TradingKey - As Arm Holdings (ARM) shows increasing signs of entering the ASIC chip manufacturing space, analysts are revising their valuations higher — with BNP Paribas recently doubling its price target from $110 to $210, and upgrading the stock from “Neutral” to “Outperform”.

On Wednesday, July 16, BNP Paribas released a new research note stating that with major tech firms continuing to increase their AI capital expenditures, Arm is well-positioned to naturally expand into the application-specific integrated circuit (ASIC) market — a move that could significantly broaden its value proposition.

Arm’s current business model is built on licensing its chip architecture to other manufacturers. Wall Street has been broadly optimistic about the company’s role in the AI PC boom — but the new ASIC narrative may be underappreciated by the broader market.

While Arm has not officially commented on its ASIC strategy, reports as early as mid-2024 indicated the company was expanding from chip design into in-house AI chip development, with ambitions to enter the data center market.

In February 2025, the Financial Times reported that Arm was preparing to launch a new AI chip — with Meta as a potential early buyer.

The ASIC Opportunity

BNP Paribas analysts estimate that if Arm captures 7% of the ASIC market, its EBITDA could double.

They project the ASIC market to reach $200 billion by 2030, and that Arm could generate $8–15 billion in revenue from its ASIC business by FY2030–FY2031.

Currently, the ASIC market is dominated by players like Broadcom (AVGO) and Marvell Technology (MRVL). Arm’s potential entry would bring a new heavyweight to the competition.

While some existing clients may be wary of Arm’s shift into manufacturing — which could create vertical integration concerns — BNP Paribas argues that the risk-reward tradeoff is justified.

Having both chip design and production capabilities would allow Arm to capture more value across the AI supply chain — a key advantage in the evolving tech landscape.

Market Hasn’t Fully Priced In the ASIC Potential

BNP Paribas analysts noted that current market valuations have not yet priced in Arm’s potential in the ASIC space — suggesting significant upside potential.

They believe that once Arm’s ASIC strategy becomes more concrete, investor sentiment could shift dramatically — unlocking a new wave of growth for the company.

As of July 17, ahead of U.S. markets’ opening, ARM shares rose 2% in pre-market trading.

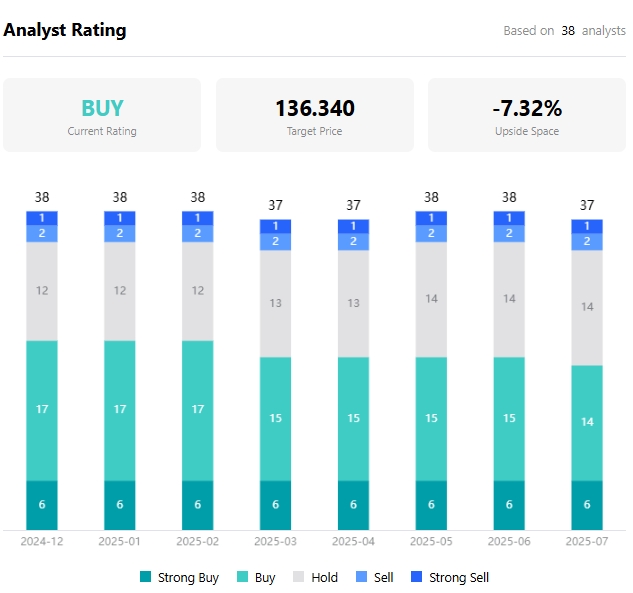

According to TradingKey, the current average analyst price target for ARM is $136.34, down over 7% from the latest closed price.

Analyst Price Targets for ARM, Source: TradingKey

Find out more