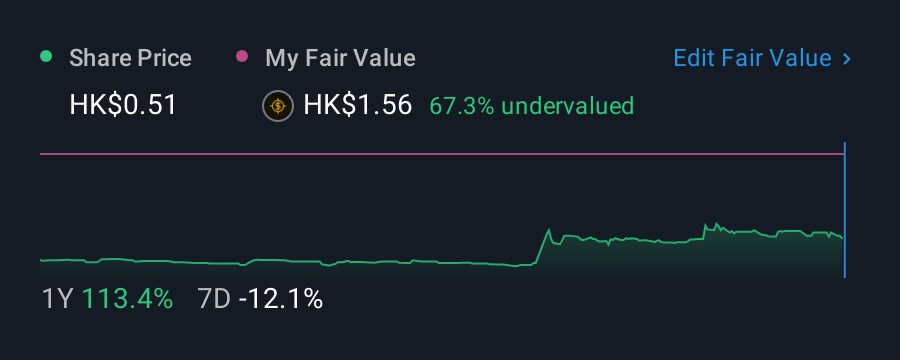

Most readers would already be aware that REF Holdings' (HKG:1631) stock increased significantly by 22% over the past three months. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Specifically, we decided to study REF Holdings' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for REF Holdings is:

7.1% = HK$5.7m ÷ HK$80m (Based on the trailing twelve months to December 2024).

The 'return' is the profit over the last twelve months. That means that for every HK$1 worth of shareholders' equity, the company generated HK$0.07 in profit.

View our latest analysis for REF Holdings

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of REF Holdings' Earnings Growth And 7.1% ROE

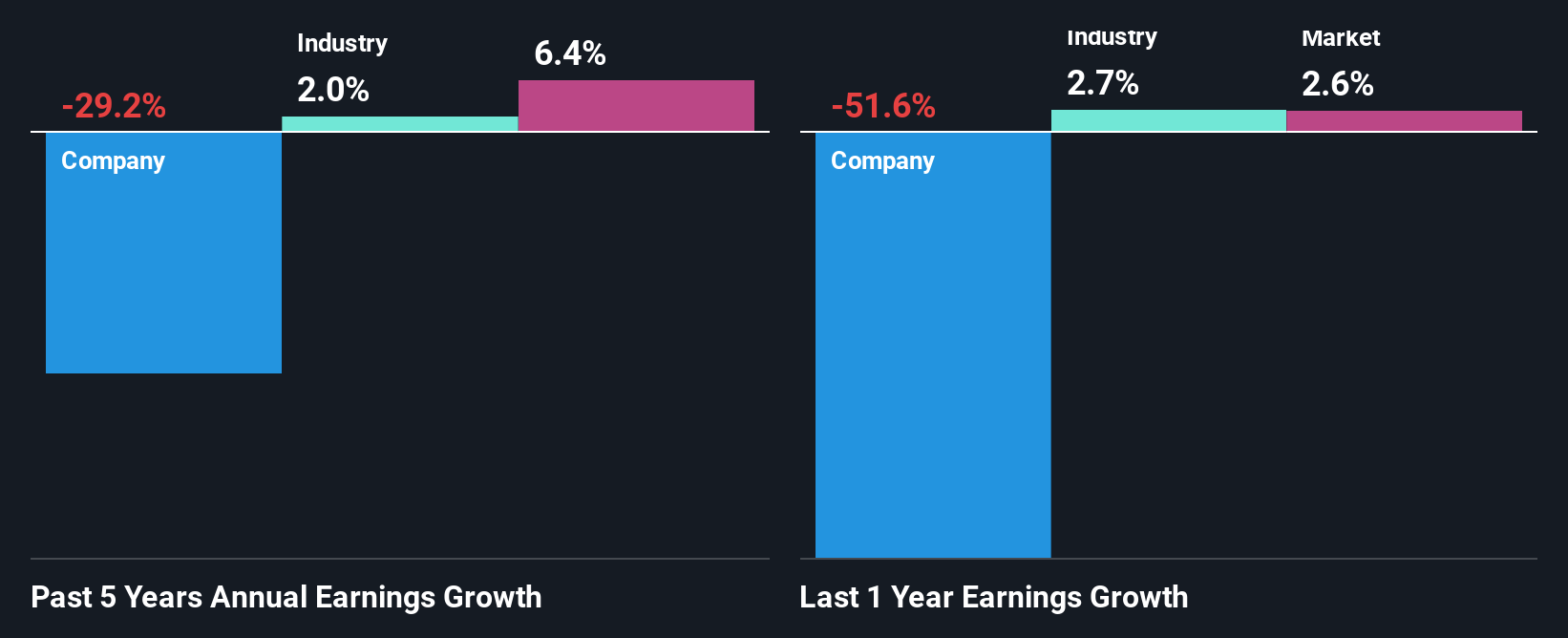

On the face of it, REF Holdings' ROE is not much to talk about. Yet, a closer study shows that the company's ROE is similar to the industry average of 7.4%. But REF Holdings saw a five year net income decline of 29% over the past five years. Bear in mind, the company does have a slightly low ROE. Therefore, the decline in earnings could also be the result of this.

So, as a next step, we compared REF Holdings' performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 2.0% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is REF Holdings fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is REF Holdings Efficiently Re-investing Its Profits?

While the company did payout a portion of its dividend in the past, it currently doesn't pay a regular dividend. This implies that potentially all of its profits are being reinvested in the business.

Conclusion

In total, we're a bit ambivalent about REF Holdings' performance. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. Up till now, we've only made a short study of the company's growth data. So it may be worth checking this free detailed graph of REF Holdings' past earnings, as well as revenue and cash flows to get a deeper insight into the company's performance.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.