Most Shareholders Will Probably Agree With MYP Ltd.'s (SGX:F86) CEO Compensation

Key Insights

- MYP to hold its Annual General Meeting on 25th of July

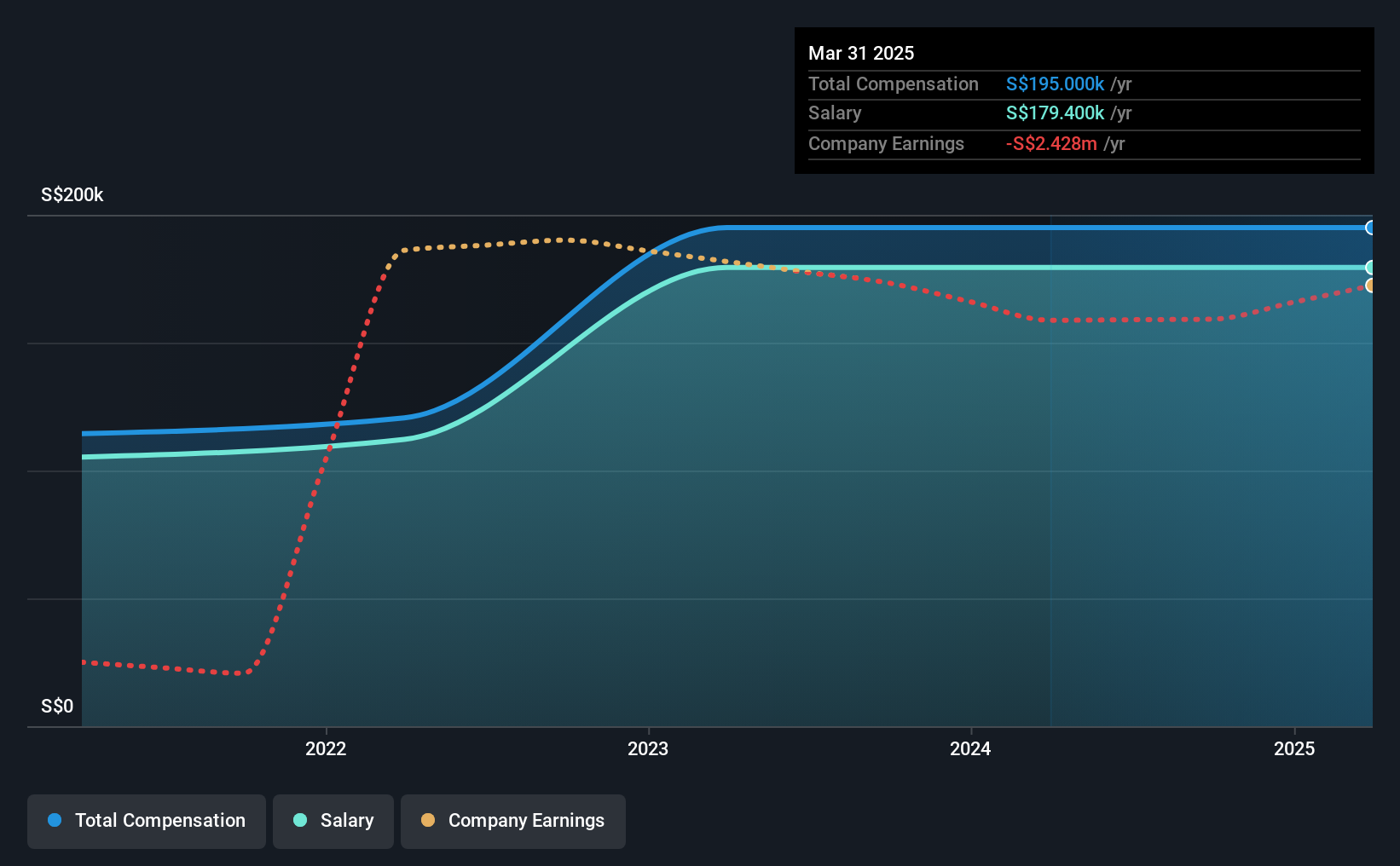

- CEO Jonathan Tahir's total compensation includes salary of S$179.4k

- Total compensation is 52% below industry average

- MYP's total shareholder return over the past three years was 21% while its EPS was down 98% over the past three years

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

The performance at MYP Ltd. (SGX:F86) has been rather lacklustre of late and shareholders may be wondering what CEO Jonathan Tahir is planning to do about this. At the next AGM coming up on 25th of July, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for MYP

How Does Total Compensation For Jonathan Tahir Compare With Other Companies In The Industry?

At the time of writing, our data shows that MYP Ltd. has a market capitalization of S$119m, and reported total annual CEO compensation of S$195k for the year to March 2025. This was the same amount the CEO received in the prior year. Notably, the salary which is S$179.4k, represents most of the total compensation being paid.

On comparing similar-sized companies in the Singaporean Real Estate industry with market capitalizations below S$257m, we found that the median total CEO compensation was S$403k. Accordingly, MYP pays its CEO under the industry median. What's more, Jonathan Tahir holds S$103m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | S$179k | S$179k | 92% |

| Other | S$16k | S$16k | 8% |

| Total Compensation | S$195k | S$195k | 100% |

Talking in terms of the industry, salary represented approximately 64% of total compensation out of all the companies we analyzed, while other remuneration made up 36% of the pie. MYP is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at MYP Ltd.'s Growth Numbers

Over the last three years, MYP Ltd. has shrunk its earnings per share by 98% per year. Its revenue is up 2.4% over the last year.

Overall this is not a very positive result for shareholders. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has MYP Ltd. Been A Good Investment?

MYP Ltd. has served shareholders reasonably well, with a total return of 21% over three years. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

While it's true that shareholders have seen decent returns, it's hard to overlook the lack of earnings growth and this makes us wonder if the current returns can continue. Shareholders might want to question the board about these concerns, and revisit their investment thesis for the company.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 2 warning signs for MYP you should be aware of, and 1 of them shouldn't be ignored.

Important note: MYP is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10