Mondelez International (MDLZ) Announces REESE'S OREO Collaboration And 6% Dividend Increase

Mondelez International (MDLZ) recently announced a 6% dividend increase and introduced new collaborations with Reese's, launching innovative products like the REESE'S OREO Cup. Despite a solid 2.85% share price increase over the last month, these developments come amid broader market trends focused on corporate earnings and Federal Reserve interest rate decisions. The company's positive Q2 earnings report, showing rising sales, contrasts with a decline in its six-month net income, adding a complex layer to its overall financial outlook. While these factors lend weight to the share price movement, they align with market dynamics, which also experienced a slight uptick.

We've identified 1 risk for Mondelez International that you should be aware of.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

The recent 6% dividend increase and innovative collaborations with Reese's could strengthen Mondelez International's brand presence and consumer engagement, aligning with their strategic focus on long-term value creation. These moves may offset some of the pressure from elevated cocoa costs and softer consumer demand, as highlighted in the company's narrative. Over the past five years, Mondelez has posted a total return of 41.35%, reflecting a consistent growth trajectory despite recent volatility in the broader market.

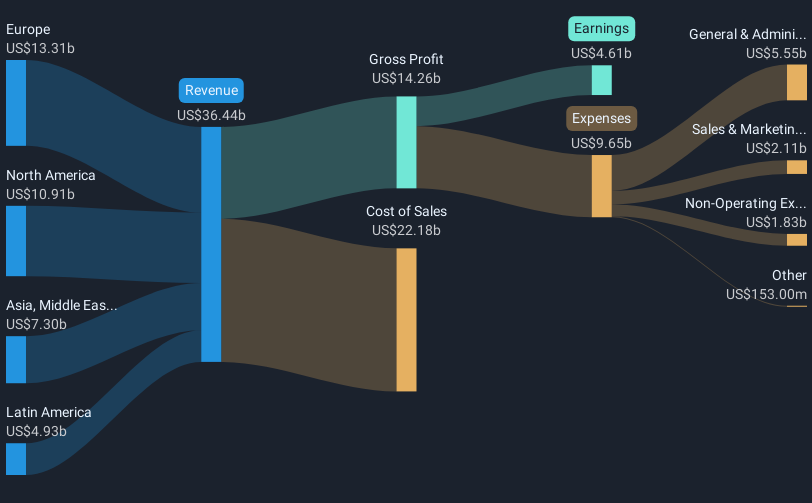

In the shorter term, Mondelez's shares experienced a modest 2.85% increase in the last month, despite being below the analyst consensus price target of $73.70. The analysts anticipate future revenue growth of 4.8% annually and earnings reaching $4.6 billion by 2028, driven by pricing strategies and global market expansion. While the company's share price remains at a 5.70% discount to the price target, the recent dividend hike could enhance investor confidence and potentially influence revenue and earnings forecasts positively.

Comparing performance to the industry, Mondelez outperformed the US Food industry, which declined by 8% over the past year, but underperformed the US Market, which posted a 17.5% return. This comparison highlights Mondelez's resilience in a challenging industry landscape. Despite this, analysts note the company's current Price-To-Earnings Ratio of 25.1x is higher than both industry and peer averages, suggesting the shares may be considered expensive by some investors.

Our comprehensive valuation report raises the possibility that Mondelez International is priced higher than what may be justified by its financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10