Earnings Miss: WillScot Holdings Corporation Missed EPS By 27% And Analysts Are Revising Their Forecasts

It's been a mediocre week for WillScot Holdings Corporation (NASDAQ:WSC) shareholders, with the stock dropping 20% to US$25.33 in the week since its latest quarterly results. Statutory earnings per share fell badly short of expectations, coming in at US$0.26, some 27% below analyst forecasts, although revenues were okay, approximately in line with analyst estimates at US$589m. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10bn in marketcap - there is still time to get in early.

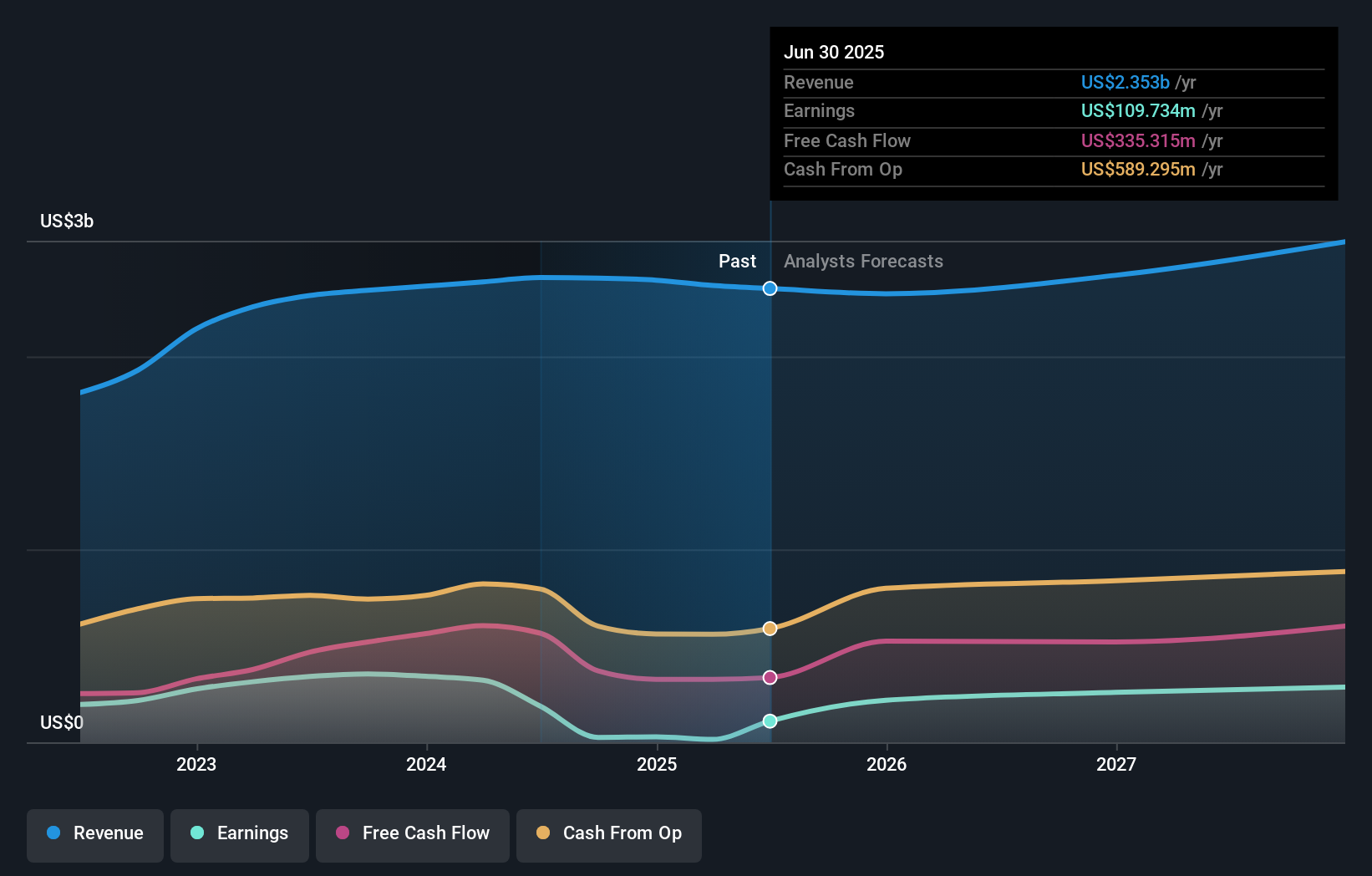

Following last week's earnings report, WillScot Holdings' nine analysts are forecasting 2025 revenues to be US$2.32b, approximately in line with the last 12 months. Statutory earnings per share are predicted to jump 101% to US$1.21. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$2.36b and earnings per share (EPS) of US$1.54 in 2025. So there's definitely been a decline in sentiment after the latest results, noting the large cut to new EPS forecasts.

See our latest analysis for WillScot Holdings

The consensus price target held steady at US$34.33, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic WillScot Holdings analyst has a price target of US$40.00 per share, while the most pessimistic values it at US$29.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that revenue is expected to reverse, with a forecast 2.3% annualised decline to the end of 2025. That is a notable change from historical growth of 14% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.8% annually for the foreseeable future. It's pretty clear that WillScot Holdings' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for WillScot Holdings. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that WillScot Holdings' revenue is expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for WillScot Holdings going out to 2027, and you can see them free on our platform here..

It is also worth noting that we have found 3 warning signs for WillScot Holdings (1 is significant!) that you need to take into consideration.

Valuation is complex, but we're here to simplify it.

Discover if WillScot Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10