With a 54% Gain in 2025, This Artificial Intelligence (AI) Stock Is Crushing the S&P 500. Is It Too Late to Buy?

-

The S&P 500 is in the red for the year amid as Trump's trade war heats up.

-

Duolingo stock is up 54% year to date, as the company's digital subscriptions aren't subject to tariffs.

-

The stock trades at a premium valuation right now.

The S&P 500 (SNPINDEX: ^GSPC) is off to a bumpy start to 2025. It slumped to a low of 19% below its peak after President Donald Trump announced his "Liberation Day" tariffs on goods from nearly every country in the world in early April, but it has since rebounded somewhat. It's now down by just 8% or so from its high, and off by around 4% year to date.

But some companies' stocks barely skipped a beat -- primarily those that aren't directly affected by Trump's global trade war, which mainly targets imported physical goods. Duolingo (DUOL 1.87%) operates the world's most popular digital language education platform, and tariffs don't apply to its subscriptions. The company continues to grow rapidly, which has propelled its stock to an eye-popping 54% gain in 2025 so far.

Duolingo just raised its full-year revenue guidance, but can the stock continue its run-up, or is it too late to buy?

Image source: Getty Images.

Accelerating user growth

Duolingo has developed a highly engaging and interactive mobile application that places a powerful learning experience at the fingertips of anyone with a smartphone. It's clearly resonating: The platform had 130.2 million monthly active users (MAU) as of the end of the first quarter, a 33% increase from a year earlier. Its growth rate actually accelerated from 32% in the fourth quarter.

Duolingo monetizes its app in two ways: It shows ads to free users, and it offers paid subscription options that unlock additional features to help users accelerate their learning. The platform had a record 10.3 million paying subscribers at the end of Q1, which was a 40% increase year over year. Since the subscriber base is growing faster than Duolingo's overall active user base, it suggests users see real value in paying for those extra features.

Artificial intelligence (AI) is becoming an important source of that value. Duolingo's most expensive subscription tier is called Max, and it offers three powerful AI features:

- Roleplay: This feature offers an AI chatbot interface to help users practice their conversational skills in the language of their choice.

- Explain My Answer: This tool provides personalized feedback to each user based on their mistakes in each lesson.

- Video Call: Duolingo created a digital avatar named Lily that helps users practice their speaking skills. Lily can hold conversations on almost any topic, and even remembers previous interactions to provide users with a highly personalized experience.

Duolingo's long-term goal is to deliver a learning experience that rivals that of studying with a human tutor, and AI has brought the company closer to achieving it than ever before. The Max subscription was only launched in 2023 (and the Video Call feature late last year) yet it already represented 7% of Duolingo's total subscriber base at the end of Q1, up from 5% just three months earlier.

Duolingo just raised its revenue forecast for 2025

Duolingo generated $230.7 million in revenue during the first quarter. That was a 38% year-over-year increase, and comfortably above the $223.5 million that was the high end of management's forecast range.

The strong result prompted management to increase its forecast for the year: It now expects the company to generate up to $996 million in revenue (at the high end of the guidance range), compared to $978.5 million previously. This is one of the key reasons the stock has gained 25% since Duolingo released its Q1 report.

Another reason is the company's soaring profitability. Duolingo's total operating expenses came in at $140.5 million during the first quarter, an increase of 32% compared to the year-ago period. Since its costs grew at a slower pace than its revenue, more money flowed to the bottom line. As a result, its net income jumped by 30% to $35.1 million.

Duolingo's marketing strategy relies heavily on organic campaigns across social media, so it doesn't spend much money to acquire new users. In fact, marketing was the company's smallest operating cost during Q1, coming in at just $26.6 million. This strategy allows management to direct more money toward research and development to create new features, which are a big driver of monetization.

Is it too late to buy Duolingo stock?

Duolingo's business is firing on all cylinders right now. Plus, its digital subscriptions won't be directly impacted by tariffs, and the company operates in 194 countries, so it has a diversified revenue base that could offer some insulation from the economic impacts of global trade tensions. But that doesn't necessarily mean the stock is a good buy right now.

Its 54% gain this year -- and its 151% surge over the past 12 months -- has catapulted it to a lofty valuation. It trades at a price-to-sales (P/S) ratio of 29.5, which is near its highest level since the company went public in 2021. It's also an 87% premium to the stock's average P/S ratio of 15.8 over that period.

DUOL PS Ratio data by YCharts.

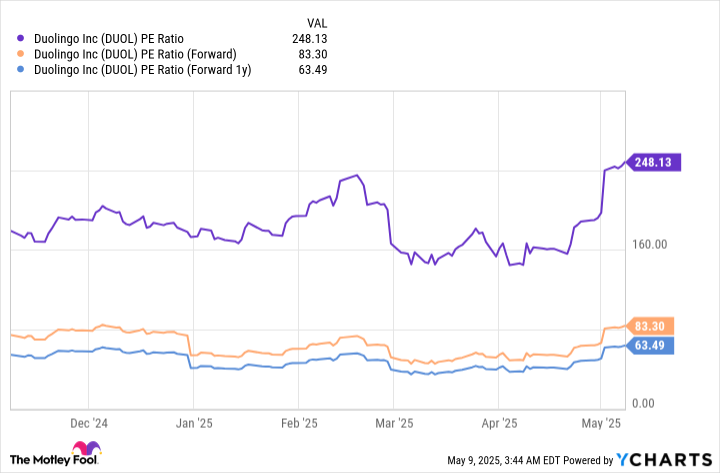

Duolingo stock also trades at an eye-popping price-to-earnings (P/E) ratio of 248. For some perspective, the S&P 500 trades at a P/E ratio of just 22.5.

However, Duolingo is growing quickly, so its valuation looks slightly more reasonable when measured against its future potential earnings. According to Wall Street's consensus estimate (provided by Yahoo! Finance), the company could deliver earnings of $6.05 per share in 2025, and $7.93 per share in 2026. That gives its stock forward P/E ratios of 83 and 63, respectively, for those years.

DUOL PE Ratio data by YCharts.

Don't get me wrong: The stock is still wildly expensive even on a forward basis, so it probably isn't a good buy right now for investors with a short-term time horizon. However, patient investors who are willing to hold the stock for at least the next five years (but preferably longer) could do extremely well as catalysts like AI and the Max subscription mature.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10