known as "neutral interest rate." This rate does not lean towards being accommodative or tight.

After the 2008 financial crisis, we went through a prolonged period of a "zero lower bound" on interest rates. At that time, there was also government debt monetization to counter the crisis. Subsequently, due to soaring inflation, the central bank made a strong tightening move. This interest rate policy operates in a cyclical pattern.

But whether it's the "nominal interest rate" or the "neutral interest rate," fundamentally, they fluctuate within a target range. Some economists now believe that the neutral interest rate might be around 2.75% to 3%—a level that neither hampers the economy nor excessively stimulates it.

Therefore, whether you are a central bank or a bank, a high interest rate does not necessarily mean "good." Of course, banks or institutions like us may benefit somewhat on the balance sheet from the increased interest income on reserve assets. However, overall, this environment is restrictive—economic activities decrease, the velocity of funds slows down, capital investment decelerates, and risk appetite diminishes.

When interest rates fall, indeed, the interest income from our reserve assets will also decrease; this is an objective fact. However, at the same time, funds become cheaper, liquidity strengthens, capital investment increases, and the economy speeds up—a positive development for the venture capital market, the real economy, entrepreneurial activities, all of which, in turn, promote the use and growth of stablecoins.

We have been through an accommodative cycle and also experienced a tightening cycle. The next phase may be a more moderate one, which we cannot yet predict. But we always believe:

On the one hand, macroeconomic forces are at play, which are beyond our control, such as the global economic trajectory, central bank decisions;

On the other hand, we have constructed a platform network ourselves, with a user growth flywheel, a developer ecosystem flywheel. We are building a highly practical form of digital currency and creating a robust development platform—this system inherently possesses its own growth logic.

Today, the total market size of the global "Central Bank Digital Currency" exceeds $100 trillion. I believe that one subset of this, the stablecoin market represented by USD stablecoins, EUR stablecoins, will continue to grow, whether interest rates are high or low.

What we are seeing now is that the total size of the stablecoin market is only a mere $160 billion (now over $200 billion), accounting for only 0.16%. This is clearly still a very early stage.

If you agree with how "Internet-level utility" has reshaped media, communications, transportation, and software distribution, then you would also believe that this new form of internet-based currency could also potentially have the same transformative effect in the future.

If all goes well, perhaps in the next 10 to 20 years, we could see 10% of the global money supply take the form of stablecoins. This may sound ambitious — as reaching a 10% penetration rate for internet products indeed takes a decade or more — but it will indeed change the world.

We hope that Circle can be a significant participant in this transformation.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10