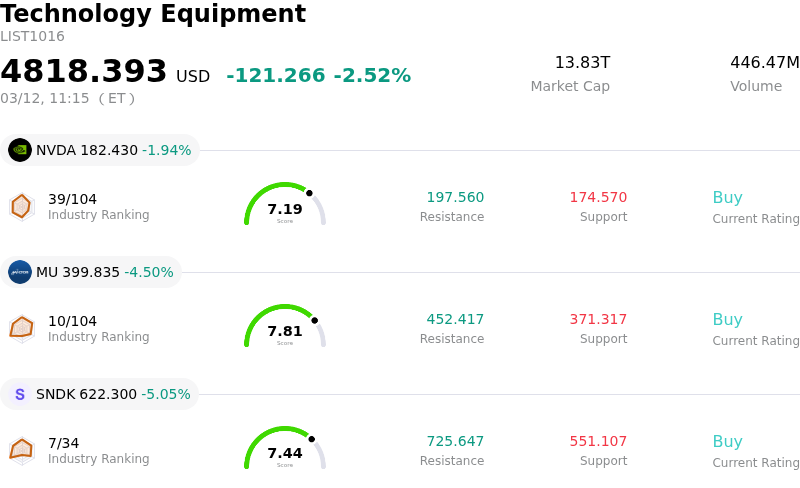

Lam Research Corp (LRCX) moved down by 4.43%. The Technology Equipment sector is down by 2.52%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 1.94%; Micron Technology Inc (MU) down 4.50%; SanDisk Corporation (SNDK) down 5.05%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

Lam Research's stock experienced a downward movement today, reflecting a combination of significant insider selling, institutional portfolio adjustments, and persistent company-specific risks that are weighing on market sentiment. While the broader outlook for the semiconductor equipment industry remains robust and the company has recently reported strong financial results, these negative factors appear to have dominated intraday trading.

A notable development contributing to the negative sentiment was the recent sale of a substantial number of shares by the company's Chief Financial Officer on March 4th. This insider selling, representing a measurable decrease in the executive's ownership, can be interpreted by investors as a signal of reduced confidence, leading to selling pressure. Additionally, a significant institutional investor, ProShares S&P Technology Dividend Aristocrats ETF, reduced its stake in Lam Research, further adding to the selling activity in the market. Such institutional rebalancing and divestment can exert considerable downward pressure on a stock, especially during periods of market sensitivity.

Furthermore, investors continue to monitor several company risks that, while not new, contribute to vulnerability. Concerns about potential margin compression due to an unfavorable product mix and escalating risks related to China revenue concentration, particularly in light of export controls, remain relevant. These long-standing risks, coupled with the stock's premium valuation, make it susceptible to profit-taking and sharper reactions to any perceived negative news or selling signals.

Despite these headwinds, the fundamental picture for Lam Research largely remains positive. The company recently exceeded revenue and earnings expectations for its fiscal second quarter and provided optimistic guidance for the upcoming quarter. The semiconductor equipment sector itself is projected for substantial growth, driven by increasing demand for AI-related technologies and advanced packaging. Moreover, analysts maintain a generally positive outlook on the stock, with many reiterating "Buy" ratings and upwardly revising price targets. The company's upcoming inclusion in the S&P 100 is also seen as a positive catalyst. However, today's price action suggests that immediate concerns over selling activity and valuation risks have temporarily overshadowed these more favorable long-term prospects.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [0.91], indicating a neutral signal. The RSI at 47.28 suggests neutral condition and the Williams %R at -60.40 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.39, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Significant insider selling pressure, including a director's reduction of their stake by over 12% and the CFO selling over $11.2 million in shares within the last 72 hours, potentially signaling cautious sentiment.

- Ongoing scrutiny from the US House Select Committee on the CCP regarding sales practices in China, coupled with a projected decline in revenue from China due to export controls and geopolitical tensions, represents a critical vulnerability given China's past revenue contribution.

- Negative outlook due to a decline in gross margin, attributed to a less favorable customer mix and reduced revenue from China.

- Analyst valuation models suggest the stock may be significantly overvalued, with some estimates pointing to a potential downside of over 34%, and recent downgrades citing a stretched price-to-earnings ratio.

Find out more