SpaceX's latest financial data reveals that its Starlink business generated $11.4 billion in revenue last year with an EBITDA margin of 63%, making it the company's only profitable segment. However, the combined rocket and AI businesses consumed approximately $17 billion in cash, resulting in a net loss for the company of nearly $5 billion. Analysts suggest this IPO is essentially Elon Musk financing his space and AI ambitions, with the massive valuation hiding significant cash burn risks, posing a severe test for market acceptance.

SpaceX is approaching a potentially record-breaking IPO, with its newly revealed financial data exposing a sharply divided fundamental picture: the Starlink satellite internet business has become the company's sole profit engine, while the rocket launch and artificial intelligence (AI) businesses are mired in heavy cash consumption.

On April 13, according to a report by tech media The Information, undisclosed financial data shows that SpaceX's total capital expenditure last year reached a massive $20.7 billion, exceeding its total annual revenue, with a net loss close to $5 billion. The approximately $3 billion in free cash flow generated by the Starlink business was far from sufficient to cover the combined cash burn gap of roughly $17 billion from the rocket and AI businesses.

Market analysis indicates that this unconventional IPO is essentially Elon Musk raising funds for his space exploration and AI ambitions. Investors need to maintain a clear-eyed view of the potential financial risks before participating. Whether SpaceX's current $2 trillion valuation gains market acceptance will largely depend on investors' willingness to pay a premium for Starlink's rapid growth and the company's long-term vision, which includes space-based data centers and AI competition.

Starlink: The Sole Profit Engine with Strong Growth Momentum

SpaceX's financial fundamentals show significant internal divergence.

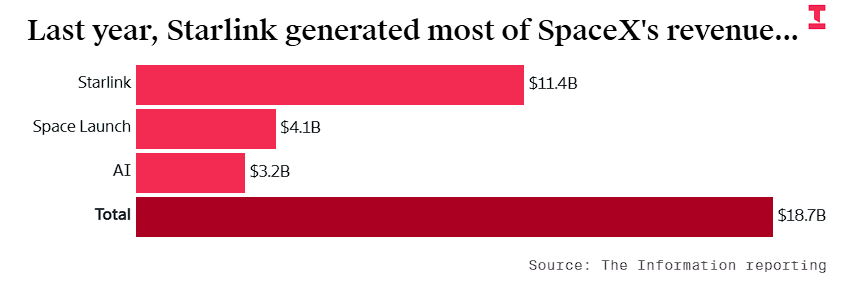

According to the financial data disclosed by The Information, the Starlink business generated $11.4 billion in revenue last year, a 50% increase year-over-year, accounting for 61% of the company's total sales. This business is SpaceX's only cash-generating segment, with adjusted EBITDA reaching $7.2 billion and its margin jumping from 41% in 2023 to 63%.

Chris Quilty, a satellite and space analyst at Quilty Space, stated that Starlink is providing data capacity previously unattainable, attracting a broad customer base including urban users.

However, the cash generated by Starlink is far from sufficient to support SpaceX's other businesses. Data shows that SpaceX's capital expenditure last year was as high as $20.7 billion, with overall cash burn amounting to approximately $14 billion.

Within this, the rocket launch business revenue grew only 8% to $4.1 billion, generating approximately negative $3 billion in free cash flow; meanwhile, the AI business, which includes social media platform X and model developer xAI, generated only $3.2 billion in revenue but consumed nearly $14 billion in cash.

The report points out that despite Starlink's strong performance, SpaceX as a whole remains a "money pit," with high AI development costs being the largest source of losses.

Doubts Over the Logic Behind the $2 Trillion IPO Valuation

The report states that SpaceX's listing will severely test the public market's ability to price an extreme growth story, as SpaceX's current valuation logic requires investors to possess extremely high optimism. The company's most recent valuation was $1.25 trillion, equivalent to 266 times last year's EBITDA.

This multiple is significantly higher than the valuation multiples of 16 to 36 times for tech giants like Meta (META), Alphabet, and Nvidia (NVDA), and even exceeds the 119x multiple of Elon Musk's other company, Tesla (TSLA).

Furthermore, according to The Information, some bankers are even hoping to assign SpaceX a $2 trillion valuation, which falls outside the scope of traditional financial analysis.

To support this valuation, SpaceX is trying to paint a picture for investors of synergistic development across its three business areas, such as leveraging its advantage in rocket launches to deploy data centers in space to advance its AI business. However, it's undeniable that AI development costs are extremely high, and investments in rockets and data centers are continuously compressing the company's profit margins.

The Information analysis notes that this is not a conventional stock offering, but rather Elon Musk asking the public to fund his grand goals of competing in AI, building orbital data centers, and space travel. While these goals are ambitious, they are not necessarily the foundation for building a profitable company.

For potential investors, the key is to remain clear-headed and explicitly recognize that investing in SpaceX means taking on real risk of capital loss. The final investment decision will depend entirely on their risk appetite for this future vision.