BUCK: Harvesting Interest Rate Volatility Premium To Boost Treasury Returns

Jitalia17

Recently, I wrote a bullish article on the JPMorgan Ultra-Short Income ETF (JPST). With the Federal Reserve set to begin cutting policy interest rates at the upcoming September FOMC meeting, the JPST should outperform cash from the tailwind of its modest duration exposure.

This article looks at another 'cash replacement' tool, the Simplify Treasury Option Income ETF (NYSEARCA:BUCK).

Unlike the JPST, which uses modest credit exposure to try to outperform cash, the BUCK ETF writes options on interest rate indices and bond futures to harvest interest rate volatility premiums.

While the total returns are similar between JPST and BUCK, I believe BUCK's strategy may be fundamentally riskier, as it is short convexity and may expose investors to acute underperformance, like what happened in April 2024.

Overall, as a cash replacement tool, I prefer the credit exposures of the JPST ETF, as it is easier to monitor. I rate the BUCK ETF a hold.

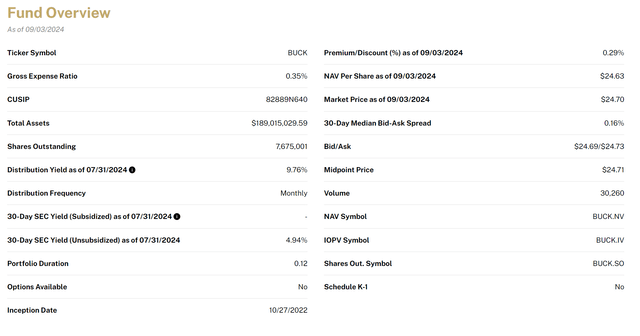

Fund Overview

The Simplify Treasury Option Income ETF (formerly called the Simplify Stable Income ETF) seeks to generate monthly income by investing at least 80% of the fund's portfolio in U.S. Treasury securities with a duration of less than 1 year. The fund also aims to generate additional income by writing options on fixed-income indices, futures, and ETFs.

The BUCK ETF, launched in October 2022, has $189 million in assets and charges a 0.35% gross expense ratio (Figure 1).

Figure 1 - BUCK overview (simplify.us)

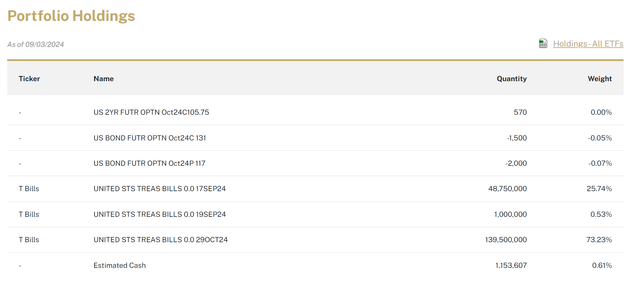

Portfolio Holdings

As per its mandate, the BUCK ETF holds the majority of its assets in short-duration U.S. Treasury securities. As of September 3, 2024, BUCK holds 99.5% of its portfolio in treasury bills maturing in September and October. The fund has also written options on bond futures (Figure 2).

Figure 2 - BUCK portfolio holdings (simplify.us)

Although BUCK currently only holds treasury bills, the fund's long treasury position is actively managed and can invest in securities such as treasury bills, notes, bonds, and Treasury Inflation-Protected Securities ("TIPS"), depending on which securities provide the highest total returns at any given time.

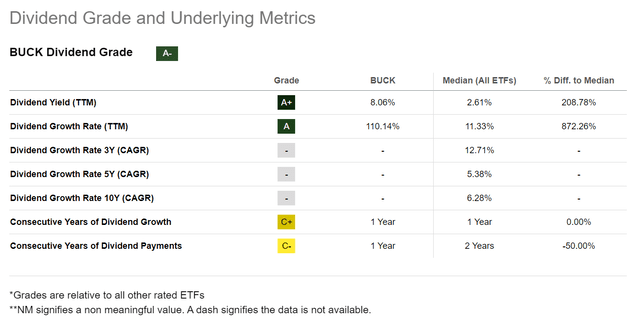

BUCK Pays An Attractive Distribution Yield...

For a short-duration fund, the BUCK ETF does pay an attractive distribution yield. In the past year, the BUCK ETF has yielded 8.1% from the combination of earning income from its treasury securities plus the income from writing options (Figure 3).

Figure 3 - BUCK has paid 8.1% LTM yield (Seeking Alpha)

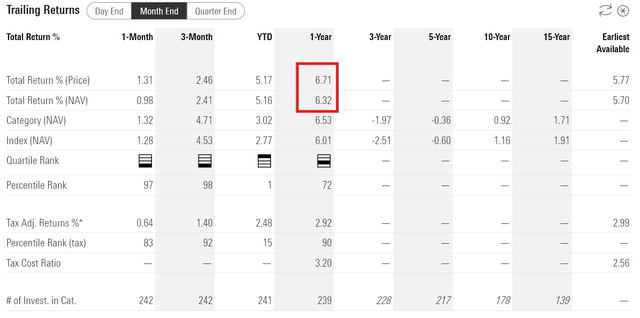

...But Modest Total Returns

However, BUCK's modest total returns, with a 1-year total return of 6.3% to August 31, 2024, suggest there is less meets the eye (Figure 4).

Figure 4 - BUCK's historical total returns (morningstar.com)

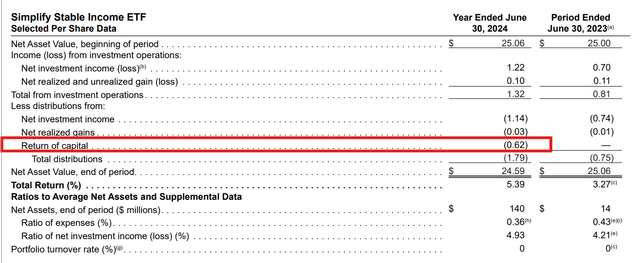

Looking through the fund's annual financial statements, we see that $0.62 out of the fund's $1.79 in distributions paid in the year to June 30, 2024 was deemed 'return of capital' ("ROC"), which means investors were simply paid back their own capital through the distribution (Figure 5).

Figure 5 - BUCK uses ROC to boost yield (BUCK annual report)

How Does The BUCK Compare Against Peers?

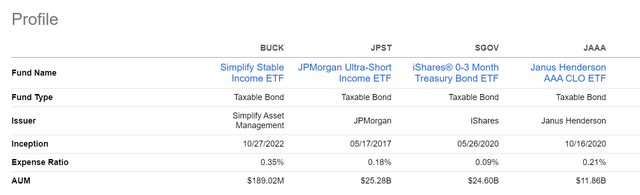

Taking a step back, let's take a look at how the BUCK ETF stacks up against short-term money-market and cash-replacement funds like the JPST ETF, the iShares 0-3 Month Treasury Bond ETF (SGOV), and the Janus Henderson AAA CLO ETF (JAAA).

In terms of fund structure, BUCK is the smallest fund with just $189 million in AUM compared to $25 billion for JPST and SGOV and $12 billion for the JAAA. It also charges the highest expense ratio at 0.35% compared to 0.18% for JPST, 0.09% for SGOV, and 0.21% for JAAA (Figure 6).

Figure 6 - BUCK vs. peers, fund structure (Seeking Alpha)

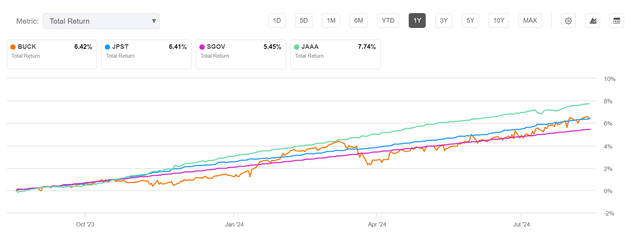

Next, if we compare total returns, we can see that BUCK's 1-year total return is comparable to that of the JPST ETF at 6.4% and has outperformed the SGOV's 5.5%, but has lagged the JAAA ETF's 7.7% (Figure 7).

Figure 7 - BUCK vs. peers, 1-year total return (Seeking Alpha)

Another notable feature of Figure 7 is the relative volatilities of the strategies. While JPST, SGOV, and JAAA all appear to have minimal volatilities, BUCK's total returns appear to exhibit significant volatility, with a notable decline in early April.

Reading BUCK's Q2 commentary, the BUCK ETF underperformed in Q2/2024 due to its "option-writing strategies as interest rates were very volatile and threatened to break out of their range."

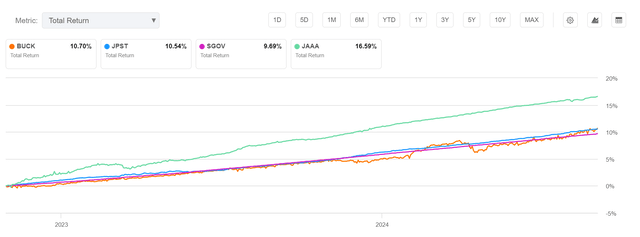

Stretching the historical returns to BUCK's inception in October 2022 shows a similar total returns picture, with the BUCK roughly matching JPST, outperforming SGOV, and underperforming the JAAA (Figure 8).

Figure 8 - BUCK vs. peers, since inception returns (Seeking Alpha)

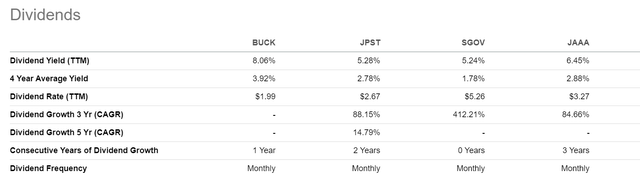

Finally, comparing the funds' distribution yields, we see that the BUCK ETF has paid the highest distribution yield (Figure 9). However, this should be tempered by BUCK's use of ROC to boost its distribution.

Figure 9 - BUCK vs. peers, distribution yield (Seeking Alpha)

Overall, comparing the BUCK ETF against other 'cash alternative' funds like the JPST and JAAA, I believe the BUCK ETF may be a relatively riskier product, as it is attempting to harvest interest rate volatility premiums to boost its total returns. As shown in Figure 7, when interest rate volatility rises, the BUCK ETF may underperform, as it is short convexity.

In contrast, the JPST and JAAA use modest credit exposures to outperform cash and may be 'relatively safer' bets, as credit markets are well understood.

Key Risk To BUCK

The key risks to the BUCK ETF and other 'cash replacement' funds like JPST and JAAA are market crashes. For example, the JPST ETF had a mini-crash during the COVID-19 pandemic as credit markets went 'no-bid', causing MTM losses for the JPST ETF (Figure 10).

Figure 10 - JPST can suffer steep MTM losses when credit markets become dislocated (am.jpmorgan.com)

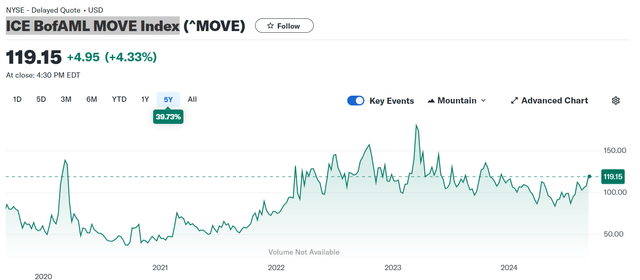

A similar situation could re-occur in the future during market stress events, particularly with BUCK's short volatility exposure. For BUCK investors, one key metric to monitor is the BofA MOVE Index, which measures market interest rate volatility, similar to how the VIX Index measures equity volatility (Figure 11).

Figure 11 - BUCK investors should monitor the MOVE (Yahoo Finance)

When interest rate volatilities spike higher, like in April 2024, short-vol funds like BUCK may be at risk of a drawdown.

Being a discretionary fund, investors are also at the whim of the fund managers' acumen. While the team at Simplify is long-tenured and experienced, they have also occasionally slipped up.

Conclusion

The BUCK ETF is an innovative 'cash replacement' fund that harvests interest rate volatility premiums to enhance the returns from holding short-duration treasuries.

So far, the BUCK ETF has performed in line with similar cash replacement tools like the JPST ETF. However, the BUCK ETF has exhibited greater volatility, as its option-writing strategy may be fundamentally riskier than JPST's modest credit exposures.

In my opinion, I prefer the JPST and JAAA, as they have similar or better returns than BUCK while exhibiting lower volatility. I rate the BUCK a hold.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10