Does the Strata Elite Launch Mark a Turning Point for Citigroup's High-End Strategy (C)?

- Earlier this week, Citigroup launched its new Strata Elite premium credit card and saw analysts raise their earnings forecasts, signaling fresh optimism in the company's near-term outlook.

- This move into the high-end credit card segment highlights Citigroup's efforts to expand its presence among affluent customers and diversify sources of fee income.

- We'll explore how the launch of Strata Elite could support Citigroup's push for higher-margin growth and digital innovation.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Citigroup Investment Narrative Recap

To be a Citigroup shareholder, you need to believe the company can turn its scale, global payments network, and digital upgrades, like the Strata Elite card, into higher-margin revenue despite regulatory scrutiny and rising competition from fintechs. The recent premium card launch is an interesting near-term catalyst, but it does not alter the biggest risk: mounting compliance costs and operational complexity from ongoing regulatory constraints.

One announcement that ties into these catalysts is Citi's July 18 partnership with Ant International for enhanced FX risk management solutions, which directly supports ongoing efforts to improve fee income and position the bank as a leader in innovative cross-border services.

Yet, in contrast to new product rollouts, investors should not ignore the ongoing regulatory pressures and transformation costs that continue to ...

Read the full narrative on Citigroup (it's free!)

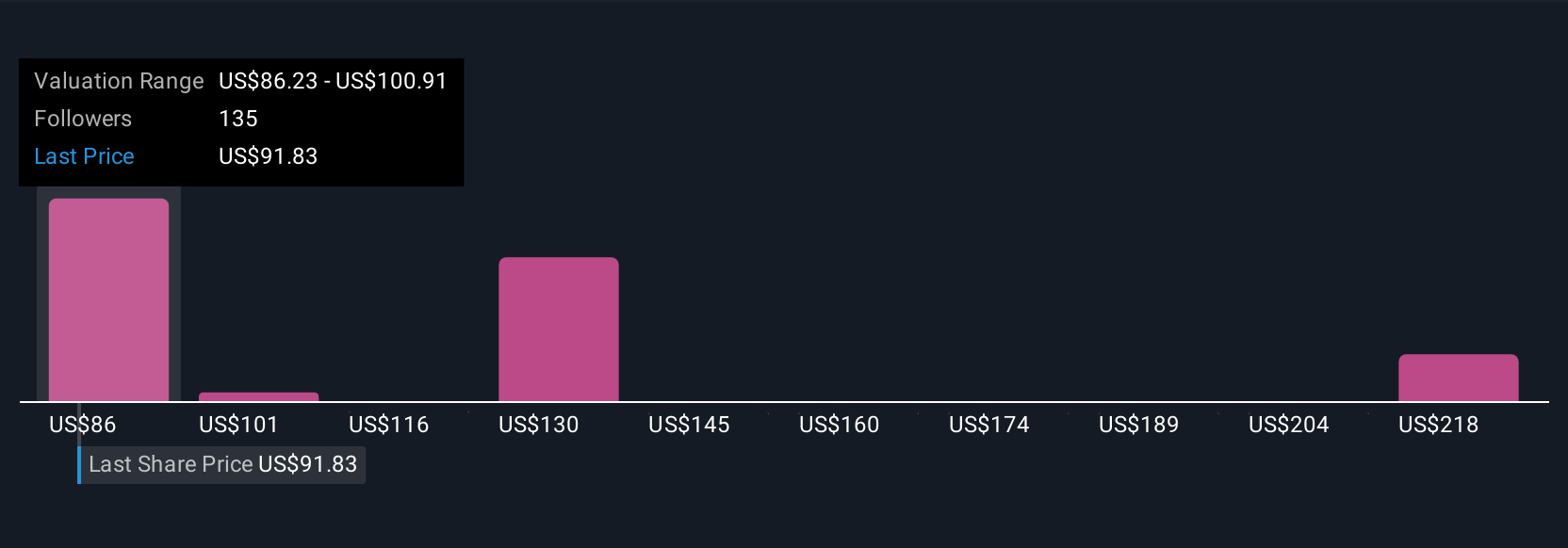

Citigroup's narrative projects $95.2 billion revenue and $17.0 billion earnings by 2028. This requires 9.1% yearly revenue growth and a $4.1 billion earnings increase from $12.9 billion today.

Uncover how Citigroup's forecasts yield a $99.45 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts predicted Citigroup’s revenues could reach US$91.3 billion and earnings US$20.0 billion by 2028, banking on significant benefits from AI and wealth management growth. These projections are far above consensus, so it is important to consider how new events might affect the wide range of expectations and invite you to explore different viewpoints.

Explore 9 other fair value estimates on Citigroup - why the stock might be worth over 2x more than the current price!

Build Your Own Citigroup Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Citigroup research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 25 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10