Citigroup (C) Appointed Depositary Bank for Youlife ADR Program on Nasdaq

Citigroup (C) has recently been designated as the depositary bank for Youlife Group Inc.'s ADR program, a move reinforcing its prominent role in global financial services. Over the last quarter, Citigroup shares have experienced a significant price increase of 41%, driven in part by robust financial performance, including a net income rise and strategic initiatives like its substantial buyback program. These developments align with a broader market uptrend, where the overall market has risen, adding weight to Citigroup's impressive quarterly performance, as they report increasing dividends and secure strategic partnerships.

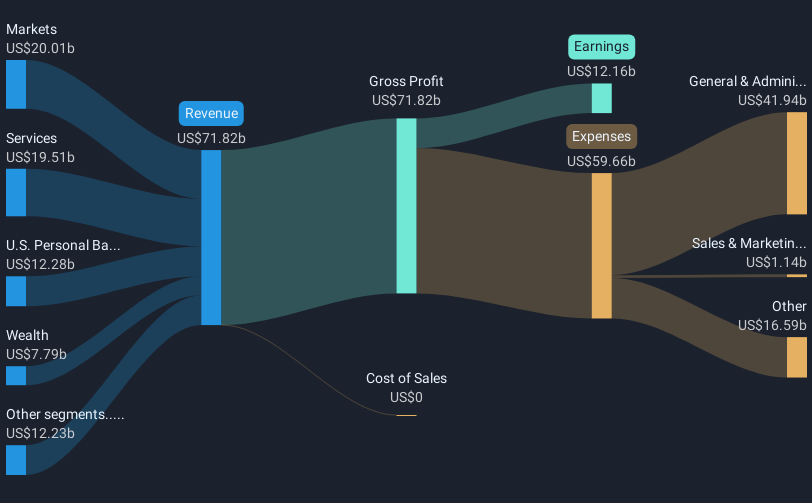

Buy, Hold or Sell Citigroup? View our complete analysis and fair value estimate and you decide.

These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Citigroup's recent role as the depositary bank for Youlife Group Inc.'s ADR program could enhance its global financial service reputation, potentially boosting both its revenue and earnings forecasts. By securing this strategic partnership, Citigroup may see increased revenue from transaction fees, positively impacting future financial performance as indicated by bullish analyst expectations. The development is part of Citigroup's broader strategic initiatives aimed at increasing operational efficiency and client acquisition through AI and infrastructure modernization.

Over the last five years, Citigroup has achieved a total shareholder return of 120.67%, including share price growth and dividends. This performance highlights a consistent upward trend, contrasting with the company's recent significant 41% increase in shares over the last quarter alone. On a one-year basis, Citigroup's earnings growth of 85.6% surpassed the Banks industry's 7.7% growth, further signifying its strong performance against market standards.

The current share price of US$95.99 remains slightly below the analyst consensus price target of US$99.45. This indicates moderate room for appreciation according to the current market sentiment. The company's ongoing investments in wealth management and AI could align with optimistic forecasts for revenue, which bullish analysts expect to grow by 8.3% annually over the next three years. However, potential global trade and economic uncertainties could pose risks to these optimistic projections.

Understand Citigroup's earnings outlook by examining our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10