Waystar Holding Corp. (NASDAQ:WAY) About To Shift From Loss To Profit

Waystar Holding Corp. (NASDAQ:WAY) is possibly approaching a major achievement in its business, so we would like to shine some light on the company. Waystar Holding Corp. develops a cloud-based software solution for healthcare payments. The US$6.9b market-cap company posted a loss in its most recent financial year of US$51m and a latest trailing-twelve-month loss of US$53m leading to an even wider gap between loss and breakeven. Many investors are wondering about the rate at which Waystar Holding will turn a profit, with the big question being “when will the company breakeven?” In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

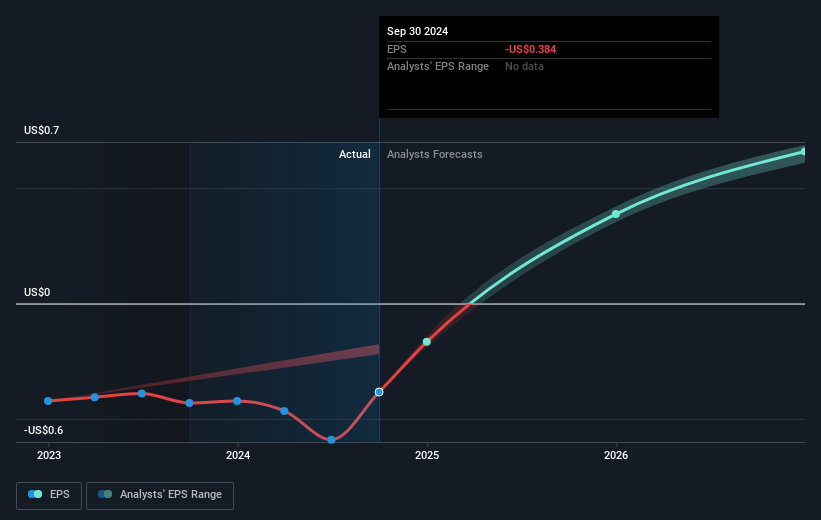

Check out our latest analysis for Waystar Holding

According to the 8 industry analysts covering Waystar Holding, the consensus is that breakeven is near. They expect the company to post a final loss in 2024, before turning a profit of US$71m in 2025. Therefore, the company is expected to breakeven roughly 12 months from now or less. At what rate will the company have to grow in order to realise the consensus estimates forecasting breakeven in under 12 months? Using a line of best fit, we calculated an average annual growth rate of 117%, which signals high confidence from analysts. Should the business grow at a slower rate, it will become profitable at a later date than expected.

We're not going to go through company-specific developments for Waystar Holding given that this is a high-level summary, though, take into account that generally healthcare tech companies, depending on the stage of product development, have irregular periods of cash flow. This means, large upcoming growth rates are not abnormal as the company is beginning to reap the benefits of earlier investments.

Before we wrap up, there’s one issue worth mentioning. Waystar Holding currently has a relatively high level of debt. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in Waystar Holding's case is 41%. A higher level of debt requires more stringent capital management which increases the risk in investing in the loss-making company.

Next Steps:

There are key fundamentals of Waystar Holding which are not covered in this article, but we must stress again that this is merely a basic overview. For a more comprehensive look at Waystar Holding, take a look at Waystar Holding's company page on Simply Wall St. We've also compiled a list of essential aspects you should look at:

- Valuation: What is Waystar Holding worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Waystar Holding is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Waystar Holding’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

Valuation is complex, but we're here to simplify it.

Discover if Waystar Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10