Investment Thesis

ResMed is the global leader in the sleep apnea device market, holding approximately 48% of the share. Its core business encompasses high-profit CPAP devices, masks, and rapidly growing SaaS solutions. Benefiting from Philips' recall in 2021, the rising global OSA diagnosis rate and the aging demand, the compound annual growth rate of revenue from 2021 to 2024 exceeded 12%. Its "software and hardware integration" model integrates hardware and digital platforms, connects data of 28 million patients, drives recurring revenue and enhances patient dependence. The overall gross profit margin of the company has remained stable within the range of 56% to 60%, but both the operating profit margin and the net profit margin have improved significantly, reflecting the role of cost control and economies of scale. The current P/E ratio is 21x, lower than the five-year average of 32x. The target price for fiscal year 2026 is expected to be $295 (with a P/E ratio of 27x).

.jpg)

Source: TradingKey

The Global Sleep Health Crisis

According to the results of ResMed's fifth annual global sleep survey, global sleep quality showed a continuous downward trend in 2025. More than one-third of the respondents said they had difficulty falling asleep three or more times a week. The phenomenon of insufficient sleep has brought about profound impacts. It not only interferes with work performance and interpersonal relationships, but also poses a serious threat to physical and mental health.

Market Drivers for Sleep Apnea

Behind these sleep problems, sleep apnea disorder is an important but often overlooked factor. Sleep apnea is a disease characterized by repeated pauses in breathing during sleep, which can lead to sleep interruption, frequent awakenings and extreme daytime fatigue. This disease is more common among elderly patients and people with diseases such as diabetes, hypertension and cardiovascular diseases. Among them, obstructive sleep apnea (OSA) is the most common type of sleep apnea. According to the data released by the National Center for Biotechnology Information (NCBI) of the United States in 2023, approximately 936 million people worldwide suffer from mild to severe obstructive sleep apnea, and 425 million people suffer from moderate to severe OSA. It is expected that this figure will continue to rise as the aging population becomes increasingly severe. And this will drive the growth of the global sleep apnea treatment equipment market.

Sleep Apnea treatment equipment refers to medical devices used to treat Obstructive Sleep Apnea (OSA), mainly maintaining a normal breathing pattern by improving nighttime breathing and preventing airway collapse. The most common ones are Continuous Positive Airway Pressure (CPAP) devices. In addition, there are also bilevel positive airway pressure (BiPAP) devices, automatic positive airway pressure (APAP) devices and oral appliances, etc. According to the data from Future Market Insights, the global market size of sleep apnea treatment devices is expected to reach 9.794 billion US dollars in 2025. It is estimated that by 2035, the market size will reach approximately 24.81 billion US dollars, with a compound annual growth rate of nearly 10%.

Company Overview

ResMed is a globally leading medical device company headquartered in San Diego, USA. Founded in 1989, it focuses on respiratory care and sleep health. Its core products include CPAP devices for treating sleep apnea, bilayer ventilators, masks, and digital health solutions. ResMed holds approximately 48% of the global sleep apnea device market share and is a leader in this field. It provides products and services in over 140 countries with innovative technologies and extensive market coverage.

Source: Cpapdepot

Competitive Landscape

ResMed's technological innovation has established a strong patent barrier for it, which not only protects its core products and technologies but also restricts the entry of competitors. According to ResMed's 2024 annual report, as of June 30, 2024, ResMed held a total of approximately 9,711 global patents and design rights.

Its main competitors include Philips and Fisher & Paykel Healthcare. Among them, Philips was ResMed's biggest competitor, with approximately 3,000 patents. Previously, the global market share of sleep apnea devices once reached 30%. However, due to the product recall of CPAP devices in 2021 caused by foam issues, the patent portfolio was restricted after the recall, and the development of new products slowed down, among other factors, which led to a decline in market share to around 10%. The market share of Fisher & Paykel Healthcare is approximately 12% and it holds about 2,500 patents. Although it has exerted certain pressure on ResMed in the Asia-Pacific region, its software ecosystem is not as mature as that of ResMed.

Revenue Source Analysis

Source: ResMed, TradingKey

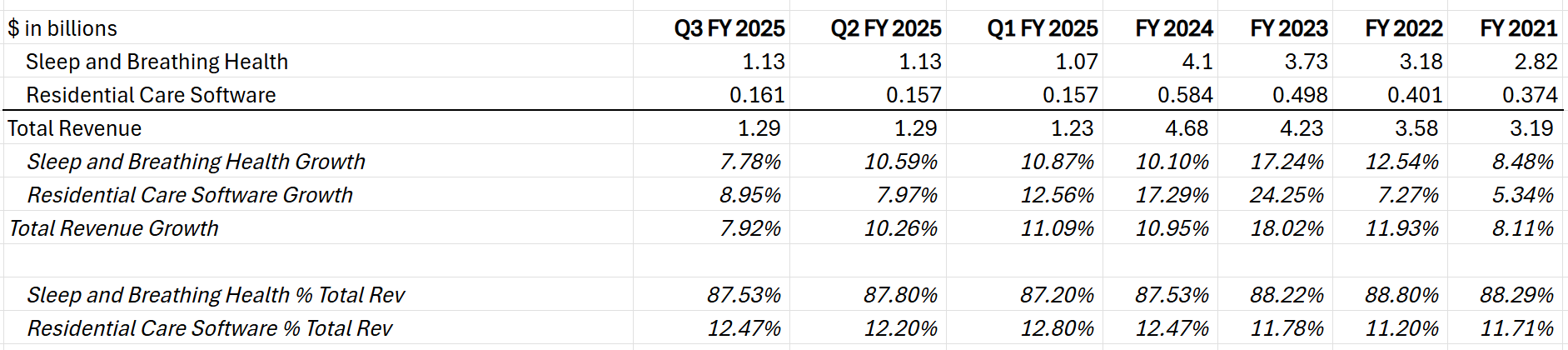

ResMed's revenue mainly comes from two parts: Sleep and Breathing Health and Residential Care Software.

Sleep and Breathing Health Business is ResMed's core business, covering Continuous Positive Airway Pressure (CPAP), bilayer ventilators, masks and related accessories. According to the latest data, the revenue from Sleep and Breathing Health Business accounts for more than 87% of the total revenue. Through its flagship products, the AirSense series and AirFit mask, it helps treat sleep apnea and chronic respiratory diseases, meeting the needs of patients worldwide. The revenue growth momentum over the past few years has mainly benefited from the shift in the market share of respiratory equipment due to the exit of competitors, as well as the increase in the global diagnosis rate of sleep apnea and the growth in demand from an aging population.

The Residential Care Software Business is ResMed's digital health business, providing cloud-based software solutions for patients through the software-as-a-service (SaaS) model, such as AirView (remote patient monitoring) and Brightree (out-of-hospital care management). Although this part of the revenue accounts for less than 13%, due to the popularization of telemedicine in recent years, its growth rate has been relatively fast and it will be a new growth point for ResMed in the future. In recent years, the revenue of this business has fluctuated significantly, primarily due to an accelerated acquisition pace to expand its SaaS business, extending from the U.S. market (CitusHealth, Somnoware) to Europe (MEDIFOX DAN, Inhealthcare), targeting aging populations and growing demand for out-of-hospital care, thus impacting the stability of this segment's revenue.

Understanding Its Business Model Through Financial Performance

Source: ResMed, TradingKey

ResMed's gross profit margin has remained stable at a high level of around 58% over the past few years. However, its operating profit margin and net profit margin have significantly increased. The operating profit margin has risen from nearly 24% in the past to over 32% currently, and the net profit margin has doubled from 13% in the fiscal year 2018 to 26% at present.

Source: ResMed, TradingKey

Persistently High Gross Profit Margin: ResMed's core business - Sleep and Breathing Health Business - adopts the "razor and blade" model. Devices (such as CPAP machines, accounting for approximately 60% of revenue) generate high profits, while consumables (such as regularly replaced masks, accounting for about 40%) provide stable recurring income. Over the past few years, the company has gradually withdrawn from low-profit businesses and focused on high-value-added areas such as sleep apnea and respiratory care. With the first-mover advantage, patent protection and differentiated design (such as the AirSense and AirFit series), ResMed products have strong pricing power, enabling them to maintain a high gross profit margin of 56%-60%.

Source: ResMed, TradingKey

Significantly Improved Operating Margin: ResMed has significantly enhanced operational efficiency through cost control and economies of scale. Research and development investment remained stable, while the proportion of sales, general and administrative (SG&A) expenses dropped from approximately 26% in 2018 to 19% recently. In addition, the company has expanded into the European and Asia-Pacific markets (such as Germany and Japan), taking advantage of the demand from an aging population and the rising diagnosis rate of sleep disorders to increase its revenue scale, effectively spread out fixed costs, and further optimize its operating profit margin.

Source: ResMed, TradingKey

Doubling of Net Profit Margin: On the basis of stable gross profit margin and improved operating profit margin, coupled with ResMed's continuous reduction of debt scale and thereby decrease in interest expenses, the company's overall net profit margin has doubled.

Source: ResMed, TradingKey

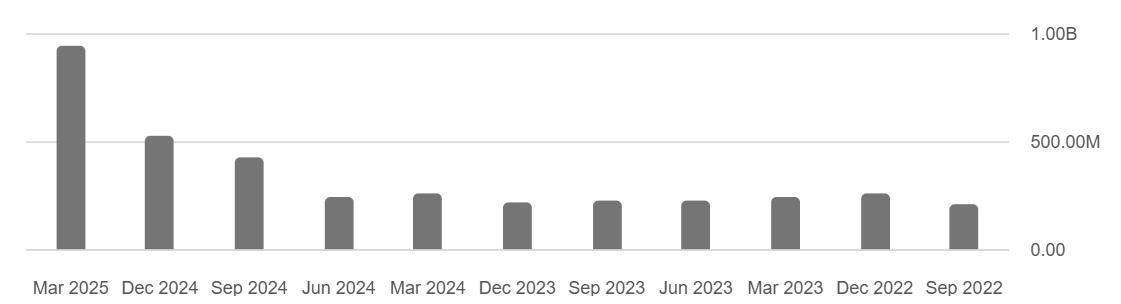

Significantly Increased Cash Flow: According to the company's latest data, ResMed's cash balance has reached 933 million US dollars, showing a significant increase compared to previous quarters. Furthermore, the company's free cash flow reached nearly 1.6 billion US dollars, and the low debt-to-equity ratio was only 0.15. A healthy balance sheet also provides strong support for ResMed's potential future mergers and acquisitions, enhancing its synergy and integration capabilities, enabling it to continue strengthening its digital health business.

Source: ResMed, Seeking Alpha

The Combination of Software & Hardware Model Contributes to Future Development

ResMed's business model combines hardware (such as CPAP devices and masks) and software (such as SaaS platforms, including AirView and myAir), forming an integrated model of "software and hardware integration". With the aging of the population and the rising incidence of chronic respiratory diseases, the demand for respiratory care equipment and services is expected to continue to grow.

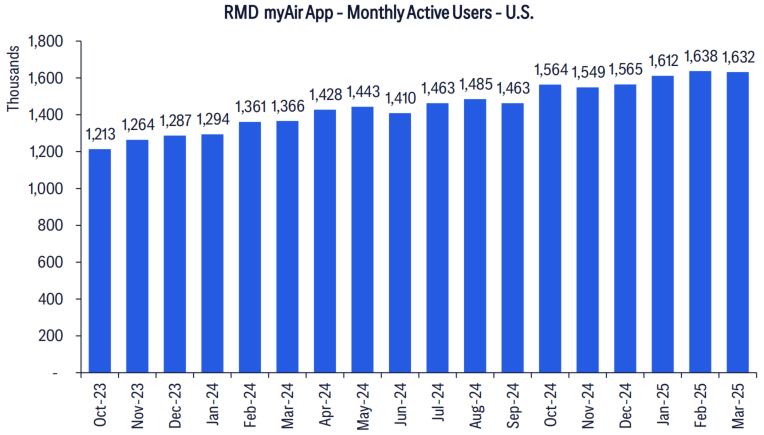

ResMed, through a model that combines software and hardware, provides end-to-end solutions for patients and medical institutions in terms of equipment, data management and remote monitoring, building a high barrier that is difficult for competitors to replicate in the short term. Its AirView platform serves over 28 million patients, and the myAir platform has over 8.3 million registered users, with the user base continuing to grow steadily. The user stickiness of myAir has significantly increased, with the average daily usage time rising from 5.5 hours to 6.5 hours, highlighting the efficiency of its digital health solutions. ResMed's 2030 strategic goal is to benefit 500 million people, indicating that its market potential will expand significantly. With the massive data generated by devices and platforms, ResMed can predict maintenance needs, optimize treatment plans and develop new services. This data-driven innovation ensures its leading position in the medical device field.

Source: Citi Research, Sensor Tower

Outlook and Valuation

Despite the challenges of the global trade environment, such as the persistent tariff issue, products used to treat chronic respiratory diseases are exempt from tariffs, which significantly reduces the potential adverse impact on ResMed's profits. At present, its core products are mainly sold through authorized dealers and distributors, with direct sales and medical institution sales accounting for a relatively small proportion. However, the company stated that it will continuously increase investment in digital platforms and direct sales channels, reduce reliance on traditional distribution, which will significantly lower its sales costs and enhance customer reach. Nevertheless, the increase in the proportion of direct sales may have a potential impact on market share due to the restrictions on medical insurance reimbursement coverage. With the supply chain almost returning to the pre-pandemic level, the full transition to the AirSense 11 platform will be completed by the end of 2025. We believe that ResMed will achieve the goal of a gross profit margin of over 60% in fiscal year 2026. EPS is expected to increase by 20% year-on-year in the fourth quarter of fiscal year 2025 and by 15% year-on-year to $10.93 in fiscal year 2026.

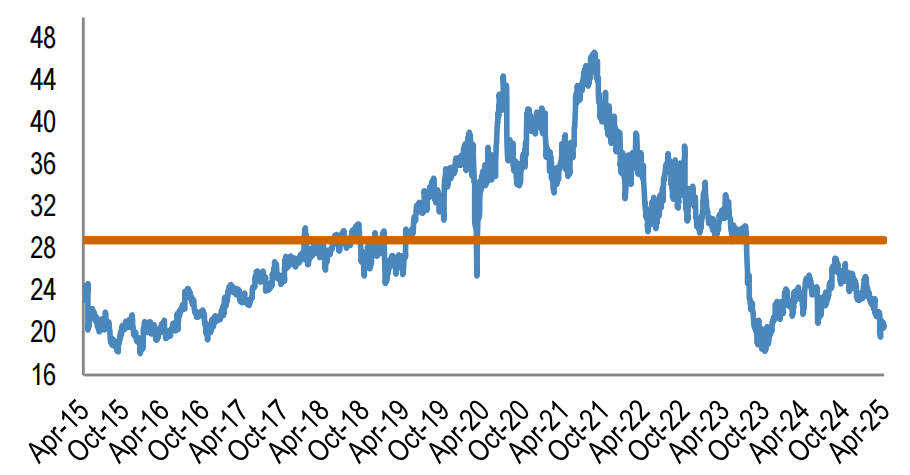

ResMed's current P/E ratio is 21x, which is lower than the 5-year average of approximately 32x and the 10-year average of approximately 29x. We expect ResMed to maintain its global market leadership and further expand its market share, leveraging its robust product portfolio and business model. Our target price of $295 corresponds to an approximate 27x P/E ratio, aligning closely with the industry average valuation. We believe that as its SaaS business becomes increasingly mature and its revenue share continues to rise, it will help further enhance its valuation level.

Source: Bloomberg Finance L.P.

Risk

The downside risks faced by ResMed include: The strong performance of emerging CPAP competitors may lead to sales falling short of expectations; Tariff changes or unexpected events may have a negative impact, although it is currently limited. In the long term, new evidence of weight loss drugs and therapies such as GLP-1 may shrink the target market size.

Find out more