MMG Limited Recorded A 12% Miss On Revenue: Analysts Are Revisiting Their Models

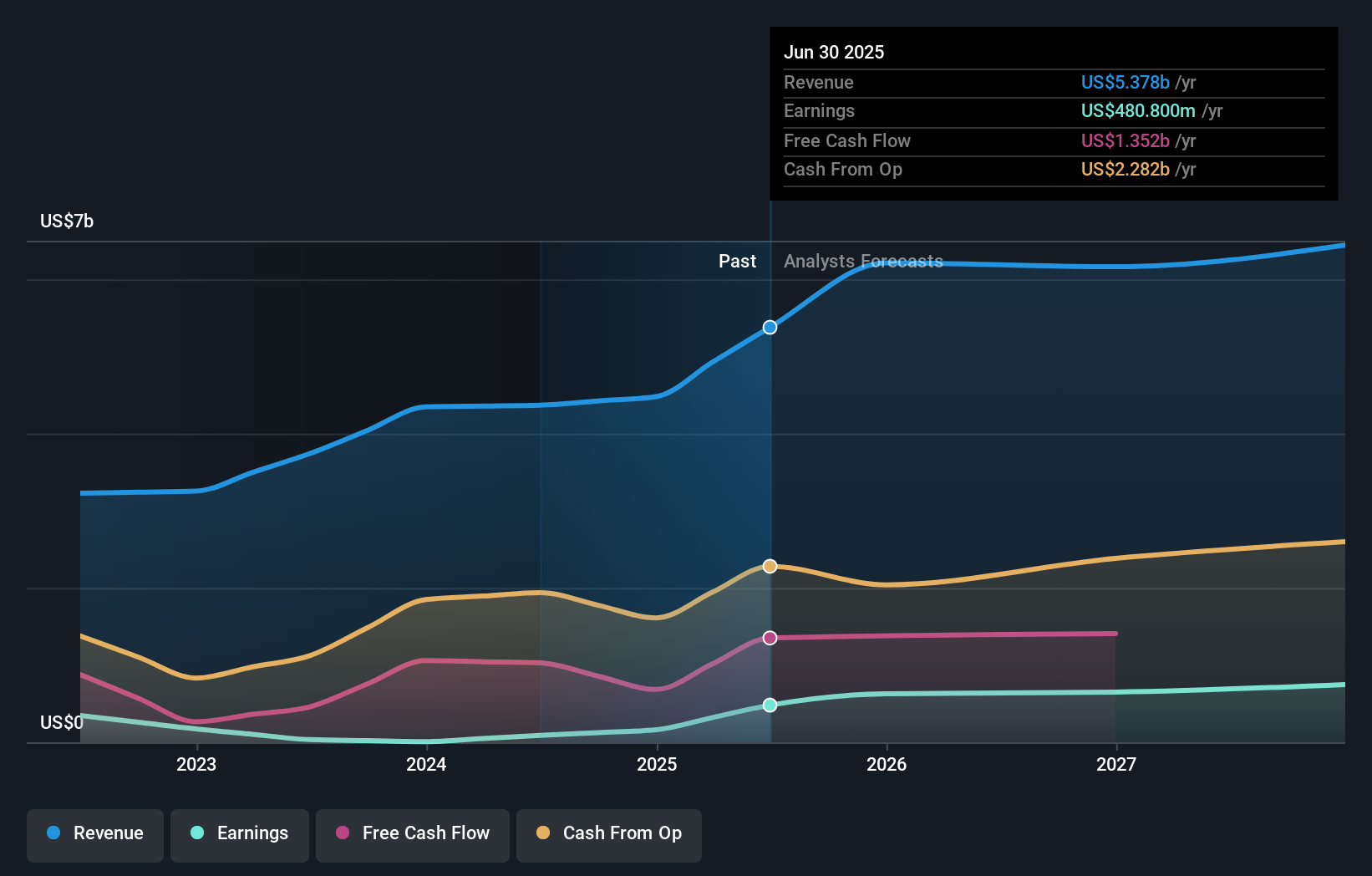

The investors in MMG Limited's (HKG:1208) will be rubbing their hands together with glee today, after the share price leapt 21% to HK$4.99 in the week following its half-year results. Revenues were US$2.8b, 12% below analyst expectations, although losses didn't appear to worsen significantly, with a statutory per-share loss of US$0.015 being in line with what the analysts anticipated. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Trump has pledged to "unleash" American oil and gas and these 15 US stocks have developments that are poised to benefit.

Taking into account the latest results, the current consensus from MMG's eleven analysts is for revenues of US$6.21b in 2025. This would reflect a notable 16% increase on its revenue over the past 12 months. Per-share earnings are expected to jump 26% to US$0.05. Before this earnings report, the analysts had been forecasting revenues of US$5.89b and earnings per share (EPS) of US$0.039 in 2025. There's been a pretty noticeable increase in sentiment, with the analysts upgrading revenues and making a great increase in earnings per share in particular.

See our latest analysis for MMG

With these upgrades, we're not surprised to see that the analysts have lifted their price target 5.9% to HK$4.39per share. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on MMG, with the most bullish analyst valuing it at HK$5.49 and the most bearish at HK$3.19 per share. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely different views on what kind of performance this business can generate. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that MMG's rate of growth is expected to accelerate meaningfully, with the forecast 33% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 8.5% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 5.2% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect MMG to grow faster than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards MMG following these results. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for MMG going out to 2027, and you can see them free on our platform here..

You should always think about risks though. Case in point, we've spotted 1 warning sign for MMG you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10