Is The Market Rewarding China Resources Gas Group Limited (HKG:1193) With A Negative Sentiment As A Result Of Its Mixed Fundamentals?

With its stock down 7.6% over the past three months, it is easy to disregard China Resources Gas Group (HKG:1193). It seems that the market might have completely ignored the positive aspects of the company's fundamentals and decided to weigh-in more on the negative aspects. Long-term fundamentals are usually what drive market outcomes, so it's worth paying close attention. Particularly, we will be paying attention to China Resources Gas Group's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for China Resources Gas Group is:

9.0% = HK$5.7b ÷ HK$64b (Based on the trailing twelve months to December 2024).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each HK$1 of shareholders' capital it has, the company made HK$0.09 in profit.

See our latest analysis for China Resources Gas Group

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

China Resources Gas Group's Earnings Growth And 9.0% ROE

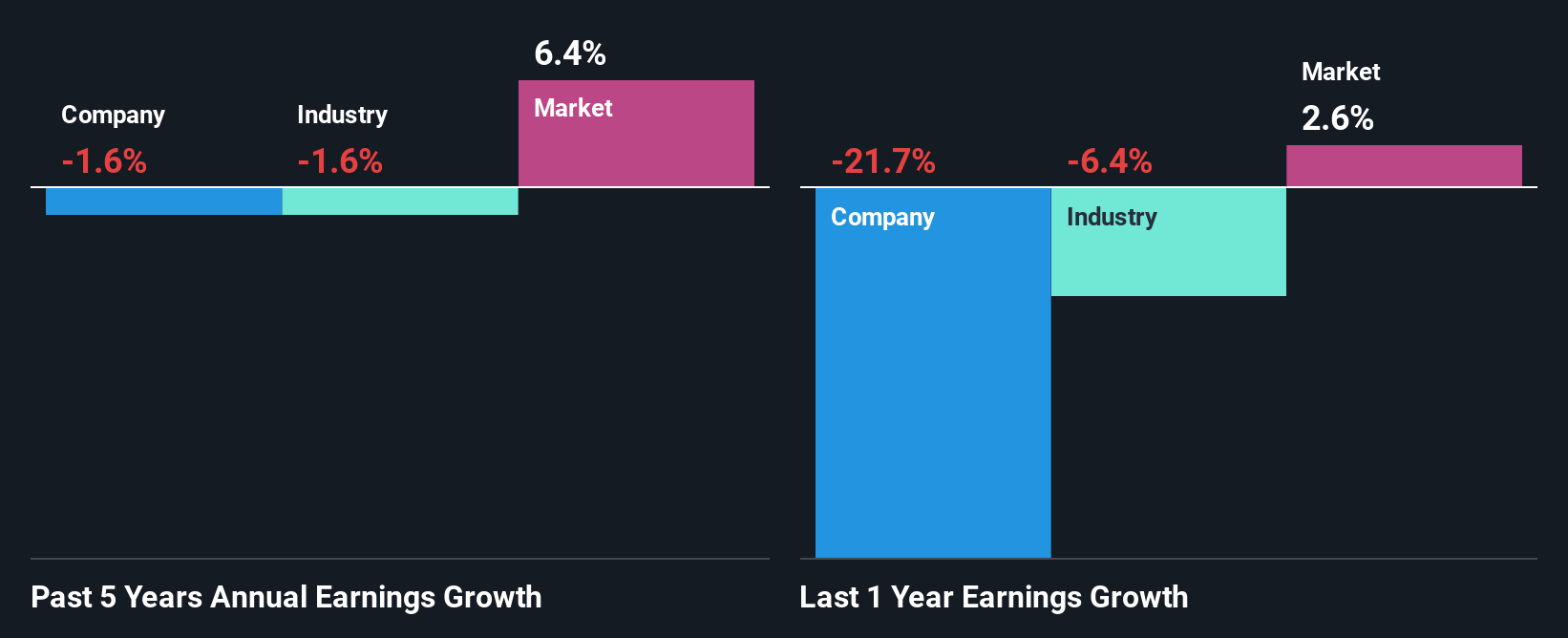

When you first look at it, China Resources Gas Group's ROE doesn't look that attractive. However, given that the company's ROE is similar to the average industry ROE of 9.1%, we may spare it some thought. However, China Resources Gas Group has seen a flattish net income growth over the past five years, which is not saying much. Remember, the company's ROE is not particularly great to begin with. So that could also be one of the reasons behind the company's flat growth in earnings.

Next, on comparing with the industry net income growth, we found that China Resources Gas Group's earnings seems to be shrinking at a similar rate as the industry which shrunk at a rate of a rate of 1.6% in the same period.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is China Resources Gas Group fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is China Resources Gas Group Using Its Retained Earnings Effectively?

In spite of a normal three-year median payout ratio of 48% (or a retention ratio of 52%), China Resources Gas Group hasn't seen much growth in its earnings. So there could be some other explanation in that regard. For instance, the company's business may be deteriorating.

In addition, China Resources Gas Group has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 56%. Therefore, the company's future ROE is also not expected to change by much with analysts predicting an ROE of 10%.

Conclusion

In total, we're a bit ambivalent about China Resources Gas Group's performance. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10