Whitehaven Coal Limited's (ASX:WHC) Share Price Boosted 29% But Its Business Prospects Need A Lift Too

Whitehaven Coal Limited (ASX:WHC) shares have continued their recent momentum with a 29% gain in the last month alone. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 7.9% in the last twelve months.

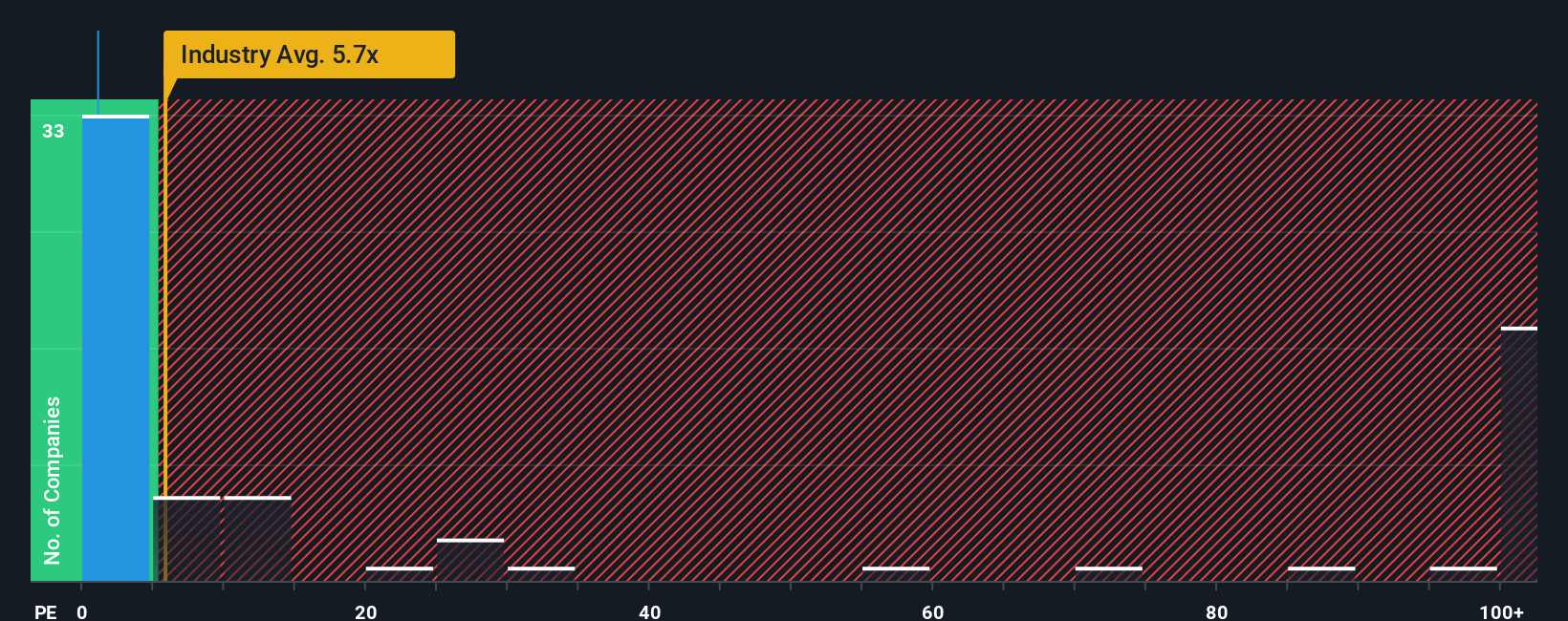

Although its price has surged higher, Whitehaven Coal may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.1x, since almost half of all companies in the Oil and Gas industry in Australia have P/S ratios greater than 5.7x and even P/S higher than 110x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Trump has pledged to "unleash" American oil and gas and these 15 US stocks have developments that are poised to benefit.

Check out our latest analysis for Whitehaven Coal

What Does Whitehaven Coal's P/S Mean For Shareholders?

With its revenue growth in positive territory compared to the declining revenue of most other companies, Whitehaven Coal has been doing quite well of late. One possibility is that the P/S ratio is low because investors think the company's revenue is going to fall away like everyone else's soon. Those who are bullish on Whitehaven Coal will be hoping that this isn't the case and the company continues to beat out the industry.

Keen to find out how analysts think Whitehaven Coal's future stacks up against the industry? In that case, our free report is a great place to start.How Is Whitehaven Coal's Revenue Growth Trending?

In order to justify its P/S ratio, Whitehaven Coal would need to produce anemic growth that's substantially trailing the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 47%. The strong recent performance means it was also able to grow revenue by 146% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 2.2% per year as estimated by the nine analysts watching the company. With the industry predicted to deliver 1,003% growth per year, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Whitehaven Coal's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What Does Whitehaven Coal's P/S Mean For Investors?

Even after such a strong price move, Whitehaven Coal's P/S still trails the rest of the industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Whitehaven Coal's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Whitehaven Coal that you should be aware of.

If you're unsure about the strength of Whitehaven Coal's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Whitehaven Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10