Why Dave (DAVE) Is Up 9.5% After Barstool Partners With FOX Sports for Expanded Coverage And What's Next

- Earlier this week, Barstool Sports founder Dave Portnoy revealed a new partnership with FOX Sports to boost football and basketball coverage with expanded Barstool content and new shows.

- This collaboration marks a significant expansion for both companies, with FOX Sports fully integrating Barstool personalities and establishing a dedicated studio in Chicago.

- We'll look at how this expanded media partnership could influence Dave Inc.'s investment narrative and growth trajectory.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Dave Investment Narrative Recap

To be a shareholder in Dave, you need to believe the company can leverage the shift toward digital-first finance and maintain both strong user growth and improved monetization, especially via its proprietary cash advance model. The latest Barstool-Fox Sports partnership is not directly material to Dave Inc. in the immediate term, so the key short-term catalysts, like evolving product features or regulatory shifts impacting ExtraCash fees, and core risks, such as dependency on the current fee structure, remain unchanged for now.

Among recent company announcements, the promotion of Kyle Beilman to Chief Operating Officer stands out most. This appointment underscores a focus on tightening operational efficiency and financial discipline, which will be crucial as Dave faces competitive pressures and executes on catalysts like new member acquisition and cross-sell of financial products.

But against this backdrop, investors should not overlook the possibility that tighter regulation of platform fees could...

Read the full narrative on Dave (it's free!)

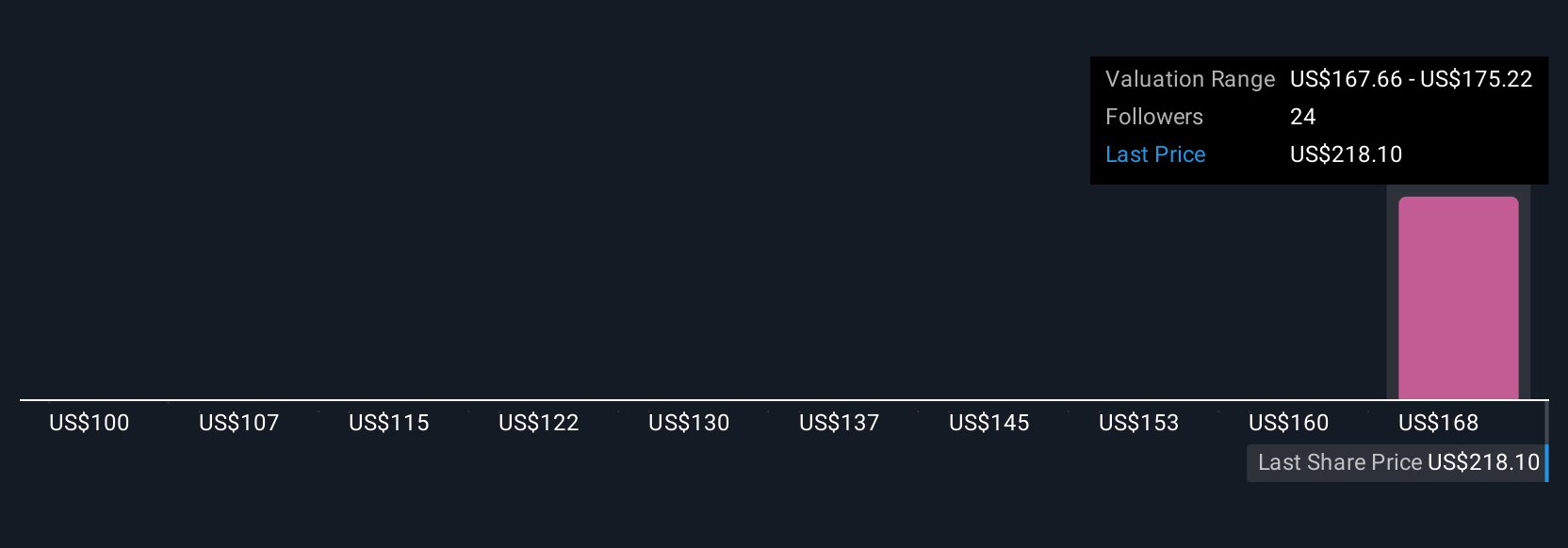

Dave's outlook anticipates $684.5 million in revenue and $204.3 million in earnings by 2028. This scenario assumes annual revenue growth of 21.5% and an earnings increase of $151.9 million from the current $52.4 million.

Uncover how Dave's forecasts yield a $237.25 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently estimate Dave's fair value between US$99.65 and US$320. With ongoing exposure to fee-related regulatory risk, it is clear that the company's future remains open to varied interpretations, now is a good time to explore several viewpoints.

Explore 3 other fair value estimates on Dave - why the stock might be worth less than half the current price!

Build Your Own Dave Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Dave research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dave research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dave's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10