Asian Penny Stocks To Consider In July 2025

As global markets continue to navigate a landscape marked by solid corporate earnings and evolving economic conditions, the Asian market presents its own unique set of opportunities for investors. Penny stocks, often seen as remnants of past trading eras, remain relevant due to their potential for growth and affordability. In this article, we explore three penny stocks in Asia that stand out for their financial strength and potential to offer significant returns.

Top 10 Penny Stocks In Asia

| Name | Share Price | Market Cap | Rewards & Risks |

| Lever Style (SEHK:1346) | HK$1.44 | HK$908.57M | ✅ 4 ⚠️ 1 View Analysis > |

| Ever Sunshine Services Group (SEHK:1995) | HK$2.18 | HK$3.77B | ✅ 4 ⚠️ 2 View Analysis > |

| TK Group (Holdings) (SEHK:2283) | HK$2.45 | HK$2.04B | ✅ 3 ⚠️ 1 View Analysis > |

| CNMC Goldmine Holdings (Catalist:5TP) | SGD0.475 | SGD192.51M | ✅ 4 ⚠️ 1 View Analysis > |

| Goodbaby International Holdings (SEHK:1086) | HK$1.16 | HK$1.94B | ✅ 4 ⚠️ 1 View Analysis > |

| T.A.C. Consumer (SET:TACC) | THB4.64 | THB2.78B | ✅ 3 ⚠️ 3 View Analysis > |

| China Sunsine Chemical Holdings (SGX:QES) | SGD0.675 | SGD643.53M | ✅ 4 ⚠️ 1 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD2.49 | SGD9.8B | ✅ 5 ⚠️ 0 View Analysis > |

| Ekarat Engineering (SET:AKR) | THB0.96 | THB1.41B | ✅ 2 ⚠️ 2 View Analysis > |

| BRC Asia (SGX:BEC) | SGD3.60 | SGD987.66M | ✅ 3 ⚠️ 1 View Analysis > |

Click here to see the full list of 973 stocks from our Asian Penny Stocks screener.

We're going to check out a few of the best picks from our screener tool.

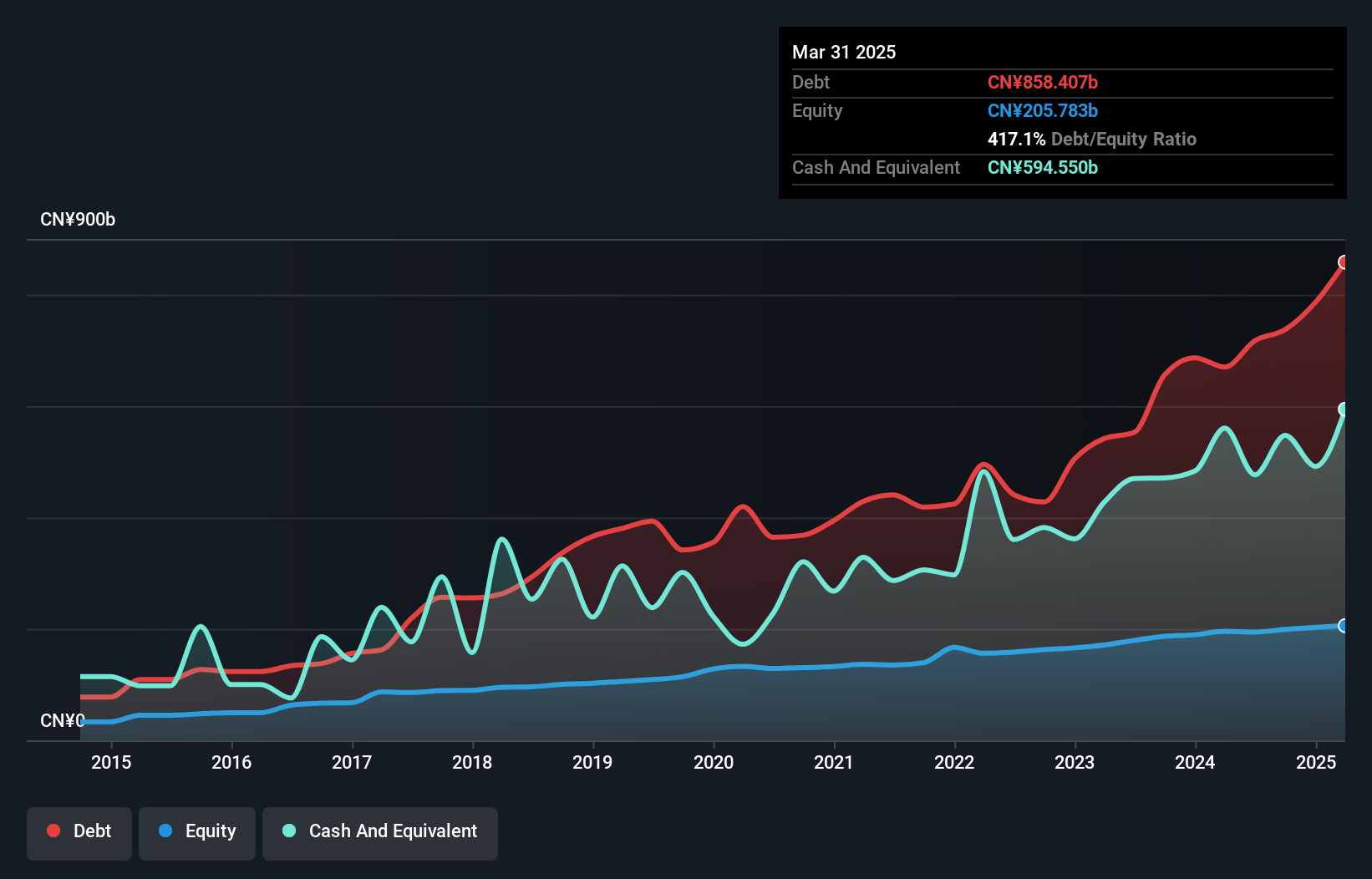

China Zheshang Bank (SEHK:2016)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: China Zheshang Bank Co., Ltd. offers a range of commercial banking products and services across Mainland China, with a market cap of HK$100.02 billion.

Operations: The company generates revenue of CN¥39.23 billion from its operations in Mainland China.

Market Cap: HK$100.02B

China Zheshang Bank, with a market cap of HK$100.02 billion and revenue of CN¥39.23 billion, offers potential value for penny stock investors due to its trading at a significant discount to estimated fair value. Despite recent executive changes, the bank maintains stable operations with an experienced board averaging 3.6 years in tenure. While earnings growth has been modest and return on equity is low at 7.7%, the bank's funding is primarily low-risk through customer deposits and it has high-quality past earnings. Recent dividend decreases and stable profit margins highlight ongoing financial adjustments amidst strategic shifts.

- Take a closer look at China Zheshang Bank's potential here in our financial health report.

- Evaluate China Zheshang Bank's prospects by accessing our earnings growth report.

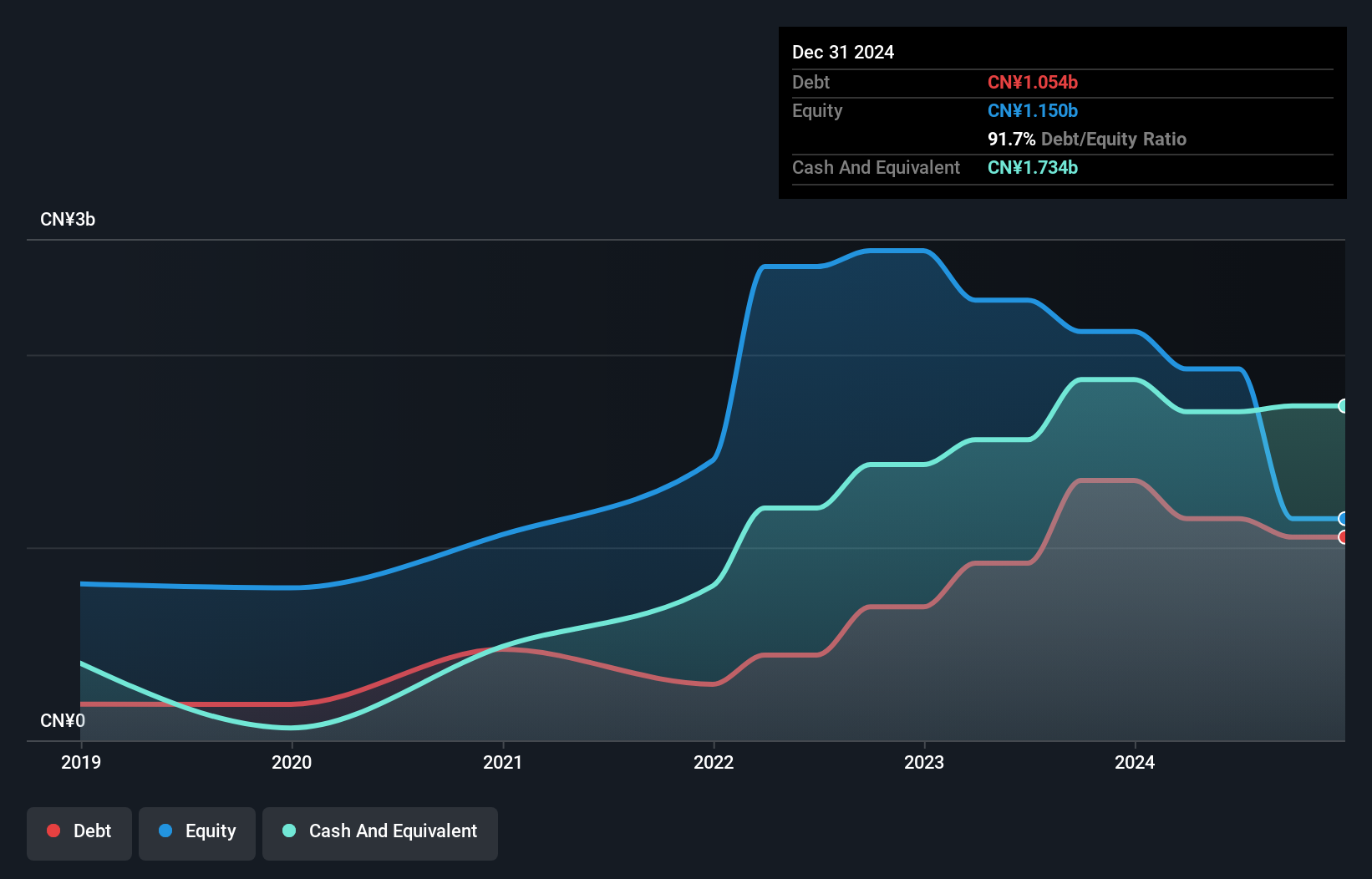

Yunkang Group (SEHK:2325)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Yunkang Group Limited is a medical operation service provider in the People's Republic of China with a market capitalization of approximately HK$2.57 billion.

Operations: The company generates revenue from its diagnostic services segment, which amounts to CN¥711.88 million.

Market Cap: HK$2.57B

Yunkang Group, with a market cap of approximately HK$2.57 billion, presents a mixed outlook for penny stock investors. The company is trading at 16.6% below its estimated fair value, suggesting potential undervaluation. However, it remains unprofitable with losses increasing by 54% annually over the past five years and a negative return on equity of -68.98%. Despite these challenges, Yunkang's financial position is robust; it has more cash than total debt and short-term assets (CN¥2.7 billion) that exceed both short-term (CN¥1.9 billion) and long-term liabilities (CN¥162 million). The management team is experienced with an average tenure of 2.7 years.

- Dive into the specifics of Yunkang Group here with our thorough balance sheet health report.

- Explore historical data to track Yunkang Group's performance over time in our past results report.

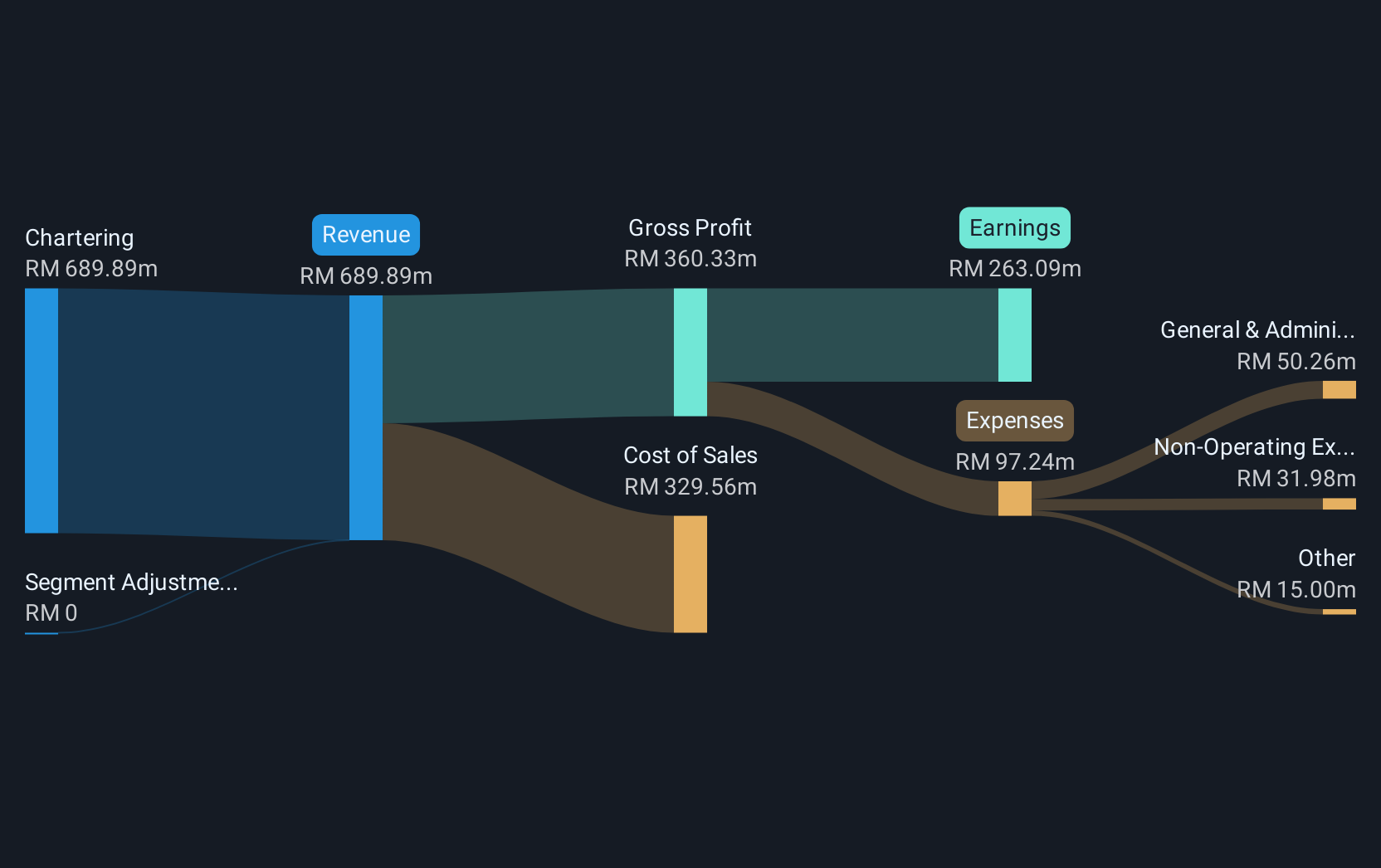

Nam Cheong (SGX:1MZ)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Nam Cheong Limited is an investment holding company engaged in shipbuilding and vessel chartering, with a market capitalization of SGD272.68 million.

Operations: The company generates revenue from its Chartering segment, amounting to MYR689.89 million.

Market Cap: SGD272.68M

Nam Cheong Limited, with a market cap of SGD272.68 million, shows both promise and challenges as an investment. The company is trading significantly below its estimated fair value while maintaining stable weekly volatility over the past year. Despite high net debt to equity ratio at 47.8%, short-term assets cover liabilities comfortably, and operating cash flow adequately covers debt obligations. Recent contracts valued at US$47.5 million for offshore support vessels in the Middle East and Japan diversify its revenue streams into renewable energy sectors, enhancing earnings visibility with 63% of its fleet under long-term charters amidst evolving global energy dynamics.

- Jump into the full analysis health report here for a deeper understanding of Nam Cheong.

- Examine Nam Cheong's past performance report to understand how it has performed in prior years.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 970 Asian Penny Stocks now.

- Curious About Other Options? Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nam Cheong might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10