Megaport (ASX:MP1) Is Up 13.4% After South Carolina Expansion With DartPoints Partnership Has The Bull Case Changed?

- Earlier this week, Megaport and DartPoints announced a partnership establishing Megaport’s global connectivity platform at DartPoints' Greenville Data Center, marking Megaport’s first location in South Carolina and expanding direct cloud access in the Southeast US.

- This collaboration allows regional enterprises to securely access major cloud providers with reduced latency, lower bandwidth costs, and streamlined operational management, addressing a longstanding need for private cloud connectivity in the area.

- We'll explore what Megaport’s entry into South Carolina means for its US expansion and future growth narrative from an investment standpoint.

Find companies with promising cash flow potential yet trading below their fair value.

Megaport Investment Narrative Recap

To be a shareholder in Megaport, you need to believe that its network expansion and new data center partnerships will translate into sustained revenue growth, while operational discipline keeps costs in check. The DartPoints partnership marks a meaningful step in US market expansion and adds to the near-term growth catalysts, but the main risk, balancing extensive expansion against rising costs, remains present and isn't materially reduced by this news.

The earlier announcement of Megaport’s global network extension through partnerships in Brazil is especially relevant, as it underscores the company’s broader goal of increasing market presence and direct cloud access across regions. These expansions support Megaport’s ambitions but also add pressure to execute well and manage costs, key factors influencing the investment narrative.

Yet, while Megaport’s footprint grows, investors should be aware that intensifying competition in the cloud connectivity market could...

Read the full narrative on Megaport (it's free!)

Megaport's narrative projects A$310.1 million in revenue and A$42.3 million in earnings by 2028. This requires 14.4% yearly revenue growth and a A$36.3 million earnings increase from the current A$6.0 million.

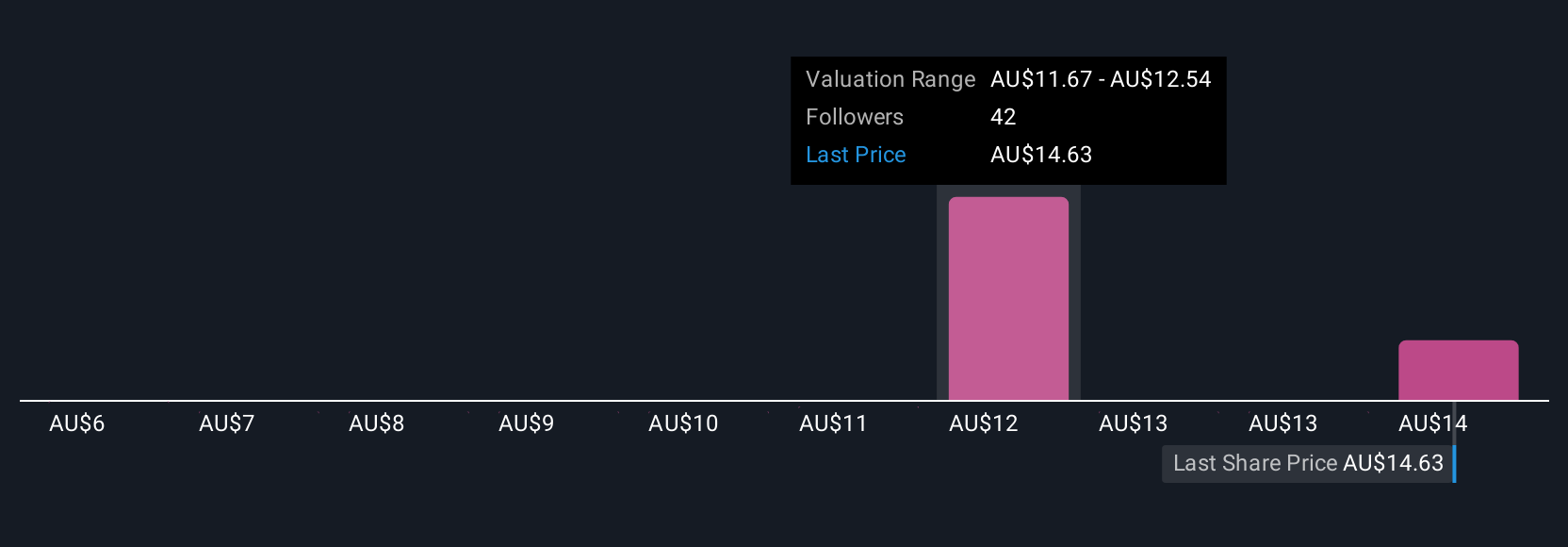

Uncover how Megaport's forecasts yield a A$12.07 fair value, a 17% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community member fair value targets for Megaport range from A$6.40 to A$15.17, with five differing analyses. As many continue to focus on expanding network capacity as a growth catalyst, these viewpoints highlight just how much expectations for future performance diverge, consider exploring several perspectives before drawing your own conclusions.

Explore 5 other fair value estimates on Megaport - why the stock might be worth as much as A$15.17!

Build Your Own Megaport Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Megaport research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Megaport research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Megaport's overall financial health at a glance.

No Opportunity In Megaport?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10