3 ASX Dividend Stocks Yielding Up To 6.4%

As the Australian market experiences a buoyant day led by strong performances in materials and utilities, investors are keenly observing sectors that can offer stability amid fluctuating commodity prices and international trade developments. In this context, dividend stocks stand out as attractive options for those seeking consistent income, especially when they yield up to 6.4%, providing a potential buffer against market volatility.

Top 10 Dividend Stocks In Australia

| Name | Dividend Yield | Dividend Rating |

| Super Retail Group (ASX:SUL) | 7.86% | ★★★★★☆ |

| Sugar Terminals (NSX:SUG) | 8.20% | ★★★★★☆ |

| Ricegrowers (ASX:SGLLV) | 5.91% | ★★★★★☆ |

| Nick Scali (ASX:NCK) | 3.19% | ★★★★★☆ |

| New Hope (ASX:NHC) | 9.36% | ★★★★★☆ |

| Lycopodium (ASX:LYL) | 6.56% | ★★★★★☆ |

| Lindsay Australia (ASX:LAU) | 6.99% | ★★★★★☆ |

| IPH (ASX:IPH) | 6.67% | ★★★★★☆ |

| Fiducian Group (ASX:FID) | 3.75% | ★★★★★☆ |

| Accent Group (ASX:AX1) | 6.71% | ★★★★★☆ |

Click here to see the full list of 29 stocks from our Top ASX Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

Amotiv (ASX:AOV)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Amotiv Limited, with a market cap of A$1.19 billion, operates through its subsidiaries to manufacture, import, distribute, and sell automotive products across Australia, New Zealand, Thailand, South Korea, France, and the United States.

Operations: Amotiv Limited generates revenue through its segments: Powertrain & Undercar (A$322.90 million), Lighting Power & Electrical (A$329.97 million), and 4WD Accessories & Trailering (A$345.41 million).

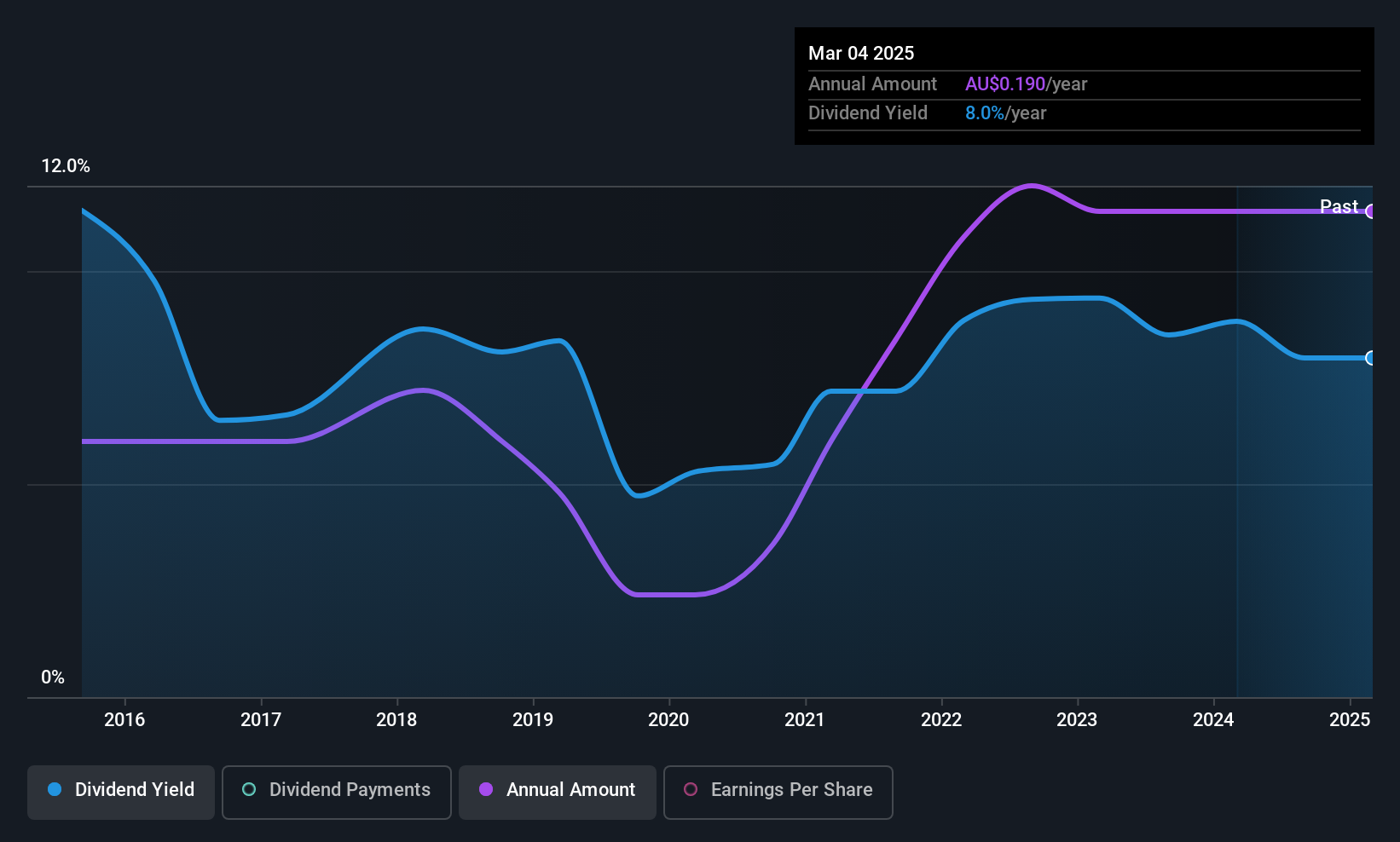

Dividend Yield: 4.6%

Amotiv's dividend payments have been volatile over the past decade, though they have shown growth. Currently, the dividend yield of 4.62% is below the top quartile of Australian dividend payers. Despite this, Amotiv offers a reasonable payout ratio of 70.1%, indicating dividends are well-covered by earnings and cash flows. Trading at a significant discount to its estimated fair value, Amotiv presents good relative value compared to peers and industry standards amidst upcoming leadership changes with James Fazzino as Chair-elect.

- Navigate through the intricacies of Amotiv with our comprehensive dividend report here.

- Upon reviewing our latest valuation report, Amotiv's share price might be too pessimistic.

GR Engineering Services (ASX:GNG)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: GR Engineering Services Limited offers engineering, procurement, and construction services to the mining and mineral processing industries both in Australia and internationally, with a market cap of A$602.67 million.

Operations: GR Engineering Services Limited generates revenue through its Oil and Gas segment, which accounts for A$96.61 million, and its Mineral Processing segment, contributing A$412.30 million.

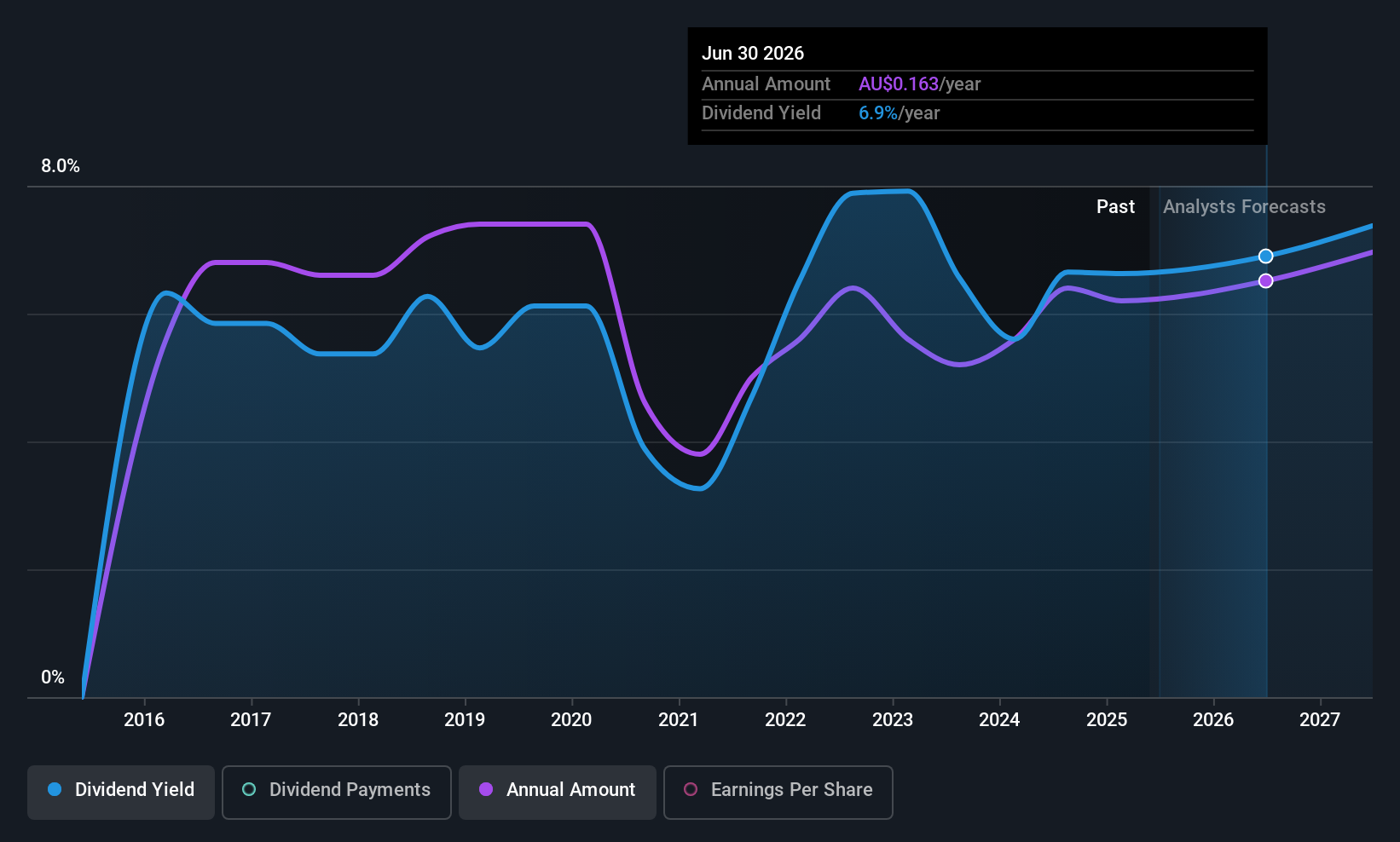

Dividend Yield: 5.6%

GR Engineering Services offers a dividend yield of 5.56%, slightly below the top quartile of Australian dividend payers. Its dividends are well-covered by earnings, with a payout ratio of 86%, and cash flows, at a cash payout ratio of 37.6%. Despite an unstable dividend history over the past decade, there has been growth in dividend payments during this period. The stock trades significantly below its estimated fair value, suggesting potential value for investors.

- Click here and access our complete dividend analysis report to understand the dynamics of GR Engineering Services.

- Our valuation report here indicates GR Engineering Services may be overvalued.

GWA Group (ASX:GWA)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: GWA Group Limited is involved in the research, design, manufacture, importation, and marketing of building fixtures and fittings for residential and commercial properties across Australia, New Zealand, and international markets with a market cap of A$636.49 million.

Operations: GWA Group's revenue is primarily derived from its Water Solutions segment, which generated A$417.40 million.

Dividend Yield: 6.5%

GWA Group's dividend yield of 6.46% places it among the top 25% in Australia, but its sustainability is questionable with a high payout ratio of 111.7%, indicating dividends are not well-covered by earnings. Cash flows do cover payouts, with a cash payout ratio of 71.9%. The company's dividend history is volatile and unreliable over the past decade despite increases. Trading at a significant discount to fair value suggests potential investment appeal amidst recent board changes.

- Click to explore a detailed breakdown of our findings in GWA Group's dividend report.

- The analysis detailed in our GWA Group valuation report hints at an deflated share price compared to its estimated value.

Make It Happen

- Click this link to deep-dive into the 29 companies within our Top ASX Dividend Stocks screener.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10