Is Sky Light Holdings (HKG:3882) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Sky Light Holdings Limited (HKG:3882) makes use of debt. But should shareholders be worried about its use of debt?

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

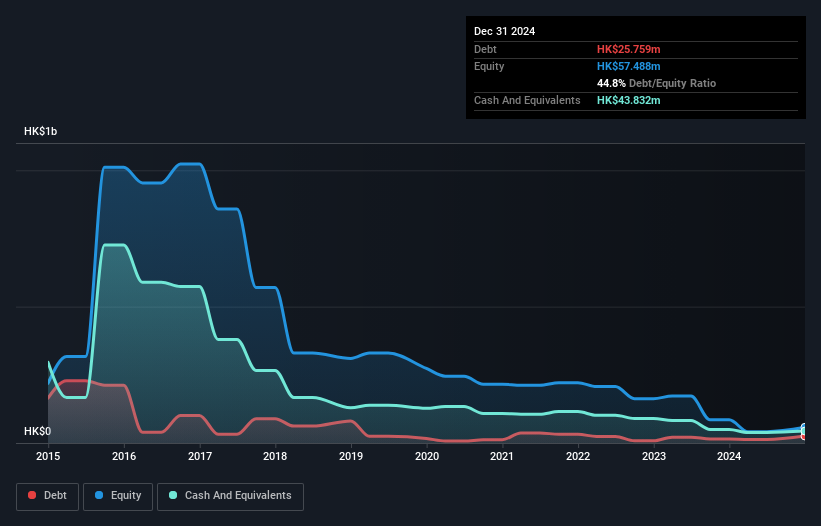

What Is Sky Light Holdings's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2024 Sky Light Holdings had HK$25.8m of debt, an increase on HK$14.7m, over one year. But on the other hand it also has HK$43.8m in cash, leading to a HK$18.1m net cash position.

How Strong Is Sky Light Holdings' Balance Sheet?

The latest balance sheet data shows that Sky Light Holdings had liabilities of HK$189.1m due within a year, and liabilities of HK$9.30m falling due after that. Offsetting these obligations, it had cash of HK$43.8m as well as receivables valued at HK$70.0m due within 12 months. So it has liabilities totalling HK$84.6m more than its cash and near-term receivables, combined.

Since publicly traded Sky Light Holdings shares are worth a total of HK$897.6m, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Sky Light Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Sky Light Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Check out our latest analysis for Sky Light Holdings

Over 12 months, Sky Light Holdings made a loss at the EBIT level, and saw its revenue drop to HK$296m, which is a fall of 7.9%. We would much prefer see growth.

So How Risky Is Sky Light Holdings?

Although Sky Light Holdings had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of HK$7.3m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. With revenue growth uninspiring, we'd really need to see some positive EBIT before mustering much enthusiasm for this business. For riskier companies like Sky Light Holdings I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10