Kennedy-Wilson Holdings (NYSE:KW) Has A Somewhat Strained Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Kennedy-Wilson Holdings, Inc. (NYSE:KW) does use debt in its business. But should shareholders be worried about its use of debt?

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

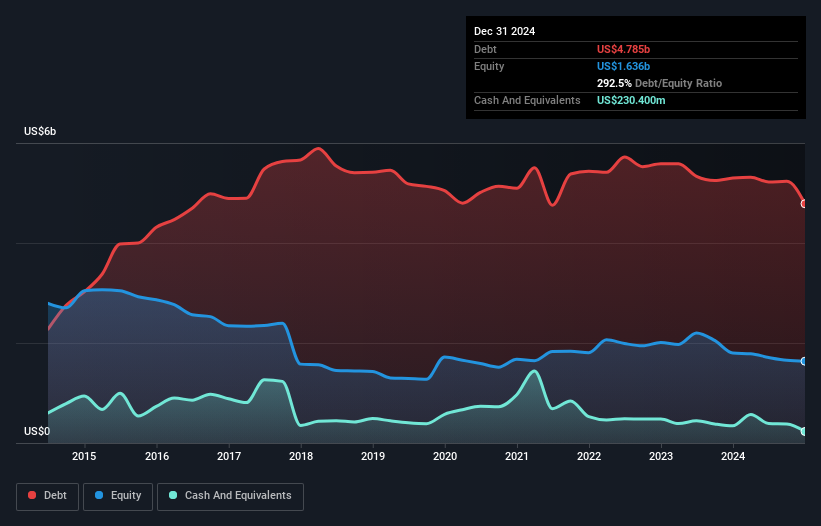

What Is Kennedy-Wilson Holdings's Net Debt?

As you can see below, Kennedy-Wilson Holdings had US$4.78b of debt at December 2024, down from US$5.30b a year prior. However, it also had US$230.4m in cash, and so its net debt is US$4.55b.

How Strong Is Kennedy-Wilson Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kennedy-Wilson Holdings had liabilities of US$673.9m due within 12 months and liabilities of US$4.65b due beyond that. On the other hand, it had cash of US$230.4m and US$310.3m worth of receivables due within a year. So its liabilities total US$4.78b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$924.7m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Kennedy-Wilson Holdings would likely require a major re-capitalisation if it had to pay its creditors today.

Check out our latest analysis for Kennedy-Wilson Holdings

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 0.19 times and a disturbingly high net debt to EBITDA ratio of 23.3 hit our confidence in Kennedy-Wilson Holdings like a one-two punch to the gut. The debt burden here is substantial. Looking on the bright side, Kennedy-Wilson Holdings boosted its EBIT by a silky 58% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Kennedy-Wilson Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Kennedy-Wilson Holdings generated free cash flow amounting to a very robust 90% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

To be frank both Kennedy-Wilson Holdings's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Kennedy-Wilson Holdings stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 3 warning signs we've spotted with Kennedy-Wilson Holdings .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you're looking to trade Kennedy-Wilson Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kennedy-Wilson Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10