Eli Lilly (LLY) Gains CHMP Approval for Donanemab in Alzheimer's Treatment

Eli Lilly (LLY) recently received a positive opinion from the Committee for Medicinal Products for Human Use (CHMP) for its Alzheimer's drug donanemab, underscoring the company's advancements in a crucial therapeutic area. During the same period, LLY registered a 5% share price increase, notably outpacing the broader market's 1% rise over the past week. This uptrend in LLY's stock could be attributed to investors' optimism about donanemab's potential impact. Additionally, the company's collaboration with Gate Bioscience to develop novel therapies further strengthens its innovative capabilities, adding weight to its share price momentum amid broader market gains.

We've spotted 2 risks for Eli Lilly you should be aware of, and 1 of them doesn't sit too well with us.

Find companies with promising cash flow potential yet trading below their fair value.

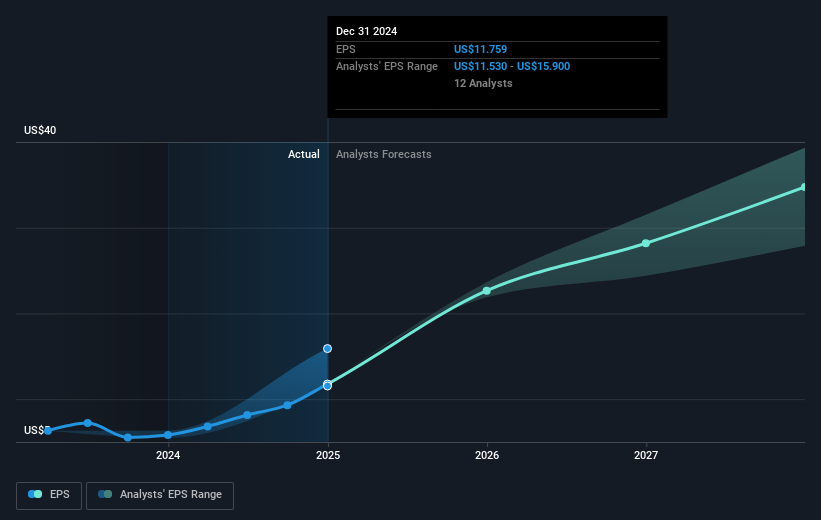

The recent positive opinion from the CHMP about Eli Lilly's Alzheimer's drug, donanemab, could significantly enhance the company's revenue and earnings forecasts. This development positions the company well for future growth, adding credibility to its strategic focus on expanding into high-demand therapeutic areas like oncology and immunology. Coupled with its collaboration with Gate Bioscience, these advances may provide substantial long-term benefits to the company's bottom line.

Over the past five years, Eli Lilly's total return, which includes both share price growth and dividends, was a very large 473.44%. This long-term growth far outpaces the recent 1% rise in the broader market over the past year, bolstering investor confidence in the company's strategic trajectory and robust pipeline.

In comparison to the US Pharmaceuticals industry, which saw a decline of 5.9% over the past year, Eli Lilly's sharp uptick in share price highlights its strong performance relative to industry peers. The company’s earnings growth was a robust 80.9% over the past year, indicative of its potent execution in a challenging market.

The current share price of US$812.69, when set against the analyst consensus price target of US$952.27, suggests there is room for potential growth. However, it also indicates investor caution, likely weighed down by concerns over competitive pressure and pricing dynamics. Investors might find reassurance in the company's ongoing manufacturing and R&D investments, which aim to mitigate risks and sustain growth in the coming years.

Understand Eli Lilly's track record by examining our performance history report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eli Lilly might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10