We're Keeping An Eye On Golden Faith Group Holdings' (HKG:2863) Cash Burn Rate

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should Golden Faith Group Holdings (HKG:2863) shareholders be worried about its cash burn? In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

How Long Is Golden Faith Group Holdings' Cash Runway?

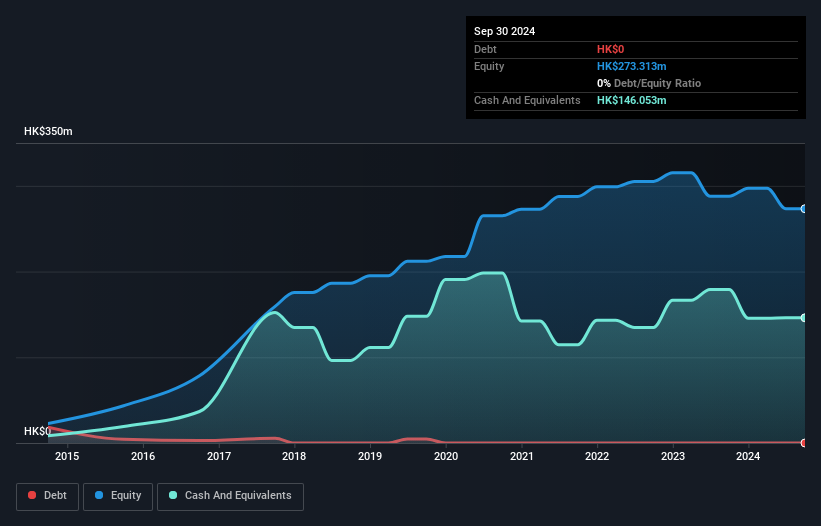

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In September 2024, Golden Faith Group Holdings had HK$146m in cash, and was debt-free. Importantly, its cash burn was HK$39m over the trailing twelve months. That means it had a cash runway of about 3.7 years as of September 2024. There's no doubt that this is a reassuringly long runway. Depicted below, you can see how its cash holdings have changed over time.

See our latest analysis for Golden Faith Group Holdings

How Well Is Golden Faith Group Holdings Growing?

It was quite stunning to see that Golden Faith Group Holdings increased its cash burn by 4,953% over the last year. That does give us pause, and we can't take much solace in the operating revenue growth of 9.7% in the same time frame. In light of the above-mentioned, we're pretty wary of the trajectory the company seems to be on. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how Golden Faith Group Holdings has developed its business over time by checking this visualization of its revenue and earnings history .

How Hard Would It Be For Golden Faith Group Holdings To Raise More Cash For Growth?

Golden Faith Group Holdings seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of HK$220m, Golden Faith Group Holdings' HK$39m in cash burn equates to about 18% of its market value. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is Golden Faith Group Holdings' Cash Burn A Worry?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Golden Faith Group Holdings' cash runway was relatively promising. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Golden Faith Group Holdings' situation. Separately, we looked at different risks affecting the company and spotted 3 warning signs for Golden Faith Group Holdings (of which 2 don't sit too well with us!) you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10