EcoGraf And 2 Other ASX Penny Stocks To Watch

The Australian market has shown a positive start to the week, with the ASX200 trading higher and Materials leading as the standout sector. In such an environment, investors often seek opportunities in smaller or newer companies that can offer growth at lower price points. While penny stocks may seem like a relic of past markets, they continue to present unique opportunities for those who focus on strong financial health and potential for long-term growth.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Rewards & Risks |

| Alfabs Australia (ASX:AAL) | A$0.39 | A$111.77M | ✅ 3 ⚠️ 3 View Analysis > |

| EZZ Life Science Holdings (ASX:EZZ) | A$2.12 | A$100.01M | ✅ 4 ⚠️ 3 View Analysis > |

| GTN (ASX:GTN) | A$0.40 | A$76.27M | ✅ 4 ⚠️ 2 View Analysis > |

| IVE Group (ASX:IGL) | A$2.96 | A$456.38M | ✅ 4 ⚠️ 2 View Analysis > |

| West African Resources (ASX:WAF) | A$2.71 | A$3.09B | ✅ 5 ⚠️ 1 View Analysis > |

| Southern Cross Electrical Engineering (ASX:SXE) | A$1.85 | A$489.16M | ✅ 4 ⚠️ 1 View Analysis > |

| Regal Partners (ASX:RPL) | A$3.01 | A$1.01B | ✅ 4 ⚠️ 2 View Analysis > |

| Austco Healthcare (ASX:AHC) | A$0.36 | A$131.58M | ✅ 4 ⚠️ 1 View Analysis > |

| CTI Logistics (ASX:CLX) | A$1.81 | A$145.79M | ✅ 4 ⚠️ 2 View Analysis > |

| Reckon (ASX:RKN) | A$0.655 | A$74.21M | ✅ 4 ⚠️ 2 View Analysis > |

Click here to see the full list of 456 stocks from our ASX Penny Stocks screener.

Let's review some notable picks from our screened stocks.

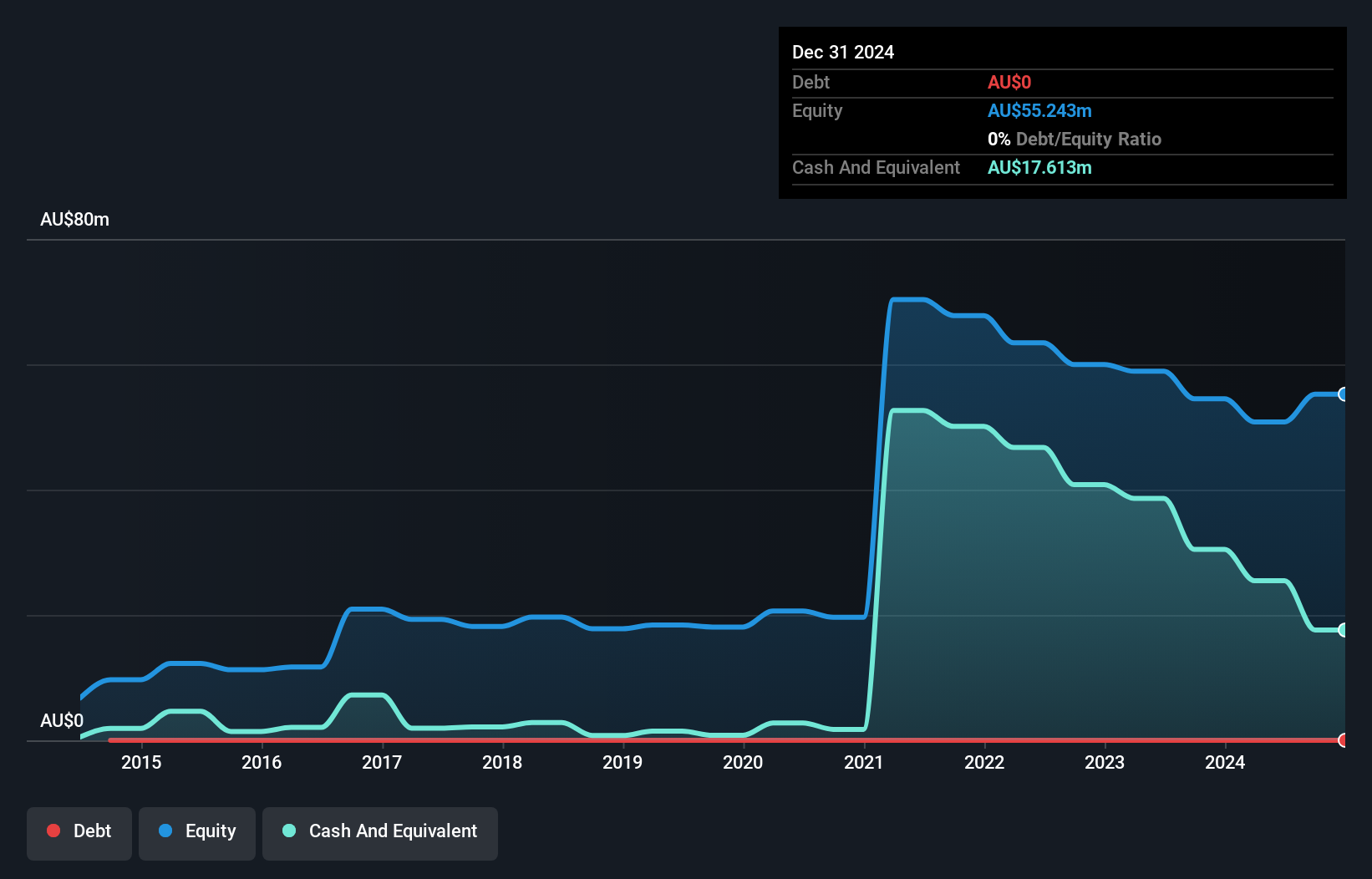

EcoGraf (ASX:EGR)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: EcoGraf Limited focuses on the exploration and production of graphite products for lithium-ion battery and advanced manufacturing markets in Tanzania and Australia, with a market cap of A$149.90 million.

Operations: The company's revenue segment is derived entirely from its operations in Australia, amounting to A$3.94 million.

Market Cap: A$149.9M

EcoGraf Limited, with a market cap of A$149.90 million, is in the pre-revenue stage, focusing on graphite products for battery and manufacturing markets. Despite being unprofitable, it holds no debt and has not diluted shareholders recently. The company boasts a seasoned board with an average tenure of 10 years and an experienced management team. EcoGraf's short-term assets significantly exceed its liabilities, providing financial stability. However, its cash runway is only sufficient for about 1.2 years if current cash flow trends persist. Earnings have declined over the past five years at a rate of 12.5% annually.

- Click to explore a detailed breakdown of our findings in EcoGraf's financial health report.

- Gain insights into EcoGraf's historical outcomes by reviewing our past performance report.

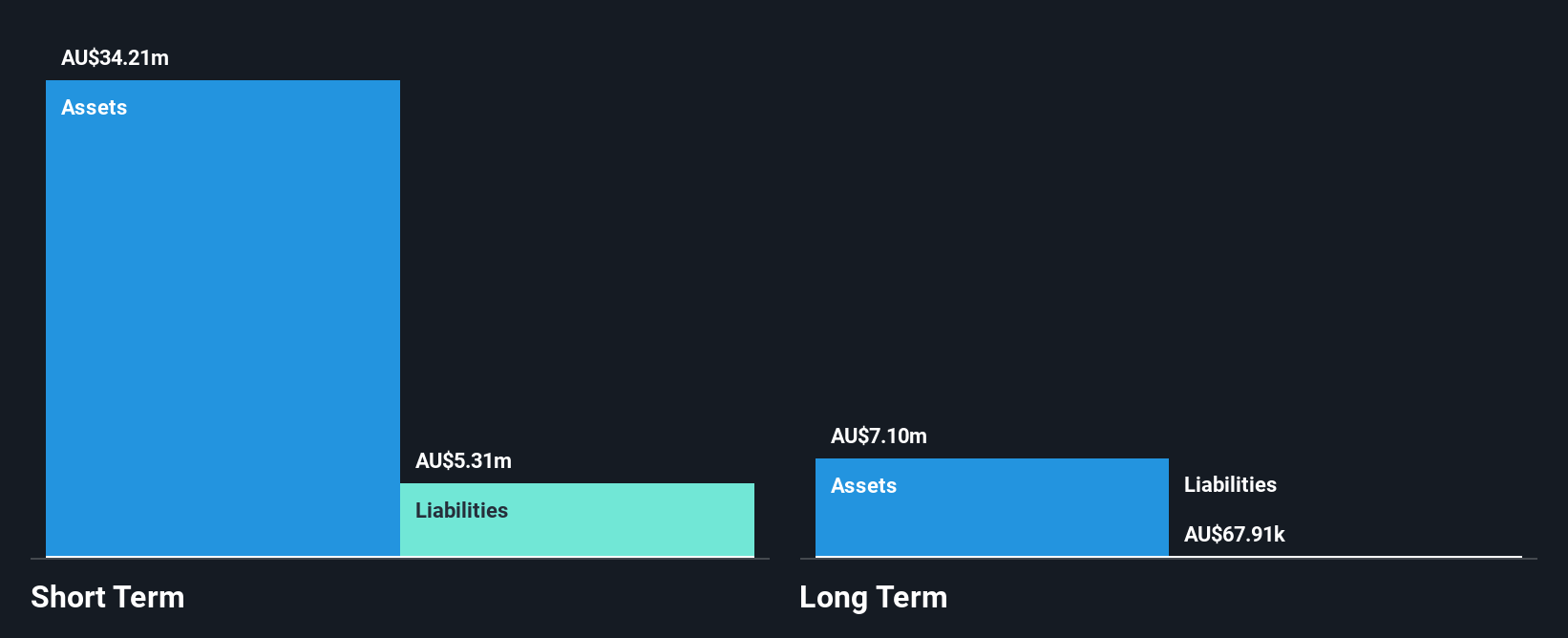

Sovereign Metals (ASX:SVM)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Sovereign Metals Limited, with a market cap of A$485.20 million, is involved in the exploration and development of mineral resource projects in Malawi through its subsidiaries.

Operations: Sovereign Metals Limited has not reported any revenue segments.

Market Cap: A$485.2M

Sovereign Metals Limited, with a market cap of A$485.20 million, is in the pre-revenue stage and focused on its Kasiya Rutile-Graphite Project in Malawi. The company recently completed significant geotechnical programs essential for advancing its Definitive Feasibility Study, indicating favorable subsurface conditions that could streamline construction efforts. Despite being unprofitable with a negative return on equity, Sovereign Metals remains debt-free and has not diluted shareholders recently. Its short-term assets significantly exceed liabilities, offering some financial stability despite an inexperienced management team and limited cash runway forecasted for one month based on free cash flow estimates.

- Click here and access our complete financial health analysis report to understand the dynamics of Sovereign Metals.

- Examine Sovereign Metals' earnings growth report to understand how analysts expect it to perform.

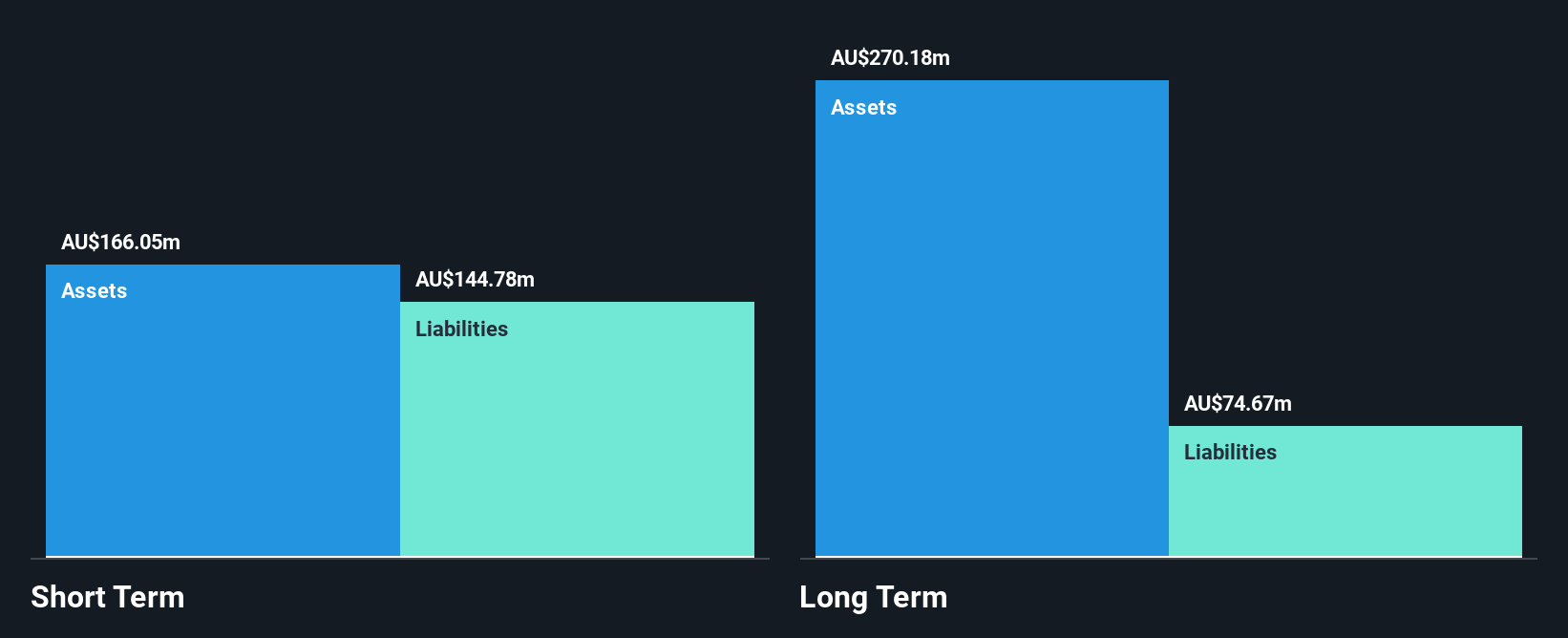

Tyro Payments (ASX:TYR)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Tyro Payments Limited provides payment solutions to merchants in Australia and has a market cap of A$508.84 million.

Operations: The company generates revenue primarily from its Payments segment, which accounts for A$464.66 million, and also earns A$14.88 million from Banking.

Market Cap: A$508.84M

Tyro Payments Limited, with a market cap of A$508.84 million, demonstrates financial stability by being debt-free and having short-term assets (A$166.0M) that exceed both short (A$144.8M) and long-term liabilities (A$74.7M). The company's revenue is primarily driven by its Payments segment, generating A$464.66 million annually. Despite recent insider selling, Tyro's earnings have grown significantly over the past year by 206.7%, surpassing industry averages and improving net profit margins from 2.2% to 6.1%. The recent board appointment of Steven Holmes may enhance strategic direction in fintech expansion efforts globally.

- Navigate through the intricacies of Tyro Payments with our comprehensive balance sheet health report here.

- Gain insights into Tyro Payments' future direction by reviewing our growth report.

Summing It All Up

- Access the full spectrum of 456 ASX Penny Stocks by clicking on this link.

- Curious About Other Options? These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10