Top Growth Stocks With High Insider Ownership July 2025

The United States market has shown positive momentum recently, with a 2.1% increase over the last week and a 14% rise in the past year, as all sectors have gained ground. In light of these strong market conditions and an anticipated annual earnings growth of 15%, stocks with high insider ownership can be particularly appealing as they often indicate confidence from those closest to the company's operations and potential for sustained growth.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Zapp Electric Vehicles Group (ZAPP.F) | 16.1% | 170.8% |

| Super Micro Computer (SMCI) | 13.9% | 39.1% |

| Ryan Specialty Holdings (RYAN) | 15.6% | 95.3% |

| Prairie Operating (PROP) | 34.6% | 92.4% |

| FTC Solar (FTCI) | 28.3% | 62.5% |

| Enovix (ENVX) | 12.1% | 58.4% |

| Credo Technology Group Holding (CRDO) | 11.9% | 45% |

| Atour Lifestyle Holdings (ATAT) | 21.8% | 23.7% |

| Astera Labs (ALAB) | 13.1% | 44.4% |

| ARS Pharmaceuticals (SPRY) | 14.3% | 63.1% |

Click here to see the full list of 188 stocks from our Fast Growing US Companies With High Insider Ownership screener.

Underneath we present a selection of stocks filtered out by our screen.

Astrana Health (ASTH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Astrana Health, Inc. is a healthcare management company offering medical care services in the United States with a market cap of approximately $1.26 billion.

Operations: Astrana Health generates revenue through its segments: Care Delivery ($139.34 million), Care Partners ($2.17 billion), and Care Enablement ($161.74 million).

Insider Ownership: 12.5%

Revenue Growth Forecast: 15.1% p.a.

Astrana Health's revenue is forecast to grow at 15.1% annually, outpacing the US market average, while earnings are expected to rise significantly at 30.8% per year. Despite recent index exclusions and a drop in profit margins, the company remains undervalued by 81.7%. Recent leadership changes aim to bolster its AI-enabled care platform as it scales nationally. A completed share buyback program signals confidence amidst these strategic shifts and financial challenges.

- Click to explore a detailed breakdown of our findings in Astrana Health's earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of Astrana Health shares in the market.

Youdao (DAO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Youdao, Inc. is an internet technology company offering online services in content, community, communication, and commerce sectors in China with a market cap of approximately $1.03 billion.

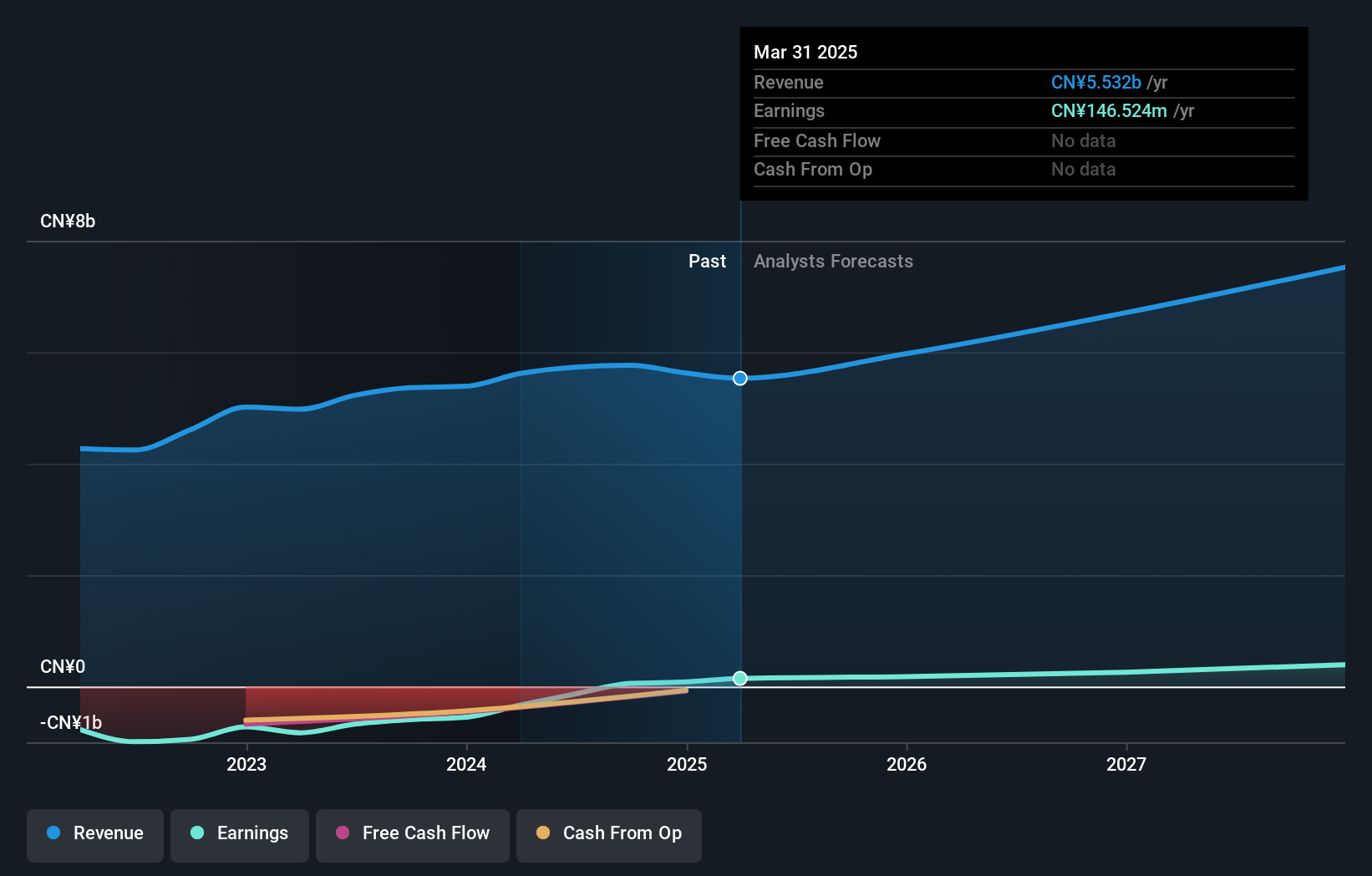

Operations: The company's revenue is primarily derived from Learning Services (CN¥2.63 billion), Online Marketing Services (CN¥1.99 billion), and Smart Devices (CN¥912.97 million).

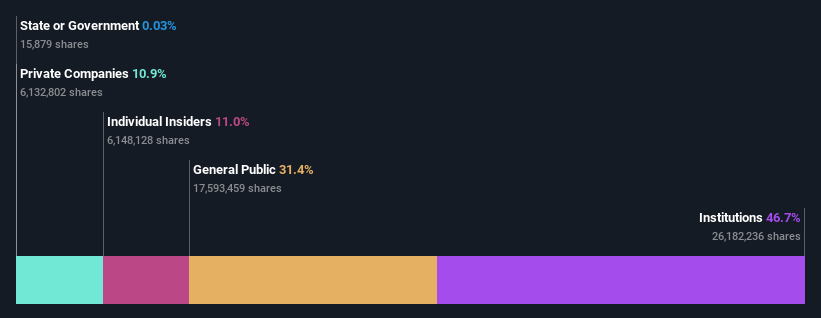

Insider Ownership: 20.4%

Revenue Growth Forecast: 11.3% p.a.

Youdao's revenue is projected to grow at 11.3% annually, surpassing the US market rate, while its earnings are expected to rise significantly at 35.7% per year. The company recently became profitable but faces challenges with negative shareholders' equity and debt coverage by operating cash flow. Despite no recent insider trading activity, Youdao completed a substantial share buyback of 6.19%, reflecting confidence in its growth trajectory amidst financial hurdles.

- Delve into the full analysis future growth report here for a deeper understanding of Youdao.

- Our valuation report here indicates Youdao may be overvalued.

Perfect (PERF)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Perfect Corp. is an artificial intelligence software as a service company offering AI and AR-powered solutions for the beauty, fashion, and skincare industries globally, with a market cap of $257.68 million.

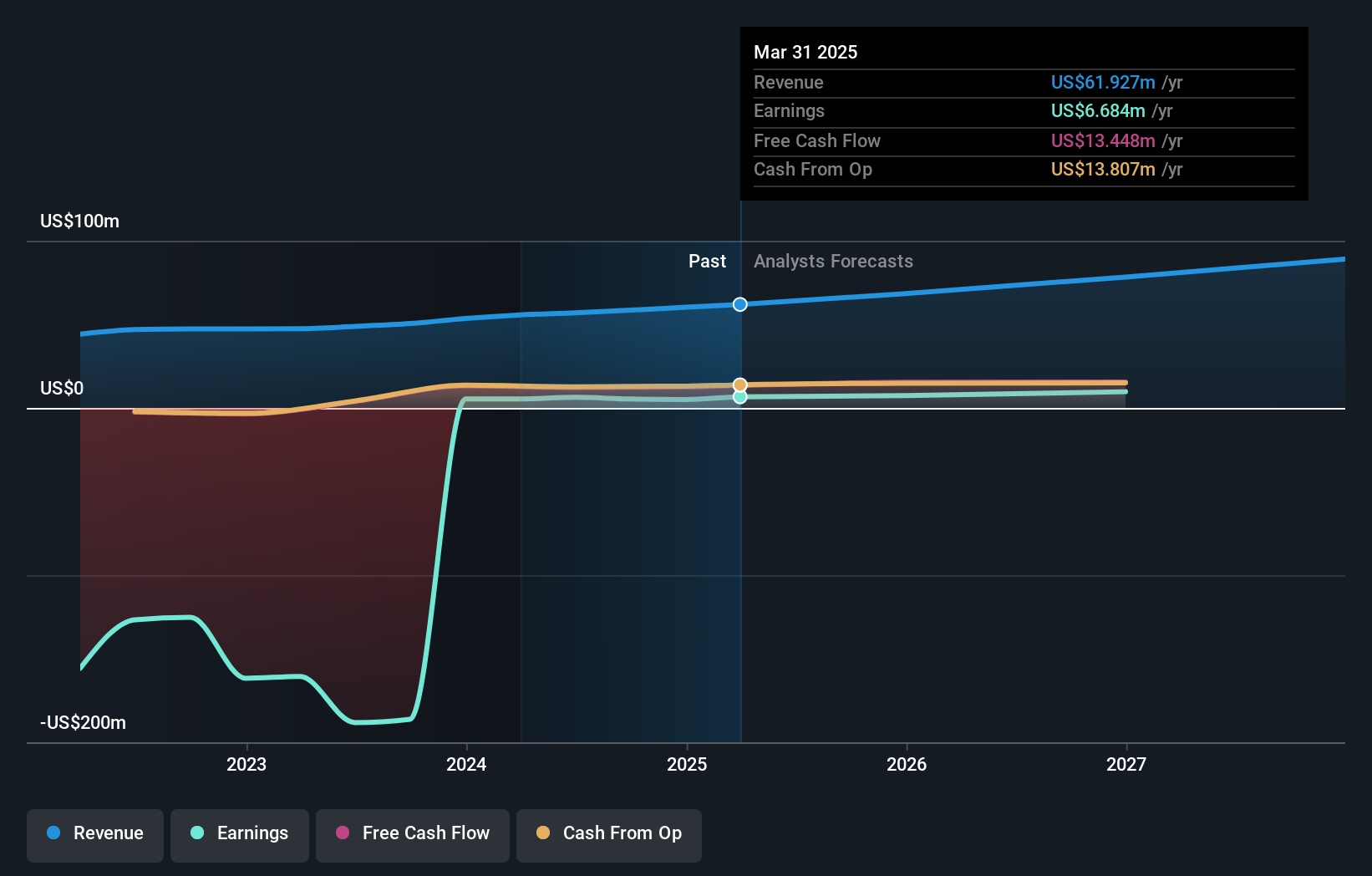

Operations: The company's revenue primarily comes from its Internet Software & Services segment, generating $61.93 million.

Insider Ownership: 23%

Revenue Growth Forecast: 12.9% p.a.

Perfect Corp. is poised for growth with forecasted annual earnings increases of 22.1%, outpacing the US market. Recent strategic partnerships, like its integration with NVIDIA, enhance its AI and AR capabilities, transforming consumer experiences in beauty and fashion through virtual try-ons and AI-driven recommendations. Despite limited insider trading data, Perfect Corp.'s innovative solutions are expected to drive revenue growth at 12.9% annually, supported by recent product launches that address online shopping challenges effectively.

- Dive into the specifics of Perfect here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Perfect is priced higher than what may be justified by its financials.

Next Steps

- Access the full spectrum of 188 Fast Growing US Companies With High Insider Ownership by clicking on this link.

- Contemplating Other Strategies? Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 24 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10