Assured Guaranty (NYSE:AGO) Exceeds Q2 Expectations

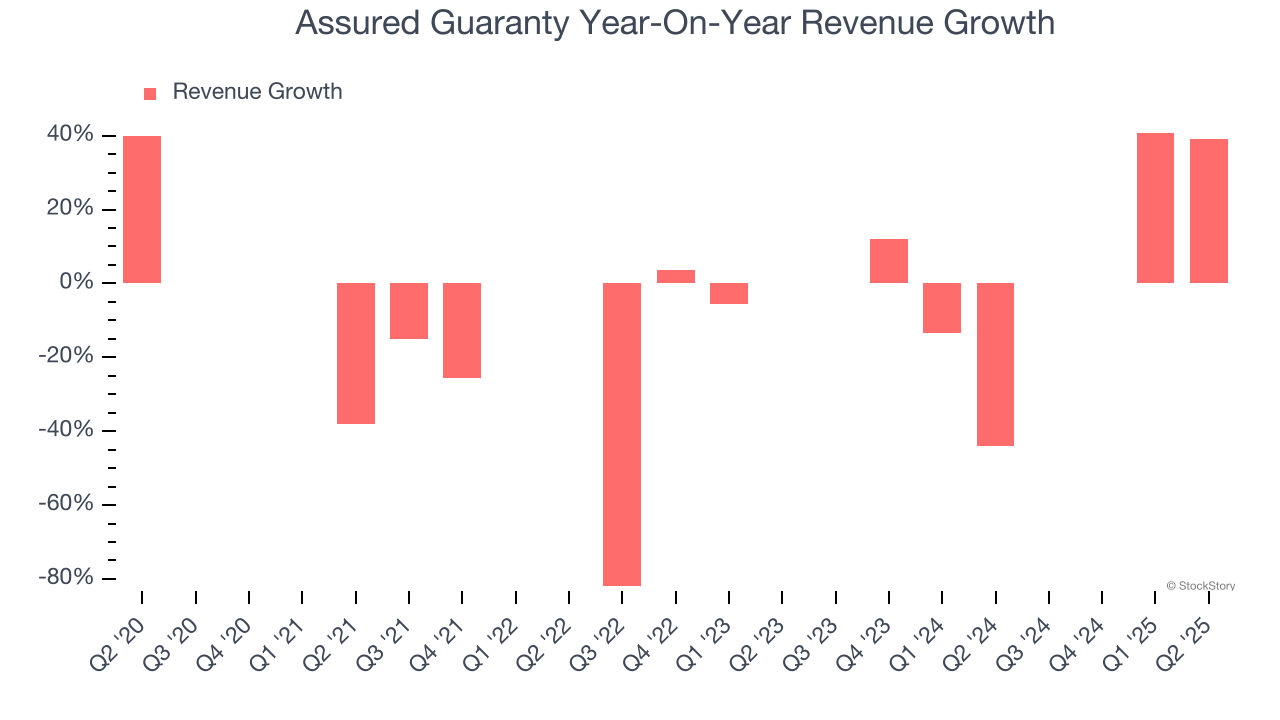

Financial guaranty insurer Assured Guaranty (NYSE:AGO) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 39.1% year on year to $281 million. Its non-GAAP profit of $1.01 per share was 36.6% below analysts’ consensus estimates.

Is now the time to buy Assured Guaranty? Find out by accessing our full research report, it’s free.

Assured Guaranty (AGO) Q2 CY2025 Highlights:

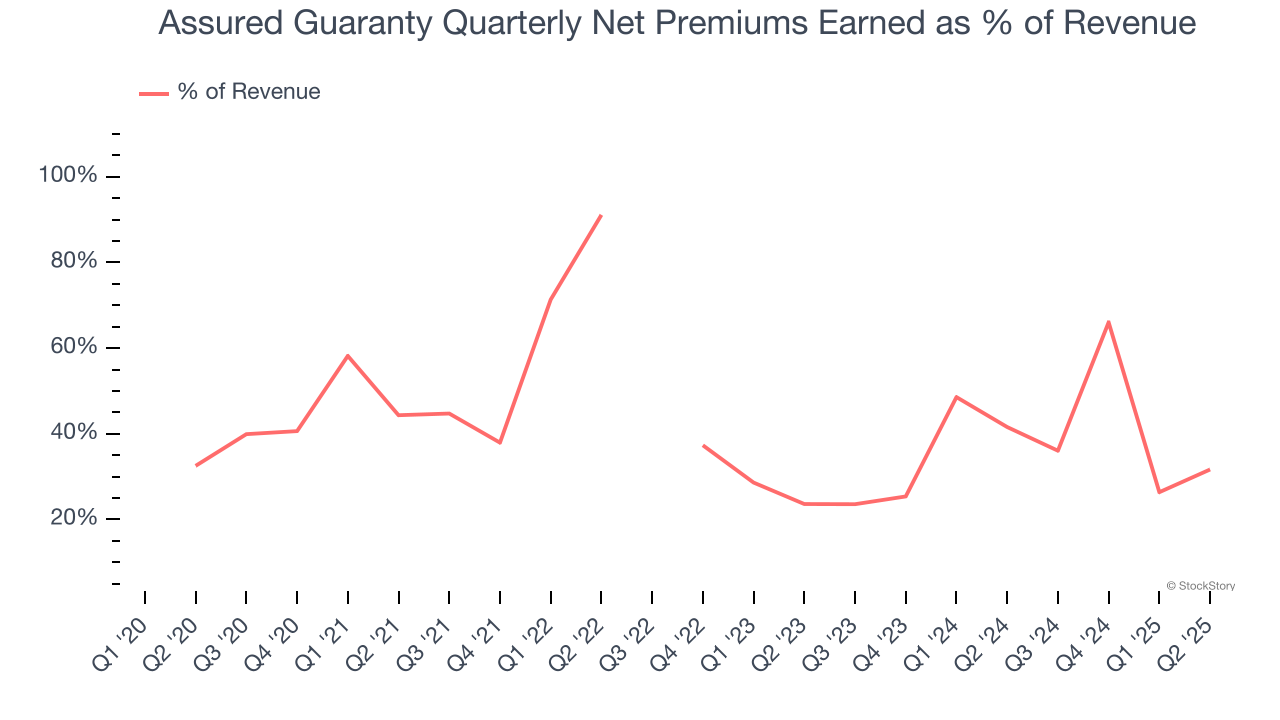

- Net Premiums Earned: $89 million vs analyst estimates of $91 million (6% year-on-year growth, 2.2% miss)

- Revenue: $281 million vs analyst estimates of $185.8 million (39.1% year-on-year growth, 51.2% beat)

- Pre-Tax Profit Margin: 47.3% (flat year on year)

- Adjusted EPS: $1.01 vs analyst expectations of $1.59 (36.6% miss)

- Market Capitalization: $4.14 billion

“Assured Guaranty’s shareholder value increased again in the first half of 2025,” said Dominic Frederico, President and CEO.

Company Overview

Serving as a financial safety net for over $11 trillion in debt service payments since its founding in 2003, Assured Guaranty (NYSE:AGO) provides credit protection products that guarantee scheduled payments on municipal bonds, infrastructure projects, and structured finance obligations.

Revenue Growth

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

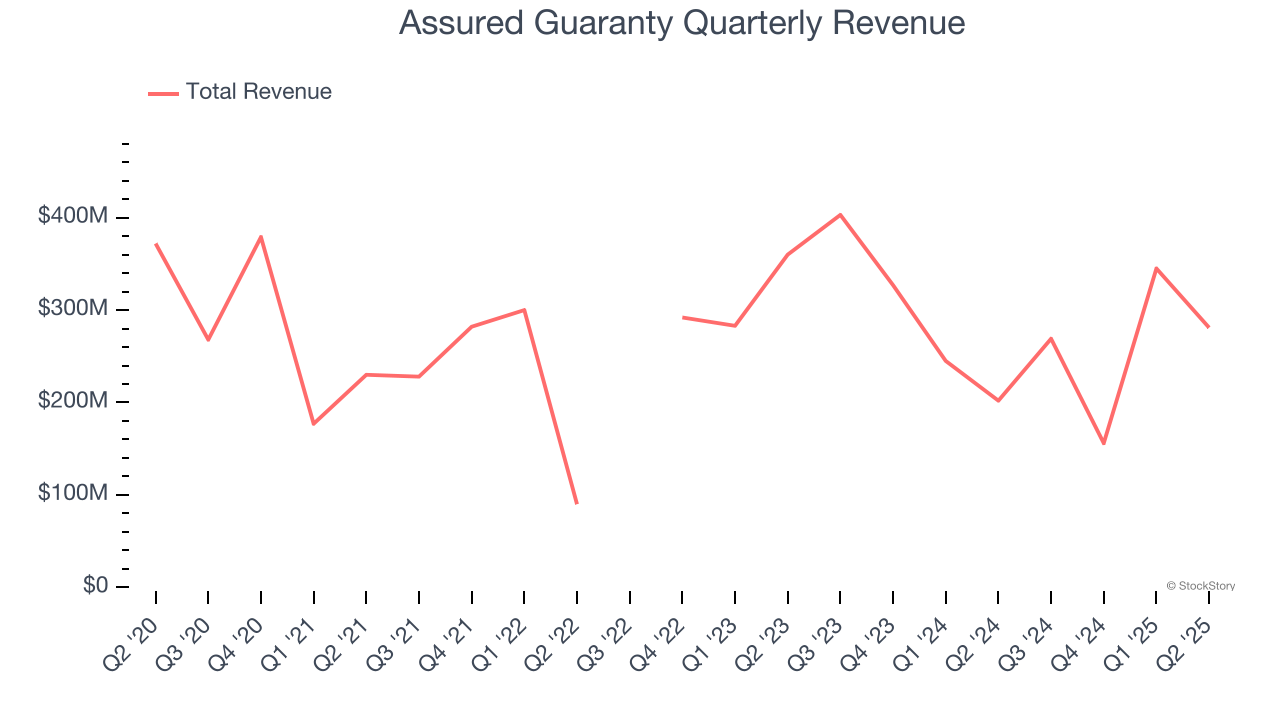

Unfortunately, Assured Guaranty’s 1.6% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks and is a poor baseline for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Assured Guaranty’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8.5% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Assured Guaranty reported wonderful year-on-year revenue growth of 39.1%, and its $281 million of revenue exceeded Wall Street’s estimates by 51.2%.

Net premiums earned made up 40.6% of the company’s total revenue during the last five years, meaning Assured Guaranty’s growth drivers strike a balance between insurance and non-insurance activities.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

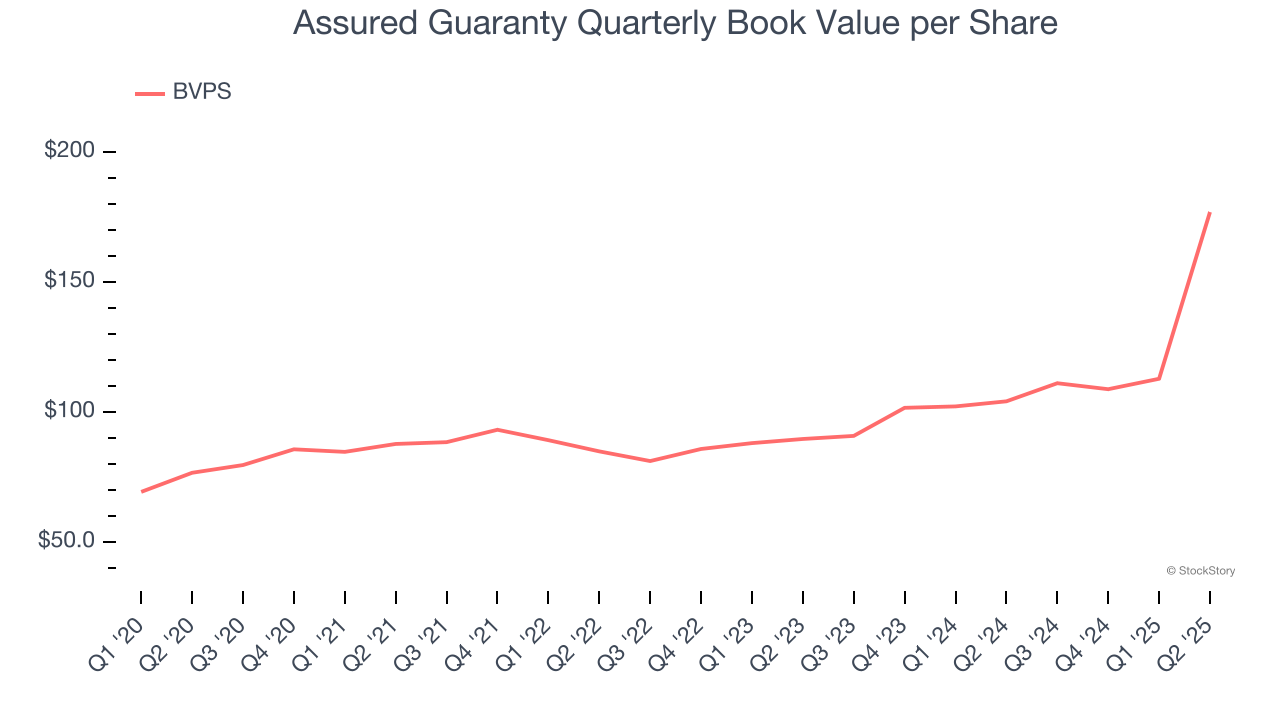

Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Assured Guaranty’s BVPS grew at an incredible 18.2% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 40.4% annually over the last two years from $89.71 to $176.95 per share.

Key Takeaways from Assured Guaranty’s Q2 Results

We were impressed by how significantly Assured Guaranty blew past analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its net premiums earned fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $84.44 immediately following the results.

Assured Guaranty’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10