Datadog (DDOG) In Talks To Acquire Israeli Cybersecurity Firm Upwind Security

Datadog (DDOG) is in advanced acquisition talks with Israeli cybersecurity firm Upwind Security, potentially enhancing its cloud security offerings. Meanwhile, a new integration with Reflectiz expands its enterprise security capabilities. Inclusion in major indices like the S&P 500 Equal Weighted and S&P Global 1200 marks a boost in Datadog's market visibility. These developments, focusing on strategic growth and expansion, provide important context to its share price growth of 28% in the last quarter, outpacing the broader market's mixed performance amidst fluctuations due to economic factors and earnings forecasts.

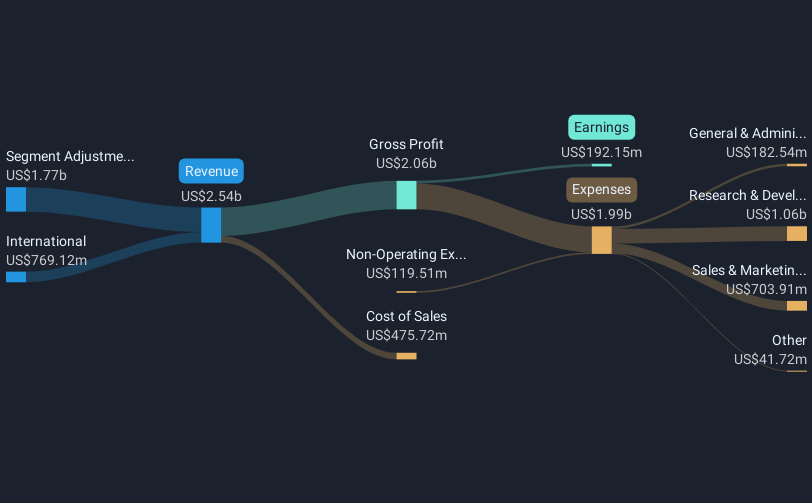

Be aware that Datadog is showing 1 possible red flag in our investment analysis.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

The potential acquisition of Upwind Security and integration with Reflectiz could enhance Datadog's cloud security and enterprise capabilities, potentially boosting its long-term revenue and earnings forecasts. These advancements align well with Datadog’s recent strategic moves in AI and security, which are central to its growth narrative. As Datadog continues to innovate and improve its product suite, these developments might support a stronger market position, which in turn could influence positive revenue trends moving forward.

Over the past five years, Datadog’s total shareholder return, including share price appreciation and dividends, was 77.57%. This performance reflects significant ongoing growth and contrasts with its recent 1-year period, where the company's return underperformed the US Software industry, which saw a 38.5% growth. Considering the recent price growth of 28% over the last quarter, the company looks appropriately active in the current market cycle, despite some challenges posed by the broader economic environment.

The current share price of US$135.60 is trading at a discount to the consensus analyst price target of US$149.99, suggesting room for potential growth if revenue and earnings forecasts align with expectations. Analysts project that earnings per share will grow significantly over the next three years, potentially validating these price targets. However, with a consensus valuation suggesting the company is fairly priced, investors should consider these price movements in the context of Datadog's broader strategic initiatives and market conditions.

Review our historical performance report to gain insights into Datadog's track record.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10