Fair Isaac (NYSE:FICO) Shares Fall 14% Over Last Month

Fair Isaac (NYSE:FICO) experienced a 14% decline in its share price over the last month amidst several key events. The company's recent removal from three Russell 1000 indices could have influenced this downward movement by impacting investor sentiment. Meanwhile, initiatives like the partnerships with MI New York and MeridianLink may underscore efforts to enhance market presence and product offerings, although these positive steps seemingly didn't offset the broader decline. Despite a share repurchase program highlighting the company's commitment to shareholder value, the flat market performance over the last week suggests limited external support for the stock's recovery.

Be aware that Fair Isaac is showing 2 risks in our investment analysis.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

The recent news surrounding Fair Isaac's removal from the three Russell 1000 indices and new partnerships with MI New York and MeridianLink has stirred investor sentiment, impacting the company's narrative. While the share price witnessed a 14% decline over the past month, it remains essential to consider its overall performance over a longer horizon. Over the last five years, Fair Isaac has achieved a total return of 273.77%, showcasing strong long-term growth despite recent fluctuations. This performance contrasts with its recent underperformance relative to the US Software industry, where Fair Isaac's one-year return lagged behind the industry's average increase of 20.6%.

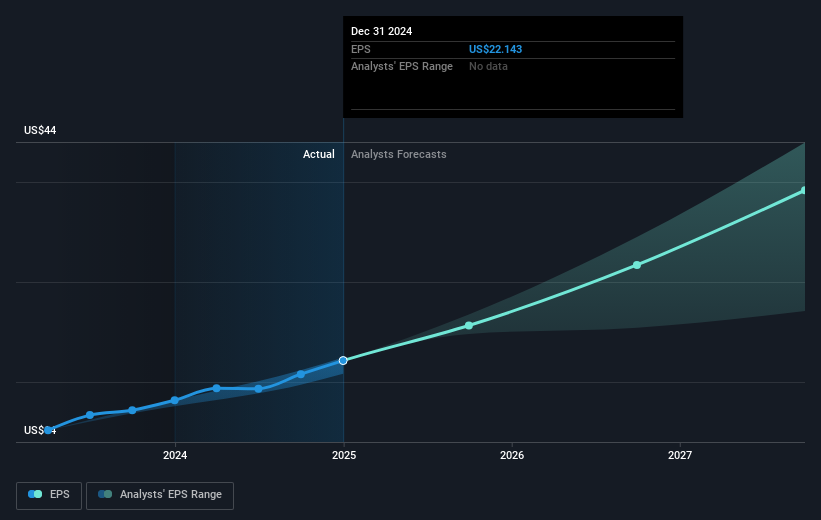

The recent announcements could influence the company's revenue and earnings forecasts, particularly given the plans to expand international markets and diversify product solutions. However, the ongoing share price discount to the analysts' consensus price target indicates a potential valuation gap. Currently trading at US$1703.17, Fair Isaac's share price is 22.4% lower than the consensus price target of US$2195.28. This suggests that while analysts anticipate future revenue and earnings growth bolstered by initiatives such as the Mortgage Simulator, market sentiment has yet to align fully with these expectations. Investors should weigh the potential for increased revenue against the macroeconomic risks highlighted in the company's narrative.

Insights from our recent valuation report point to the potential overvaluation of Fair Isaac shares in the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10