On April 16, Tom Lee, veteran equity strategist and co‑founder of Fundstrat, widely known as Wall Street’s “Market Prophet”, argued that U.S. and global equities are standing on firmer footing than when they hit previous record highs earlier this year. He firmly forecasts the S&P 500 could surge to 7,300 in the near term before any material downside correction.

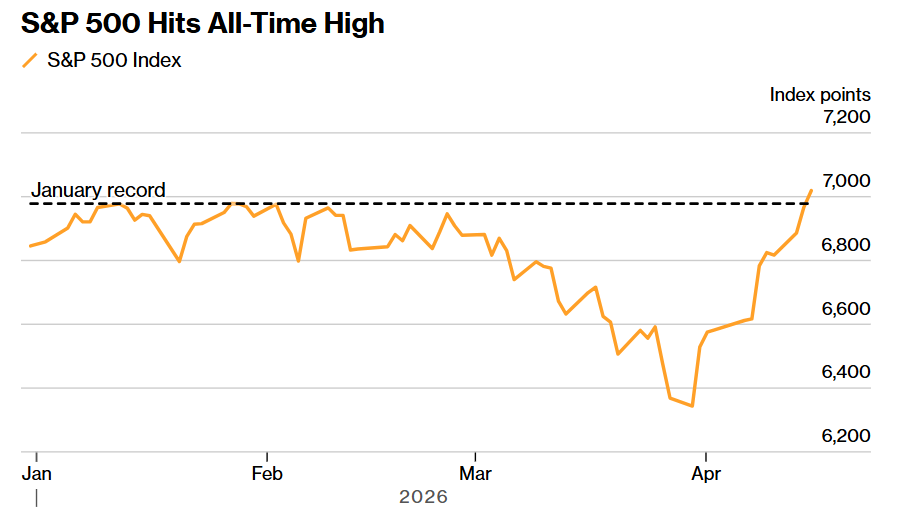

As of Wednesday’s close, the S&P 500 settled at 7,022.95, notching a fresh all‑time high. The Nasdaq Composite Index, tracking a broad range of tech stocks, rallied 1.6% to also close at a record peak, marking its latest 11‑day winning streak — the longest since December 2019.

Notably for retail investors, after an initial wave of sharp selloffs, Wall Street institutional capital has begun to brush off war‑related disturbances. Unlike early March, when geopolitical conflicts were viewed as a core market driver, Wall Street is now largely tuning out geopolitical noise.

The new bull market narrative rests on three solid pillars: robust corporate earnings resilience across the latest earnings season, improving risk appetite led by tech stocks and AI computing infrastructure, and market consensus that Middle East shocks will not trigger sustained long‑term inflation similar to the 2022 episode. As long as these three pillars hold, Wall Street will continue to treat war headlines as mere trading noise.

Tom Lee is one of Wall Street’s most accurate bullish strategists in recent years. He correctly called the 2023–2024 U.S. stock rally amid widespread pessimism in late 2022, earning him the moniker “Wall Street Prophet”. For the next market cycle, Lee remains confident that technology stocks will serve as the most powerful leader of the next super bull market.

Equities Are in Stronger Shape Than Early 2026

The chief investment officer and head of equity research shared his upbeat market outlook in recent interviews, citing multiple catalysts bolstering investor confidence. Lee outlined three key reasons for his bullish stance: exceptional earnings resilience amid spiking oil prices, upward revisions to global tech earnings forecasts, and easing inflation risks.

“Geopolitical conflict is, in fact, stimulating economic activity right now,” Lee commented. He added that Fundstrat’s historical analysis of surging WTI and Brent crude prices suggests the impact on core inflation — excluding energy and food — is far less severe than widely feared.

The veteran Wall Street strategist described the U.S. market as “the strongest house in an uncertain neighborhood”. He highlighted sustained operations across U.S. manufacturing facilities, at a time when many traditional industrial plants in Western nations face stagnation. Lee repeatedly stressed that global equity markets are fundamentally stronger today than during prior record peaks earlier this year.

Since 2020, investors have endured seven major black‑swan events. Even amid constrained shipping routes and disrupted oil supplies, the U.S. economy has proven resilient enough to absorb severe geopolitical shocks in the Middle East.

Middle East geopolitical developments also carry incremental positive signals. On April 15, Iran’s foreign ministry confirmed ongoing diplomatic dialogue with the U.S. mediated by Pakistan. The White House noted continuous, constructive bilateral engagement, with an optimistic outlook for potential agreements.

Wall Street Shuts Out War Risks, Tech Bullishness Escalates

While acknowledging lingering tail risks, Lee emphasized that the magnitude of potential downside has narrowed sharply. Aligning with mainstream Wall Street views, investors are increasingly ignoring Middle East tensions and turning bullish on artificial intelligence and computing infrastructure plays.

The dominant market narrative has shifted decisively from “whether Middle East conflicts will crush risk assets” to an optimistic growth story led by strong earnings and tech leadership.

High‑beta names with solid earnings visibility tied to AI infrastructure — led by industry leaders including NVIDIA, AMD, Broadcom and Taiwan Semiconductor — have become the most sensitive and outperforming segment during market rebounds.

This strength is underpinned by hard fundamental drivers: record‑breaking AI capital expenditures by global tech giants, rather than speculative hype. Major cloud hyperscalers such as Google, Microsoft and Amazon continue an aggressive capex arms race, prioritizing AI investment even amid debt expansion and workforce adjustments. This dynamic keeps leading AI supply‑chain stocks high‑conviction holdings.

Steve Sosnick, chief strategist at Interactive Brokers, wrote in a Wednesday report: “Market pricing suggests investors are trading as if the Persian Gulf conflict is de facto over.”

Top Wall Street traders and institutional investors, the key drivers behind the current equity recovery, are downplaying Middle East downside risks. Institutions view regional tensions as a manageable oil price disturbance rather than a systemic supply crisis.

They argue conflict fallout will remain temporary unless U.S. corporate earnings deteriorate, oil prices spiral into uncharted territory, or the Federal Reserve shifts to a full hawkish policy stance.

“Equity and broader financial markets appear remarkably complacent about the effective closure of the Strait of Hormuz,” said Doug Peta, chief U.S. investment strategist at BCA Research.

Mark Hackett, chief market strategist at Nationwide, credited institutional investors for driving the latest rally. After de‑risking via heavy selling, market focus has returned to solid corporate fundamentals delivered during the current earnings season.

Tom Lee acknowledged legitimate concerns over commodity supply disruptions, including helium shortages, but noted that a lasting ceasefire would boost growth sentiment and limit economic fallout for the U.S.

He echoed JPMorgan’s core view that tech stocks anchored in AI infrastructure must lead the next phase of the super bull market.

Since the outbreak of the Iran conflict, Bitcoin — widely regarded as a risk‑asset barometer — and Ethereum have been the best‑performing assets, closely correlated with tech sentiment.

Gains have also extended to energy stocks benefiting from geopolitical premiums, the Magnificent Seven tech giants including NVIDIA and Google, and software names that suffered historic declines in February.

“When growth concerns rise, technology remains the primary growth driver,” Lee explained. He added that tech stocks were heavily underweighted following broad investor deleveraging.

Sharp valuation contractions in the first quarter have made high‑quality tech names increasingly attractive relative to their robust long‑term earnings growth potential.

Leading AI infrastructure firms possess durable economic moats, with earnings growth consistently outpacing the S&P 500 aggregate, positioning them as top beneficiaries of the global AI adoption boom.

“Five years from now, investors will likely be shocked at how attractive these high‑fundamentals tech stocks were at current valuations,” Lee predicted.