Did Coherent's (COHR) AI Partnership and New Optical Chip Just Shift Its Investment Narrative?

- In late July 2025, Coherent announced the launch of its 56 Gbaud PAM4 transimpedance amplifier for next-generation optical transceivers and revealed a new partnership with Bell Canada to provide proprietary, secure AI solutions for government and enterprise customers across Canada.

- These developments highlight Coherent's focus on expanding its reach in AI and communications markets, while also reinforcing the company's commitment to innovation and deepening industry collaborations.

- We'll examine how the partnership with Bell Canada could accelerate Coherent's expansion into sovereign AI and enterprise infrastructure markets.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Coherent Investment Narrative Recap

To own Coherent, you have to believe in the company's ability to deliver innovative technologies for optical communications and AI markets, while managing near-term pressure in its industrial and materials business. The Bell Canada partnership sharpens Coherent’s competitive edge in sovereign AI and enterprise infrastructure, bringing the potential to influence revenue trajectories, but does not fundamentally alter the short-term catalyst, which continues to hinge on successful portfolio optimization and margin improvement, nor does it eliminate the overriding risk from softness in industrial demand.

Among recent announcements, Coherent’s July launch of the 56 Gbaud PAM4 transimpedance amplifier is directly relevant, as it underscores the company's push to expand its optical communications portfolio, an area closely tied to its growth catalyst of advanced datacenter and telecommunication products ramping up over the next quarters.

However, against these growth opportunities, investors should not lose sight of ongoing risks around

Read the full narrative on Coherent (it's free!)

Coherent's outlook projects $7.2 billion in revenue and $650.7 million in earnings by 2028. This assumes 8.5% annual revenue growth and a $682.4 million increase in earnings from the current level of -$31.7 million.

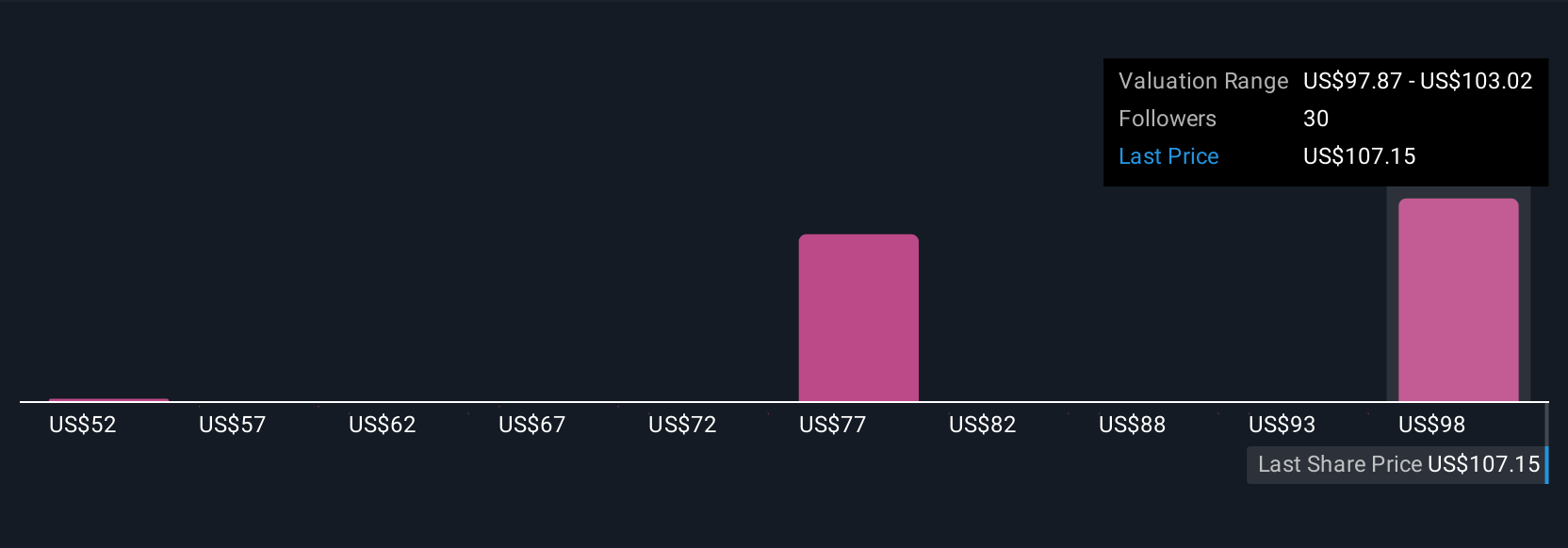

Uncover how Coherent's forecasts yield a $103.02 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members contributed 6 fair value estimates for Coherent ranging from US$51.56 to US$103.02 per share. While the company’s efforts in portfolio optimization remain a key short-term catalyst, you’ll find contrasting views on how this could impact future earnings and share value, explore several perspectives to challenge your own assumptions.

Explore 6 other fair value estimates on Coherent - why the stock might be worth as much as $103.02!

Build Your Own Coherent Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Coherent research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free Coherent research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coherent's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10