How Investors May Respond To W. P. Carey (WPC) Revenue Growth Amid Falling Net Income

- W. P. Carey Inc. recently announced its second-quarter and first-half 2025 results, showing that revenue increased to US$430.78 million and US$840.64 million, respectively, but net income fell to US$51.22 million and US$177.04 million over the same periods compared to the previous year.

- This contrast between higher revenue and sharply lower profitability highlights potential pressure on margins or increased costs impacting the bottom line, despite top-line growth.

- We'll examine how this drop in net income, despite solid revenue gains, may alter W. P. Carey's longer-term investment narrative.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

W. P. Carey Investment Narrative Recap

To be a shareholder in W. P. Carey, you generally need confidence in the company's ability to deliver stable, long-term income from its diverse, global real estate portfolio. While recent second-quarter results underscored continued revenue growth, the steep drop in net income raises fresh questions around short-term margin pressure, though for now, this headline result does not appear to drastically alter the biggest catalyst of a strong deal pipeline, nor the primary risk of tenant weakness in key European markets.

The recent increase in the quarterly dividend to US$0.90 per share, announced in June, stands out as especially relevant against the backdrop of declining earnings. This move may reassure income-focused investors that management remains committed to regular cash returns, even as margin and profit dynamics fluctuate in the near term.

Yet in contrast, investors should take note that revenue gains may not always protect against...

Read the full narrative on W. P. Carey (it's free!)

W. P. Carey’s outlook points to $1.9 billion in revenue and $639.5 million in earnings by 2028. This scenario assumes a 6.5% annual revenue growth and a $212 million increase in earnings from the current $427.4 million.

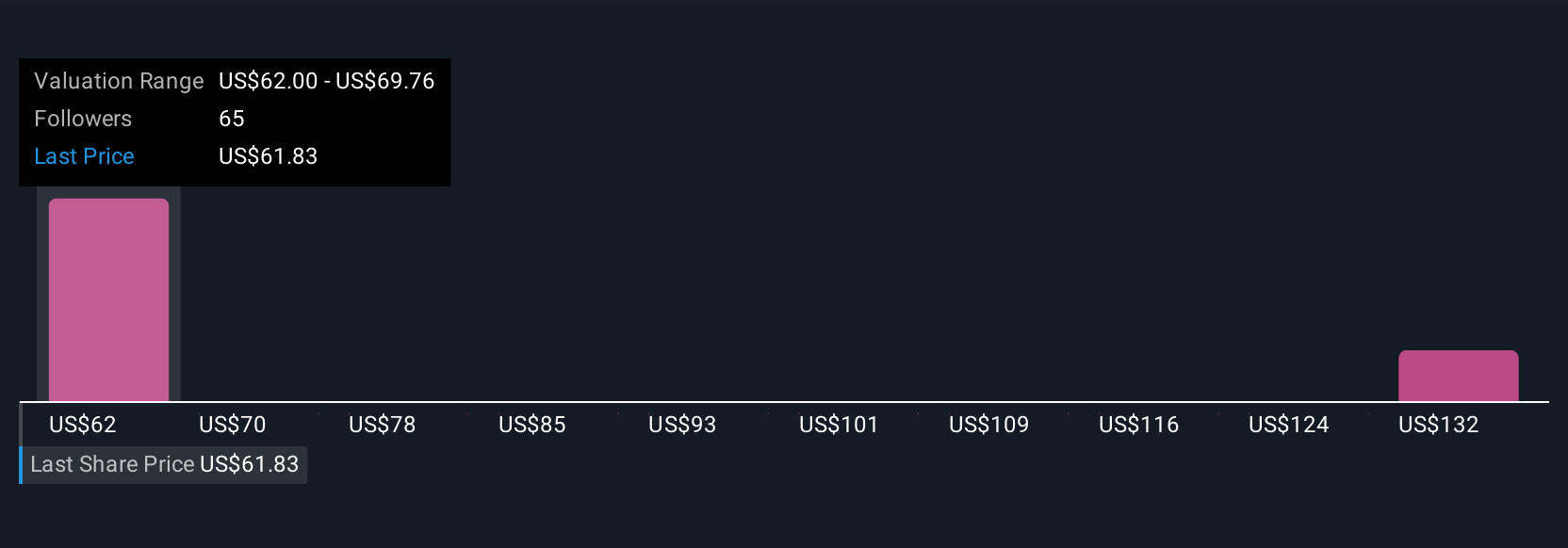

Uncover how W. P. Carey's forecasts yield a $64.36 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members offered three distinct fair value estimates for W. P. Carey, spanning from US$62 to US$141.21 per share. Several see opportunity in deal flow, but differing views on tenant risk and margin pressure highlight why it pays to weigh multiple outlooks.

Explore 3 other fair value estimates on W. P. Carey - why the stock might be worth over 2x more than the current price!

Build Your Own W. P. Carey Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your W. P. Carey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free W. P. Carey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. P. Carey's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W. P. Carey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10