Pfizer (PFE) Faces Legal Challenges Over Depo-Provera's Increased Brain Tumor Risk

Pfizer (PFE) is currently under significant scrutiny due to a study linking its product, Depo-Provera, to increased health risks, and an associated Multi-District Litigation could have influenced its recent share price performance. Despite reporting a 11% quarterly price movement, Pfizer's stock behavior aligns with broader market trends, which showed an 18% rise over the past year. Positive developments, such as successful trial results for XTANDI and HYMPAVZI™, contributed positively but were countered by legal challenges and safety concerns. These opposing factors underscore Pfizer's mixed quarter performance, balancing robust product news against adverse legal implications.

We've spotted 3 possible red flags for Pfizer you should be aware of.

The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

The recent scrutiny surrounding Pfizer due to health risks linked with Depo-Provera and subsequent litigation is likely influencing the narrative of declining revenue and earnings projections. If legal challenges intensify, they could potentially exacerbate financial pressure, hindering near-term growth prospects. While Pfizer continues to face turbulent times, the company's share price experienced a 11% rise over the past three months amid a volatile 18 months, during which the total return was a 9.75% decline over the past year. The company also underperformed compared to the US Pharmaceuticals industry, which saw a decline of 7.2% over the same period. This signals potential investor hesitance stemming from ongoing legal matters and competitive pressures affecting core products like Vyndaqel and Paxlovid.

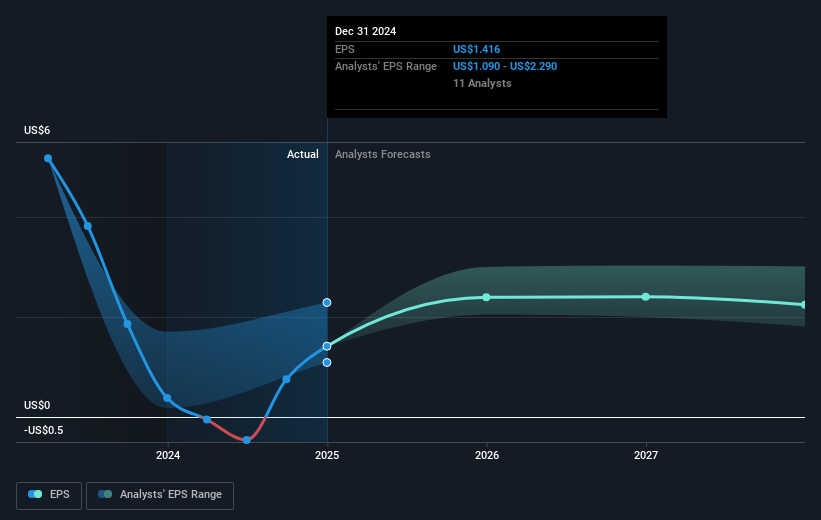

In light of the factors detailed in the narrative, Pfizer's revenue and earnings forecasts are expected to encounter downward pressure. Analysts are projecting a potential revenue decline of 2.4% annually over the next three years. Such a decline, combined with the increased legal scrutiny, could affect Pfizer's earnings growth, projected at an annual 5.8% increase, which is slower than the broader US market's projected growth of 14.9%. Despite challenges, the share price's discount of approximately 15.3% to the current consensus price target of US$29.23 might suggest potential upside if revenue growth expectations and profitability improve. Investors need to consistently evaluate these variables as the legal situation unfolds, and market conditions evolve.

The analysis detailed in our Pfizer valuation report hints at an deflated share price compared to its estimated value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10