TradingKey - Markets have been buzzing this week around the new trade deal announced between the U.S. and the European Union. But while headlines touted a breakthrough, the details—and the politics—tell a more complicated story.

In fact, statements from the White House and the European Commission have differed on key points, raising uncertainty over what was actually agreed. The so-called deal may be more of a framework—or a negotiation-in-progress—than a finalized agreement.

What’s in the Deal?

On July 27, President Donald Trump and European Commission President Ursula von der Leyen jointly outlined the initial framework.

Under the deal, the U.S. will impose a 15% tariff on most goods imported from the EU, including critical exports like automobiles and automotive components. In return, Europe has pledged to invest €600 billion into the U.S. economy and to purchase up to €750 billion worth of American energy products—primarily liquefied natural gas (LNG), oil, and nuclear fuel—as part of a broader strategy to reduce its dependence on Russian suppliers.

Both sides have also agreed to eliminate tariffs on a list of jointly defined “strategic goods.” Categories mentioned include aircraft components, parts of industrial chemical manufacturing, semiconductor fabrication equipment, select agricultural goods, and certain critical raw materials. However, this list remains vague, and the EU has yet to release the full breakdown of items.

Meanwhile, the U.S. confirmed it will maintain its 50% tariff on European steel and clarified that pharmaceuticals are not currently covered under the agreement.

Still a Lot of TBD…

Despite the big announcements, a full joint statement defining the scope of the deal—and especially the zero-tariff categories—has not yet been finalized. This means a number of unresolved issues remain on the table.

For example, the EU is reportedly pushing to include products like wine, spirits, and certain industrial inputs such as chemical fertilizers into the list of tariff-free items.

“We will publish that list in the context of the finalisation of the joint statement so that this is clear where exactly we are going,” said one EU official familiar with the matter.

while there’s a framework in place, there’s still plenty of room for negotiation—and possible friction ahead.

Did Trump Come Out on Top?

On paper, the U.S. appears to have notched some real wins. These include new tariff restrictions on EU imports, especially industrial goods; major pledges from the EU on investments and energy purchases; and the removal of export tariffs on American cars heading to Europe.

However, take a closer look and things appear a bit more complicated.

First, the premise that tariffs strengthen domestic industry often ignores economic fundamentals: it’s usually domestic consumers—not foreign suppliers—who pay the price. That means higher prices for American consumers on imported goods, which isn’t ideal amid ongoing concerns over inflation and purchasing power.

And while some industries may see symbolic gains, those wins may be hard to convert into meaningful long-term competitive advantage.

Consider autos. On the surface, this feels like a win for Detroit: U.S. carmakers will benefit from zero tariffs when exporting to Europe, while European (mainly German) brands now face a 15% tariff when shipping vehicles to the U.S.

But in reality, German brands like BMW, Mercedes-Benz, and Audi have developed long-standing, loyal customer bases in the U.S.—especially in the premium market segment. Their value proposition is more about brand strength and product perception than price point. A 15% increase in import costs may push some consumers to delay purchases, but it’s unlikely to send them straight into the arms of Ford or GM.

Meanwhile, U.S. carmakers have a relatively small presence in the European market. Stronger trade terms won’t change much if the brands themselves haven’t earned European consumer trust or demand.

Many German brands are expected to respond by expanding local manufacturing in the U.S., which would allow them to bypass tariffs altogether. BMW, for example, already operates a major plant in South Carolina.

And don’t forget: Japan and South Korea are also subject to the same 15% U.S. tariff. But carmakers like Toyota, Hyundai, and Kia already have a large manufacturing footprint in the U.S., which cushions the impact. German automakers have lagged behind in that regard—meaning they take a bigger hit upfront. But that doesn't automatically translate into more U.S. market share for American brands. More plausibly, Asian brands will capture whatever slack German automakers lose.

In short, yes—German automakers face a tougher road ahead. But calling it a slam-dunk win for U.S. firms would be premature. If anyone gains through attrition, it might actually be Korean or Japanese automakers, not American ones.

Big Promises, Questionable Follow-Through

Now, what about those headline investment numbers—€750 billion in energy procurement and €600 billion in EU investment into the U.S.? Eye-catching, for sure. But how much of that money actually hits the ground?

That’s where things get tricky.

The EU, as a supranational political bloc, doesn't actually run centralized procurement for energy or capital investment. Those decisions are made by national governments—or more importantly, by the private sector. At best, Brussels can coordinate multi-lateral frameworks, offer credit guarantees, or promote certain projects. But it can’t force companies or countries to spend a specific amount.

As context: in 2023, EU energy imports from the U.S. came in at under €80 billion. Scaling that to €750 billion over a few years looks... highly ambitious.

It’s the same story for investment flows. Without compelling business cases and a favorable investment climate, private-sector capital is unlikely to materialize on the scale promised—regardless of what a joint press conference says.

Which brings us to the bigger point: while the deal gave markets a shot of optimism and helped push equities higher in the short term, the actual economic payoff depends heavily on how much is implemented—and how fast.

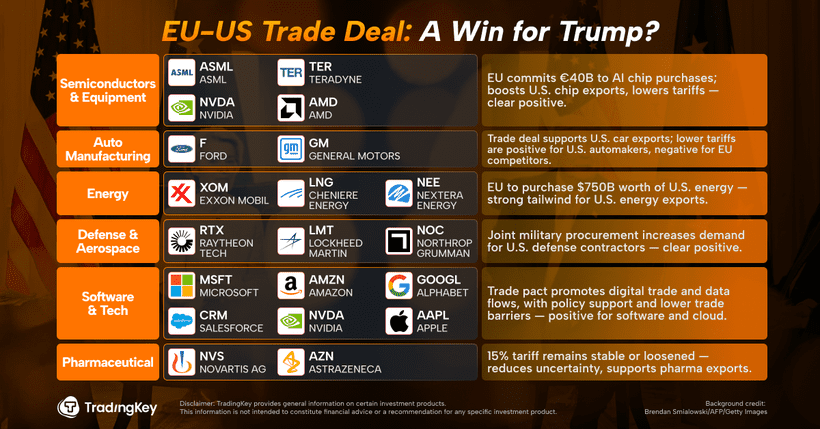

Here Are the Sectors Set to Benefit

Despite all the unknowns, some sectors in the U.S. equity market stand to gain from the current narrative and early-stage optimism:

- Semiconductors & Chip Equipment

Stocks: AMD, Teradyne, ASML, Nvidia

With the EU pledging €40 billion in AI chip procurement, U.S. chipmakers and fab equipment providers are gearing up for a wave of strong export flows—and potential tariff relief only adds to the upside.

- Autos

Stocks: General Motors (GM), Ford (F)

U.S. automakers benefit from zero tariffs into Europe, while their EU competitors now face higher costs shipping into the U.S.—at least on paper. Net gains may be muted, but sentiment still favors domestic names.

- Energy

Stocks: ExxonMobil (XOM), Cheniere Energy (LNG), NextEra Energy (NEE)

The EU’s massive energy procurement pledge—if even partially realized—gives a strong export tailwind to U.S. producers of LNG, oil and, potentially, nuclear fuel.

- Defense & Aerospace

Stocks: Lockheed Martin (LMT), Raytheon (RTX), Northrop Grumman (NOC)

With both sides pledging to boost defense spending and increase transatlantic defense coordination, American defense contractors have a clearer runway for long-term order volume.

- Software & Cloud

Stocks: Microsoft (MSFT), Amazon (AMZN), Nvidia (NVDA), Salesforce (CRM), Alphabet (GOOGL), Apple (AAPL), SAP

The deal is expected to reduce barriers to cross-border data and digital services, providing a boost to U.S. tech and SaaS vendors expanding into Europe.

- Pharma

Stocks: AstraZeneca (AZN), Novartis (NVS)

Find out more