Summary: Oracle will report its Q2 FY2026 results after market close on December 10. This earnings release will serve as a key indicator for the AI-driven market sentiment in U.S. stocks.

Q1 Review

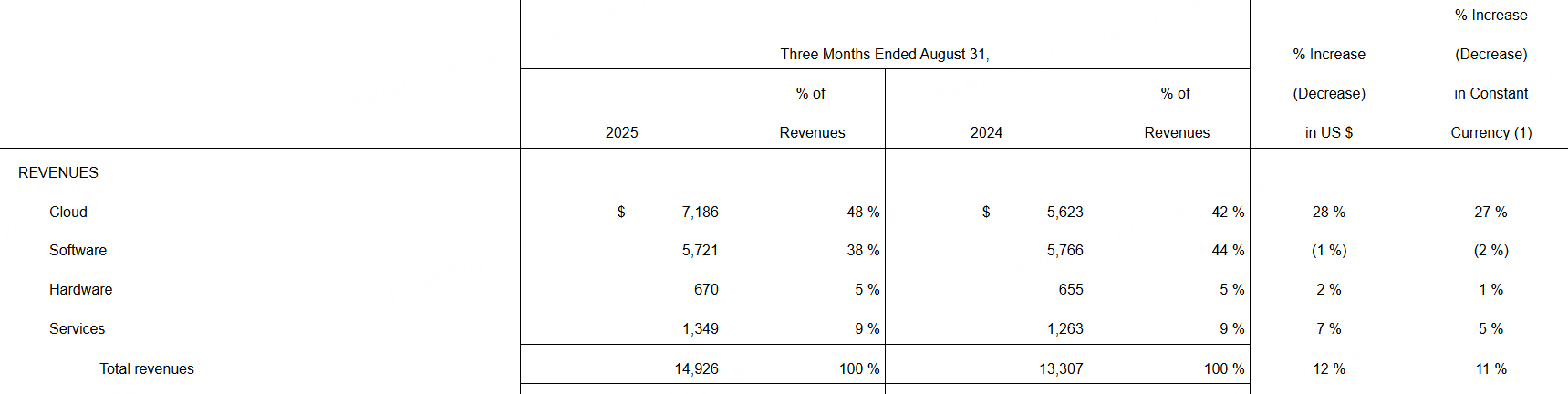

In Q1 FY2026, Oracle's remaining performance obligations reached $455 billion, growing 359% both in USD terms and at constant currency. GAAP EPS decreased 2% to $1.01, while non-GAAP EPS increased 6% to $1.47.

Total Q1 revenue was $14.9 billion, up 12% in USD and 11% at constant currency. Cloud revenue (IaaS + SaaS) totaled $7.2 billion, increasing 28% in USD and 27% at constant currency. Cloud Infrastructure (IaaS) revenue grew 55% in USD (54% cc) to $3.3 billion, while Cloud Applications (SaaS) revenue rose 11% in USD (10% cc) to $3.8 billion.

Q2 Expectations

According to Tiger Trade, analysts generally expect Oracle's Q2 total revenue to reach $16.22 billion, a 15.36% YoY increase. EPS is projected at $1.637 (up 11.37% YoY), with EBIT expected at $6.794 billion.

Quarterly Outlook

AI Computing Power Driving Cloud Demand

Recent computing power expansion for AI training and inference has accelerated Oracle's cloud and software order backlog and delivery pace. Market participants widely link this quarter's revenue and EPS growth to AI demand intensity. Last quarter's "cloud and on-premise software" revenue reached $12.907 billion, demonstrating core business resilience and improved customer stickiness. Continued AI customer demand for inference and training this quarter would drive double-digit revenue growth through increased purchases of IaaS/PaaS and related software licenses.

Gross margin stood at 67.28% last quarter, supported by economies of scale and higher-margin software revenue. Should cloud revenue continue gaining share while hardware/service revenue remains stable, overall gross margin could maintain relative robustness. However, to meet large customer delivery cycles and data center capex, operating expenses and depreciation/amortization may increase temporarily. The pace of net margin improvement depends on expense dilution from scaling.

Risks include potential delays in large-order deployment and supply-side resource coordination, which could postpone revenue/profit recognition. Should market skepticism about AI investment returns intensify, short-term stock price and valuation elasticity may be affected, though long-term fundamentals remain strengthened by the order backlog.

Software License & Support: The Cash Flow Stabilizer

Oracle's software license and support business has historically stabilized cash flow and profits. Last quarter's cloud and on-premise software scale demonstrated renewal and upsell stability. Amid macroeconomic uncertainties, existing customers' maintenance and upgrade needs for critical databases and application suites continue to support earnings quality.

Adjusted EPS is expected at $1.637 (up ~10.59% YoY). Should license/support revenue remain stable while cloud revenue structurally improves, EPS growth would gain sustainability. Key focus remains on whether revenue growth sufficiently offsets increased investment intensity and depreciation to prevent margin compression.

As major customers migrate to AI applications, demand for database/middleware performance and elasticity rises. Oracle's product portfolio and enterprise service capabilities position it to capture this incremental demand, supporting steady revenue and profit improvement.

Data Center and Capital Expenditure Balance

Amid market caution regarding AI infrastructure payback periods, Oracle must balance computing/storage resource expansion with capital efficiency and debt structure stability. Last quarter's 19.61% net margin reflected solid profitability, though sequential decline warrants investor attention to investment pacing and expense management.

Should revenue reach ~$16.2 billion, scale effects could dilute fixed costs. However, if capital-intensive investments accelerate to fulfill hyperscale customer deliveries, the slope of net margin recovery would still depend on order-to-revenue conversion speed. Management's commentary on capacity expansion, contract obligations, and margin trajectory will be crucial for market interpretation.

Amid intensifying competition, Oracle's differentiated pricing and integrated software/database ecosystem may help retain enterprise clients. Announcements of partnerships with leading AI firms during the quarter could bolster confidence in long-term growth prospects.

Analyst Views

Recent institutional focus centers on AI-related order fulfillment and target price adjustments. Multiple reports note that while Oracle's cloud/software revenue benefits from rising computing/network equipment demand from major AI clients, margin progression remains subject to capex and delivery cycles. Some analysts maintain cautious optimism ahead of earnings, suggesting targets may hold or see modest increases if guidance continues double-digit revenue growth and stable adjusted EPS expansion. Should management emphasize capital investment expansion with slower margin improvement, certain institutions might lower targets or adopt wait-and-see stances.

Overall, market divergence centers on order fulfillment velocity and margin recovery path. This quarter's revenue guidance and margin outlook will dictate subsequent target price adjustments.