Micron Technology: Smart Investment or Risky Bet in 2025?

-

Micron’s stock is still 33% below last summer’s all-time highs despite playing an active role in the artificial intelligence (AI) boom.

-

The company's new memory chips will power Nvidia’s next-gen AI accelerators in 2026.

-

Long-term investors may find this dip a good entry point, even if the ride stays bumpy.

Memory chip giant Micron Technology (MU 4.11%) is back to its cyclical habits. One might think that the artificial intelligence (AI) boom would send Micron's business results and stock returns skyward these days, but the real AI effect isn't quite that simple.

As of June 3, Micron's total return stands 33% below last summer's all-time highs. Is this a wide-open buying window or the start of a multiyear downswing?

Here's what I think about Micron in June 2025.

Why Micron isn't flying high in 2025

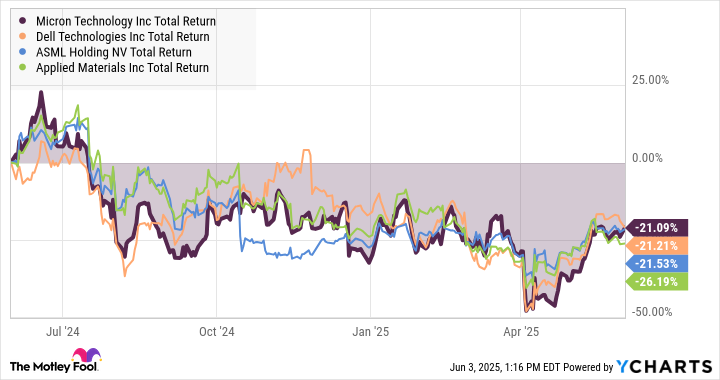

Micron isn't the only AI-oriented tech stock to take a drastic haircut over the last year. It's almost scary how tightly Micron's stock performance has matched the total returns of Dell Technologies, ASML Holding, and Applied Materials recently:

MU Total Return Level data by YCharts

For the record, AI-centric market darling Nvidia gained 25% over the same period, while the S&P 500 (^GSPC 0.22%) market index rose by 14%. So the sinking tide didn't capsize every boat, but it did weigh on most AI-focused computing hardware experts not named Nvidia.

Micron did play a part in its own downfall, of course. Sales soared in the first half of 2024, but slowed down more recently. Mind you, many businesses would celebrate a 38% year-over-year revenue jump, like the one Micron reported in March, but that's a significant slowdown from 93% two quarters earlier.

Micron's profits followed similar trend lines, which explains why investors lost patience with the stock. And of course, the proposed tariffs may undermine Micron's sales and profits. Nobody knows how the bubbling trade tensions will play out yet.

Why Micron isn't sweating the slowdown

But here's the thing: Micron is well equipped to handle a bit of a slowdown. If anything, the company's in-house chip factories should be able to stockpile memory chips until its largest customers are ready to place large orders again.

On top of that, Micron offers market-leading technology. Its next generation of power-efficient data center memory will hit the market in 2026, offering a 60% memory bandwidth increase and even lower power consumption than the current top-of-the-line products. These high-bandwidth chips are a part of Nvidia's latest and greatest AI accelerator cards, so Micron benefits in a very direct way from Nvidia's success.

Image source: Getty Images.

Is Micron's stock just taking a breather?

So Micron remains a top-notch provider of crucial hardware in the generative AI revolution. A short-term slowdown in the order book is not the end of the line.

Meanwhile, Micron's stock is trading at just 9.4 times forward earnings estimates. Analysts expect the company's profits to surge in 2025, and for good reason. Yet the market makers out there have not yet accounted for this upcoming bottom-line explosion in their share price calculations.

The AI boom makes a real difference to Micron's business prospects, and sales of those low-power but high-performance data center chips should rise from $1 billion last year to "multibillion dollars" in 2025. This surge should also be good for Micron's profit margins, since I'm talking about high-end chips with lucrative unit prices.

The speed bump simply gives long-term investors another chance to buy Micron shares on the cheap. The long-term returns won't be smooth, but Micron tends to build wealth over its sweeping business cycles. I highly recommend holding a few Micron shares for the long haul.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10