Should You Forget Costco? Why These Unstoppable Stocks Are Better Buys

-

Costco is a retail powerhouse, using a membership model to create an annuity-like income stream.

-

Investors know exactly how well the business is performing right now.

-

If you care about valuation, you'll probably be better off with these out-of-favor dividend machines.

Costco (COST 1.51%) has increased its dividend annually for over two decades. That's an impressive dividend streak, but the story today is all about growth. While Costco is doing well on the growth front, investors are also well aware of that fact. That's why a couple of reliable dividend-paying consumer staples alternatives might be better options.

The problem with Costco

Costco operates club stores, which is somewhat unusual in the broader retail sector. Essentially, its customers pay a membership fee to shop at a Costco. That creates a reliable and recurring source of revenues that allows Costco to operate with tighter profit margins. It's a virtuous circle, since lower prices keep customers happily coming back (and paying their membership fees). The best example of the strength of the model is the roughly 90% member renewal rate.

Image source: Getty Images.

Right now, Costco is performing very well as a business, with new store openings. Customers are returning more often, and spending more every time they visit. The problem with Costco isn't the business -- it's the stock. Right now, the price-to-sales (P/S), price-to-earnings (P/E), and price-to-book value (P/B) ratios are all well above their five-year averages. The dividend yield is a miserly 0.6% or so. Investors are pricing a lot of good news into Costco's stock.

If you care about valuation, consider Coca-Cola and PepsiCo

Investors who are focused on income will clearly not be happy with Costco's tiny dividend yield. Investors who care at all about valuation will also be disappointed with the stock. There are better options on both fronts, with Dividend Kings Coca-Cola (KO 1.42%) and PepsiCo (PEP 1.02%) ranking high on the income and value fronts.

Coca-Cola will likely be the easier sell here. This beverage giant is performing quite well right now relative to PepsiCo. In the second quarter, Coca-Cola was able to grow organic revenues by a solid 5%, despite people's reluctance to spend their money thanks to inflationary concerns. Essentially, Coca-Cola sells an affordable luxury that people appear willing to buy no matter what.

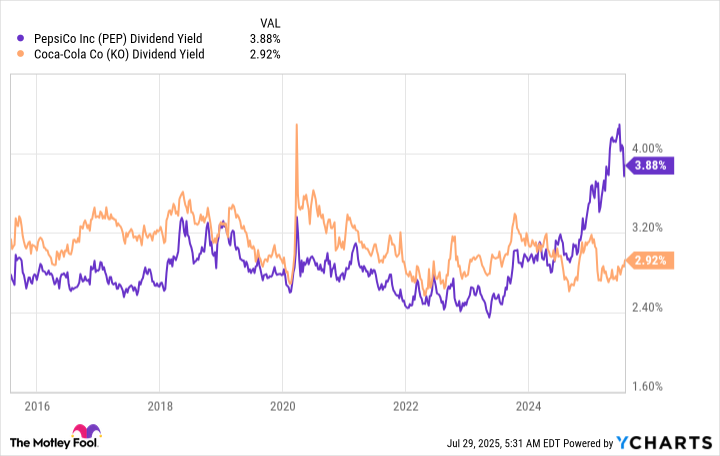

This strongly performing Dividend King, with over six decades of dividend increases behind it, isn't exactly cheap. But, unlike Costco, the stock appears reasonably priced. The P/S, P/E, and P/B ratios are all roughly at or slightly below their five-year averages. And while the stock's dividend yield is on the low side, historically speaking, it is still fairly attractive on an absolute basis at 3%. If you want to buy a good company that's performing well, Coca-Cola is a better value than Costco right now.

PEP Dividend Yield data by YCharts.

PepsiCo will appeal to investors with a deeper value bias, given that its P/S, P/E, and P/B ratios are soundly below their five-year averages. The dividend yield, at roughly 4%, is high on both a historical basis and on an absolute basis.

That said, PepsiCo isn't performing nearly as well as Coca-Cola at the moment. For example, PepsiCo's organic sales rose just 2.1% in the second quarter. That's less than half as much as Coca-Cola's organic sales growth in the same period. Clearly, investors recognize the underperformance and have priced PepsiCo's stock accordingly.

But if you are a dividend investor or a value investor, this is likely to be an opportunity. PepsiCo is a Dividend King with over five decades of annual dividend increases behind it. It has muddled through bad times before. Moreover, it's a more diversified business, operating in the beverage, salty snack, and packaged food niches of the food sector. So there are more levers to pull on the growth front as the company looks to get back on track.

Notably, it recently bought a probiotic beverage maker to augment its beverage business, and a Mexican-American food producer to supplement its food operations. In time, it's likely that PepsiCo will get back on track, and you'll get to collect a lofty yield while you wait.

Costco is too expensive -- Coca-Cola and PepsiCo are better choices

There's nothing wrong with Costco's business. The valuation of the stock is the problem. If you don't want to overpay for a company, you'll be better off with Coca-Cola or PepsiCo. Coca-Cola offers a strongly performing business and a reasonably priced stock. PepsiCo offers a relatively cheap stock backed by a historically well-run business going through tough times. Both Coca-Cola and PepsiCo have long provided unstoppable dividend growth.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10