Earnings Update: QuickLogic Corporation (NASDAQ:QUIK) Just Reported And Analysts Are Trimming Their Forecasts

It's been a pretty great week for QuickLogic Corporation (NASDAQ:QUIK) shareholders, with its shares surging 13% to US$6.53 in the week since its latest second-quarter results. Revenues were US$3.7m, with QuickLogic reporting some 7.8% below analyst expectations. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

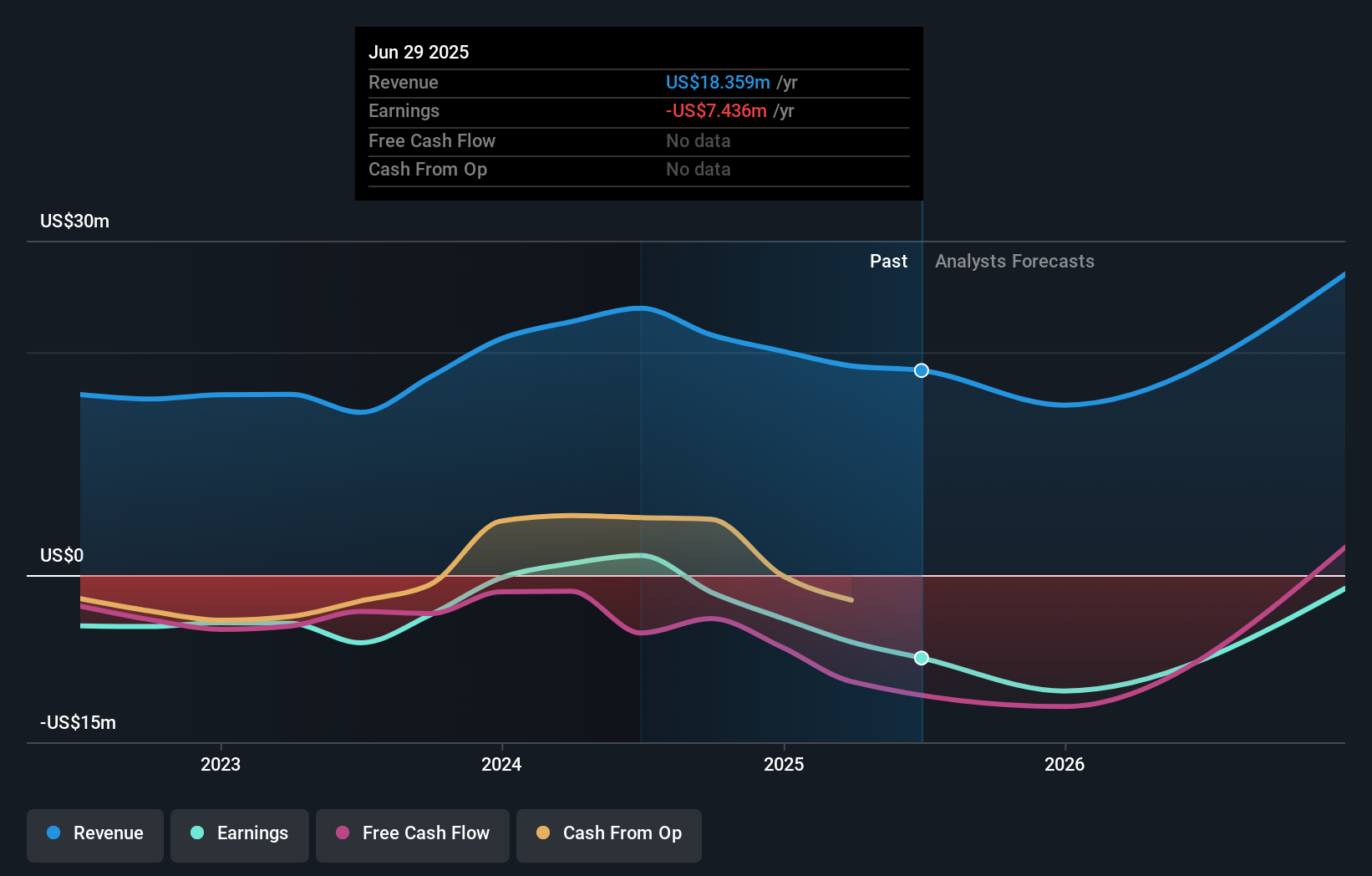

Taking into account the latest results, the current consensus, from the dual analysts covering QuickLogic, is for revenues of US$15.3m in 2025. This implies a chunky 17% reduction in QuickLogic's revenue over the past 12 months. Per-share losses are expected to explode, reaching US$0.61 per share. Before this latest report, the consensus had been expecting revenues of US$22.0m and US$0.095 per share in losses. There's been a definite change in sentiment in this update, with the analysts administering a notable cut to next year's revenue estimates, while at the same time increasing their loss per share forecasts.

View our latest analysis for QuickLogic

The consensus price target fell 12% to US$7.98, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that revenue is expected to reverse, with a forecast 31% annualised decline to the end of 2025. That is a notable change from historical growth of 18% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 17% annually for the foreseeable future. It's pretty clear that QuickLogic's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at QuickLogic. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of QuickLogic's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with QuickLogic .

Valuation is complex, but we're here to simplify it.

Discover if QuickLogic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10