Investor Optimism Abounds Diamond Offshore Drilling, Inc. (NYSE:DO) But Growth Is Lacking

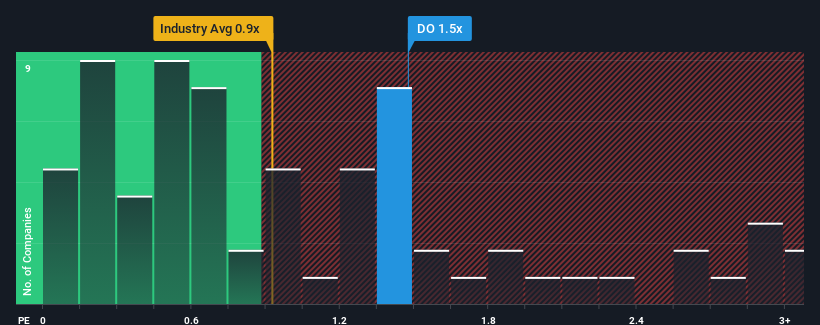

Diamond Offshore Drilling, Inc.'s (NYSE:DO) price-to-sales (or "P/S") ratio of 1.5x may not look like an appealing investment opportunity when you consider close to half the companies in the Energy Services industry in the United States have P/S ratios below 0.9x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for Diamond Offshore Drilling

How Diamond Offshore Drilling Has Been Performing

Recent times have been advantageous for Diamond Offshore Drilling as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Diamond Offshore Drilling.How Is Diamond Offshore Drilling's Revenue Growth Trending?

Diamond Offshore Drilling's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. As a result, it also grew revenue by 15% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 7.0% per annum over the next three years. That's shaping up to be materially lower than the 9.7% each year growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that Diamond Offshore Drilling's P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Diamond Offshore Drilling's P/S?

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've concluded that Diamond Offshore Drilling currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

It is also worth noting that we have found 1 warning sign for Diamond Offshore Drilling that you need to take into consideration.

If you're unsure about the strength of Diamond Offshore Drilling's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

What are the risks and opportunities for Diamond Offshore Drilling?

NYSE:DO

Diamond Offshore Drilling

Diamond Offshore Drilling, Inc. provides contract drilling services to the energy industry worldwide.

Rewards

Trading at 30.6% below our estimate of its fair value

Earnings are forecast to grow 47.58% per year

Became profitable this year

Risks

Debt is not well covered by operating cash flow

Share Price

Market Cap

1Y Return

Further research onDiamond Offshore Drilling

ValuationFinancial HealthInsider TradingManagement TeamHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10