Hyster-Yale Materials Handling (HY) Q1 Earnings: What To Expect

Lift truck and material handling solutions manufacturer Hyster-Yale Materials Handling (NYSE:HY) will be announcing earnings results tomorrow after the bell. Here’s what to expect.

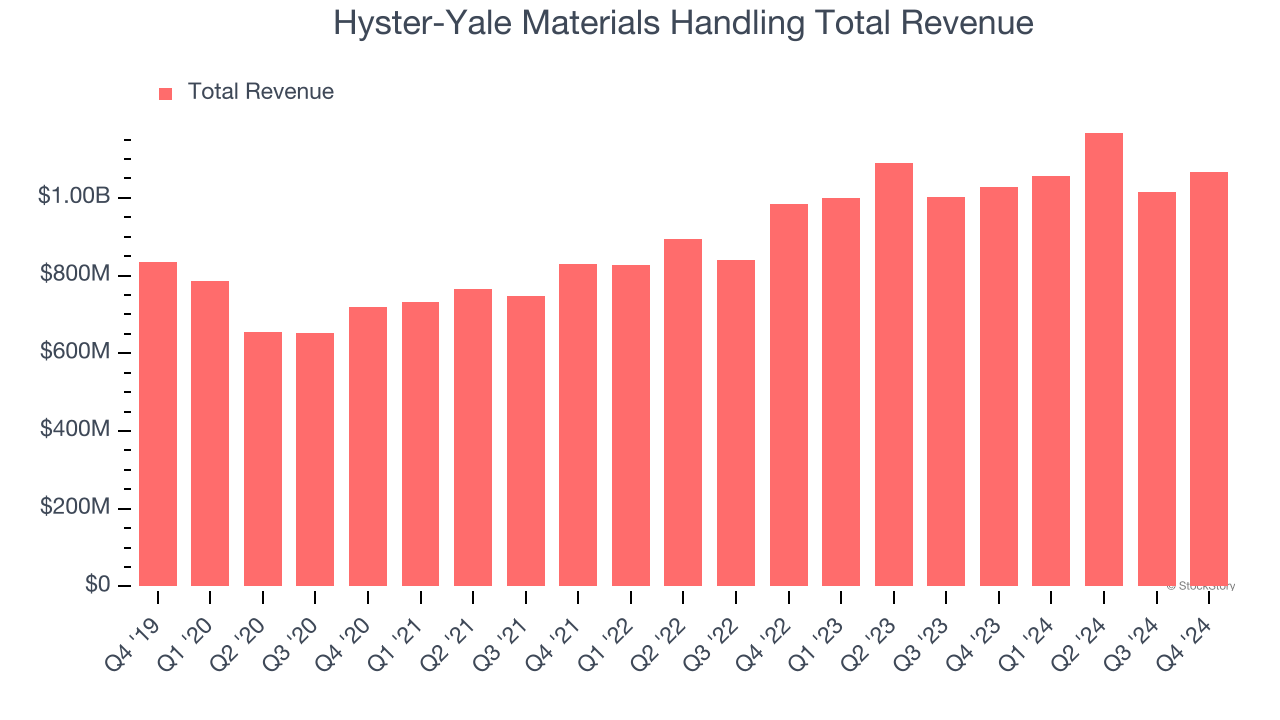

Hyster-Yale Materials Handling beat analysts’ revenue expectations by 4.4% last quarter, reporting revenues of $1.07 billion, up 3.9% year on year. It was an exceptional quarter for the company, with a solid beat of analysts’ EBITDA estimates and a decent beat of analysts’ EPS estimates.

Is Hyster-Yale Materials Handling a buy or sell going into earnings? Read our full analysis here, it’s free.

This quarter, analysts are expecting Hyster-Yale Materials Handling’s revenue to decline 10.3% year on year to $947.8 million, a reversal from the 5.7% increase it recorded in the same quarter last year. Adjusted earnings are expected to come in at $0.49 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Hyster-Yale Materials Handling has only missed Wall Street’s revenue estimates once over the last two years, exceeding top-line expectations by 4.6% on average.

Looking at Hyster-Yale Materials Handling’s peers in the professional tools and equipment segment, some have already reported their Q1 results, giving us a hint as to what we can expect. ESAB’s revenues decreased 1.7% year on year, beating analysts’ expectations by 2.2%, and Hillman reported revenues up 2.6%, falling short of estimates by 0.5%. ESAB traded up 3.1% following the results while Hillman was down 7.5%.

Read our full analysis of ESAB’s results here and Hillman’s results here.

There has been positive sentiment among investors in the professional tools and equipment segment, with share prices up 13% on average over the last month. Hyster-Yale Materials Handling is up 11.3% during the same time and is heading into earnings with an average analyst price target of $72.50 (compared to the current share price of $40.33).

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10