Prediction: This Super Software Growth Stock Will Be Worth More Than Palantir by 2030

-

Artificial intelligence (AI) has redefined Palantir's business.

-

Over the last two years, the company's valuation has risen more than 17-fold.

-

While AI will continue to be a massive opportunity for Palantir, another player in the software realm may have more upside over the next five years.

The allure of artificial intelligence (AI) has dominated the stock market for over two years. AI is not just an interest among investors -- it's become a bit of an obsession. And one stock that investors just can't seem to get enough of is data analytics specialist Palantir Technologies (PLTR 6.77%).

As of this writing (April 30), Palantir stock sports a share price of roughly $117 -- just a stone's throw away from its 52-week high. That's quite a feat considering the S&P 500 and Nasdaq Composite have struggled mightily throughout the course of 2025, thanks to a lagging technology sector.

In the piece below, I'll detail Palantir's epic rise and soaring valuation throughout the AI revolution. More importantly, let's explore why another emerging software business could be the better buy as it has the potential to eclipse Palantir's size over the next several years.

Palantir's rise has been epic, but...

Palantir was founded over 20 years ago. For most of its history, the company concentrated on the public sector -- working closely with the U.S. military and its allies in the defense world. Given the lumpy nature of government contracting, Wall Street was skeptical of Palantir's growth potential when the company went public in 2020. Some skeptics viewed Palantir as a consulting agent for the government and not so much a high-flying software business.

This narrative started changing exactly two years ago. In April 2023, Palantir released its fourth major enterprise tool, called the Artificial Intelligence Platform (AIP). In the table below, I've summarized some key performance indicators around Palantir's business prior to and following the release of AIP.

| Category | Q1 2022 (Prior to AIP) | Q4 2024 (Latest Published Financials) |

|---|---|---|

| Government customers | 93 | 140 |

| Commercial customers | 184 | 571 |

| Total revenue | $446 million | $827 million |

| Net income | ($101 million) | $79 million |

| Adjusted free cash flow | $29.8 million | $517.4 million |

Data source: Palantir.

The growth speaks for itself. AIP has been a transformative piece of infrastructure for Palantir, allowing the company to swiftly penetrate the private sector, accelerate revenue, and widen profit margins. While Palantir deserves a lot of credit, investors may be getting a little too excited. In just two years, the company's market capitalization has ballooned by more than 17 times. To add another layer of perspective here, Palantir currently trades for 100 times its trailing-12-month sales.

PLTR Market Cap data by YCharts.

PLTR Market Cap data by YCharts.

Right now, smart investors are wondering when Palantir will hit its ceiling. While AI should remain a long-run tailwind for the company, there will come a time when its valuation multiples begin to normalize. Over the next five years, expectations are likely to be higher and higher with each passing earnings report. My hunch is that the triple-digit returns from Palantir stock may be in the rearview mirror for the time being. By 2030, I would not be surprised if Palantir's valuation is largely unchanged compared to where it is today.

Image source: Getty Images.

...this other software player could be more dominant in the long run

The software company that I think has more potential than Palantir over the next five years is cybersecurity firm CrowdStrike (CRWD 2.00%). In the world of investing, CrowdStrike has become somewhat polarizing over the last year due to a high-profile security outage featuring the company's software.

The biggest tailwind I see for CrowdStrike in the coming years is the company's unique positioning at the intersection of two large, and expanding, total addressable markets (TAMs): AI and cybersecurity. According to Statista, the TAM for AI in cybersecurity is expected to reach $134 billion by 2030 -- a more than fourfold increase compared to its size at the end of 2024.

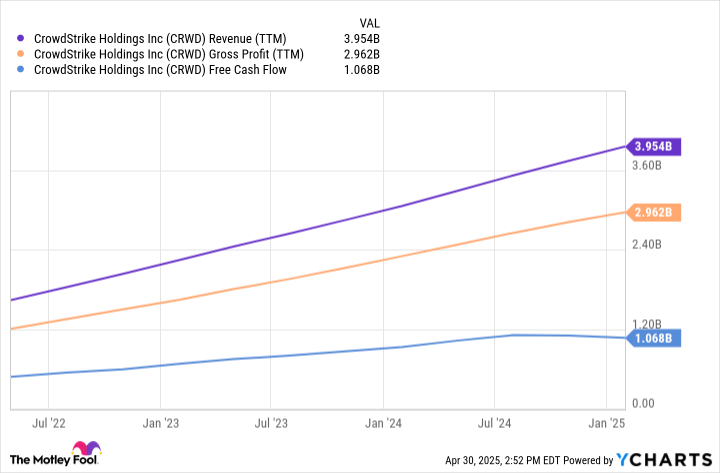

While the security outage last summer brought on much in the way of negative PR, CrowdStrike has chugged along and been performing quite well over the last several quarters. Despite any perceived reputational damage, the company's annual recurring revenue (ARR) continues to grow at an impressive clip and its ability to generate consistent free cash flow doesn't appear to be in jeopardy.

CRWD Revenue (TTM) data by YCharts.

CRWD Revenue (TTM) data by YCharts.

Is CrowdStrike stock a buy right now?

Similar to Palantir, CrowdStrike stock trades at a premium. In fact, CrowdStrike trades at the highest P/S ratio when benchmarked against a large peer group of leading cybersecurity businesses.

CRWD PS Ratio data by YCharts.

CRWD PS Ratio data by YCharts.

In a way, though, I think this premium suggests that growth investors are looking past the company's hiccups from last year and have bought into the long-run growth narrative surrounding AI and cybersecurity. Taking this one step further, despite CrowdStrike's premium, its current P/S multiple is actually slightly lower than where it was last year prior to the security outage -- as illustrated above around the July 2024 time frame.

I see CrowdStrike as a compelling buy-and-hold opportunity over the next several years and think the company's growth potential is in its early chapters. For these reasons, I think CrowdStrike has more tailwinds compared to Palantir, and I see the company becoming a higher-valued business by next decade.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10