How Investors May Respond To Simmons First National (SFNC) Q2 Earnings Growth Despite Higher Charge-Offs

- Simmons First National Corporation recently reported second quarter results, posting net interest income of US$171.82 million and net income of US$54.77 million, both higher than the same period last year, while net loans charged off grew to US$10.58 million compared to US$8.08 million a year ago.

- An interesting insight is that, despite increased charge-offs, the company delivered improved earnings alongside unchanged buyback activity during the quarter, suggesting operational resilience.

- We'll examine how Simmons First National's strong net interest income growth influences its overall investment narrative and outlook.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Simmons First National Investment Narrative Recap

To be a shareholder in Simmons First National, you need confidence in its ability to drive sustained earnings growth while managing asset quality risks and navigating a competitive deposit environment. The latest quarter’s strong net interest income and improved net income, even as net charge-offs increased, do not materially affect the most important short-term catalyst: further improvement in net interest margins, while the biggest risk remains asset quality concerns that could lead to unforeseen credit losses.

Among the recent company announcements, the report of increased net loans charged off this quarter is directly tied to concerns about asset quality. Although earnings performance has shown resilience, continued elevation in charge-offs draws attention to underlying credit trends, which remain a critical focus given current economic caution and past moves of certain loans to nonperforming status.

However, investors should also be aware that ongoing resilience in net earnings can be clouded by concerns about future unexpected credit losses, especially if asset quality were to deteriorate...

Read the full narrative on Simmons First National (it's free!)

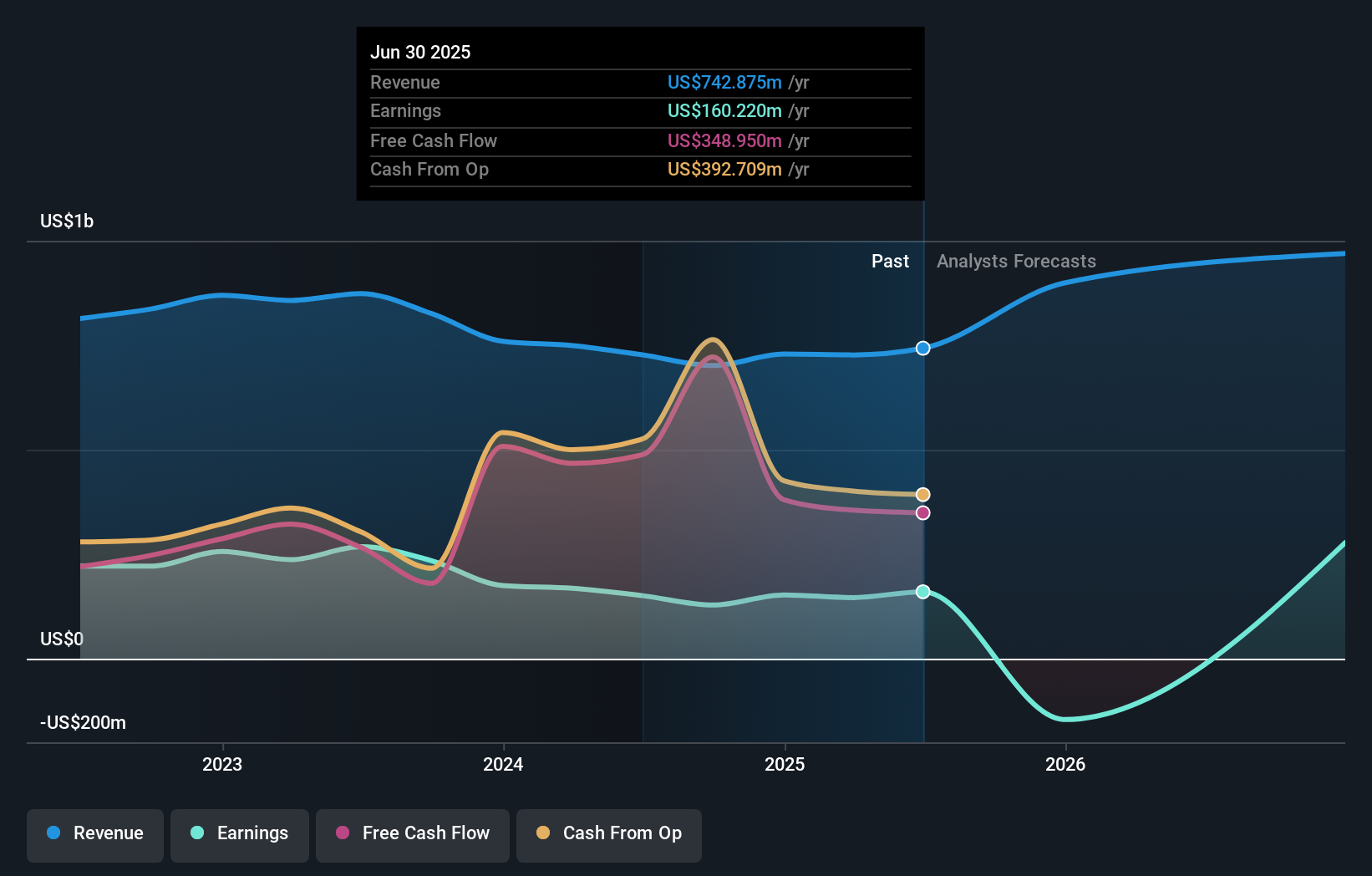

Simmons First National's narrative projects $1.1 billion in revenue and $316.0 million in earnings by 2028. This requires 16.5% yearly revenue growth and a $169.8 million earnings increase from current earnings of $146.2 million.

Uncover how Simmons First National's forecasts yield a $21.60 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community contributors have set fair values for Simmons First National ranging from US$21.60 to US$25.07. While these estimates vary, many also point out that persistent asset quality pressures may weigh on future returns, making it important to review the range of community insights before making up your mind.

Explore 2 other fair value estimates on Simmons First National - why the stock might be worth just $21.60!

Build Your Own Simmons First National Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Simmons First National research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Simmons First National research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Simmons First National's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10