CRENESSITY's Breakout Launch Might Change the Case for Investing in Neurocrine Biosciences (NBIX)

- Neurocrine Biosciences recently reported second-quarter 2025 earnings, with revenue rising to US$687.5 million and net income reaching US$107.5 million, both higher than the previous year on strong demand for INGREZZA and CRENESSITY.

- CRENESSITY's launch surpassed the company's expectations, with rapid adoption by endocrinologists and encouraging clinical feedback pointing to future commercial potential.

- We'll look at how this increased commercial strength for CRENESSITY might influence Neurocrine Biosciences' longer-term outlook and investment narrative.

These 19 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Neurocrine Biosciences Investment Narrative Recap

The core of the Neurocrine Biosciences investment case centers on the company’s ability to drive long-term growth through expanding product adoption, particularly of INGREZZA and CRENESSITY, while continuing to advance its clinical pipeline. The strong second-quarter results, fueled by above-expected CRENESSITY uptake, reinforce recent momentum but do not eliminate the major short-term risk of potential gross-to-net headwinds from contracting and reimbursement changes, which could still pressure net margins. Investors still need to keep a close eye on patient access barriers and how payer dynamics might evolve over the coming quarters.

Among recent announcements, the initiation of Phase III programs, including for NBI-'568 targeting schizophrenia, highlights Neurocrine’s ongoing investment in research and development. The success or challenges of these late-stage trials remain a key long-term catalyst, as new approvals could diversify revenue streams and offset competitive or reimbursement risks faced by core products.

Yet in contrast to the positive quarterly numbers, investors should not overlook how evolving payer requirements and reauthorization processes could challenge future revenue...

Read the full narrative on Neurocrine Biosciences (it's free!)

Neurocrine Biosciences' outlook anticipates $3.6 billion in revenue and $842.9 million in earnings by 2028. This is based on an assumed annual revenue growth rate of 13.9% and a $537.1 million increase in earnings from the current $305.8 million.

Uncover how Neurocrine Biosciences' forecasts yield a $163.76 fair value, a 27% upside to its current price.

Exploring Other Perspectives

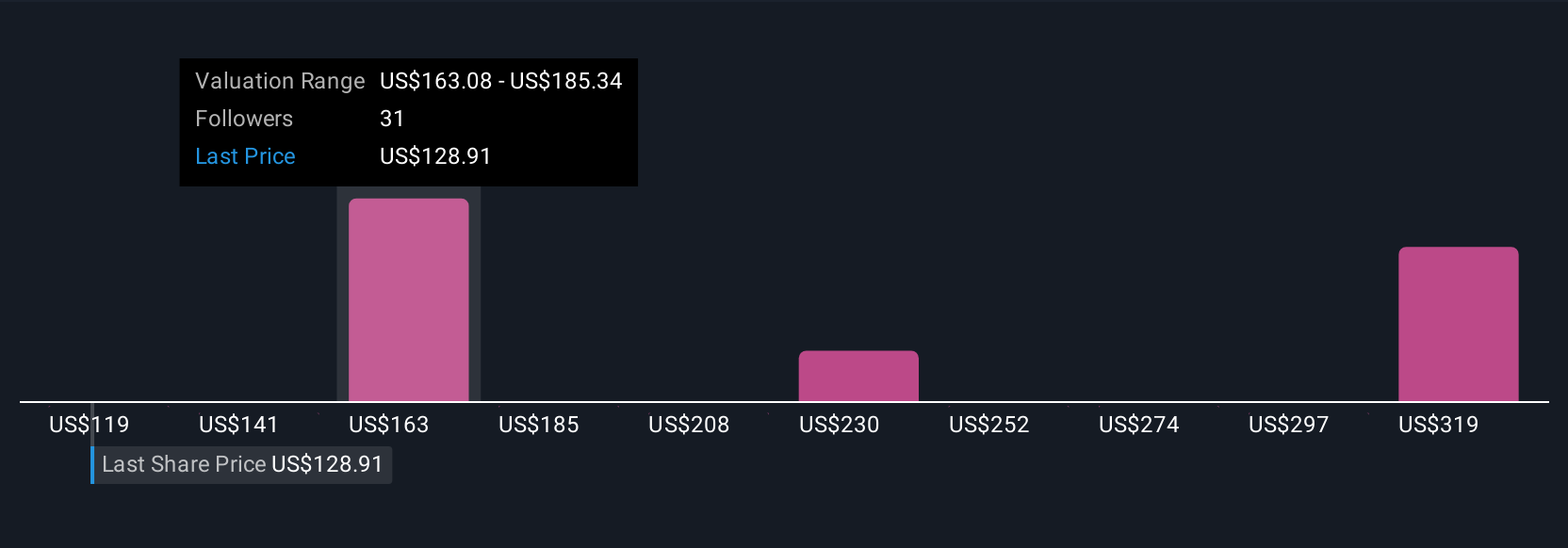

Fair value estimates from seven Simply Wall St Community members range from US$119 to US$341 per share. Many are focused on how expanded reimbursement coverage for key products could impact future expectations, these diverse views offer a look at the different ways you might assess the company’s prospects.

Explore 7 other fair value estimates on Neurocrine Biosciences - why the stock might be worth over 2x more than the current price!

Build Your Own Neurocrine Biosciences Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Neurocrine Biosciences research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Neurocrine Biosciences research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Neurocrine Biosciences' overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Neurocrine Biosciences might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10