How Corcept's Earnings Beat and Buyback Expansion Could Shape Investor Expectations for CORT

- In the past week, Corcept Therapeutics reported second quarter 2025 earnings with net income of US$35.15 million and revised its full-year revenue guidance to between US$850 million and US$900 million, reflecting improved vendor performance and an additional pharmacy coming online.

- The company also advanced its share buyback program, repurchasing 1,482,000 shares for US$103.04 million during the quarter, indicating ongoing confidence in its capital management strategy.

- We'll consider how Corcept's updated revenue guidance and operational improvements could influence the company's investment narrative and future growth outlook.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Corcept Therapeutics Investment Narrative Recap

At its core, being a Corcept Therapeutics shareholder means you believe in the company's ability to diversify beyond heavy reliance on Korlym by launching new products and expanding its patient base. The latest quarterly earnings and revised revenue guidance, reflecting improved pharmacy operations, do not materially alter the near-term catalyst, which remains the successful regulatory outcome and launch of relacorilant; however, the primary risk continues to be the potential for accelerated generic erosion of Korlym revenues should ongoing patent litigation not favor Corcept. Among recent company news, Corcept's revised 2025 revenue guidance to US$850 million–US$900 million is particularly relevant, as it reflects tangible progress in scaling commercial infrastructure and easing prior fulfillment bottlenecks. This addresses a key operational risk, boosting confidence that near-term revenue goals can be supported by better pharmacy vendor performance and enhanced distribution. By contrast, investors should be aware that ongoing legal uncertainties around Korlym’s intellectual property could still...

Read the full narrative on Corcept Therapeutics (it's free!)

Corcept Therapeutics' narrative projects $2.0 billion revenue and $903.7 million earnings by 2028. This requires 40.7% yearly revenue growth and a $771.7 million earnings increase from $132.0 million.

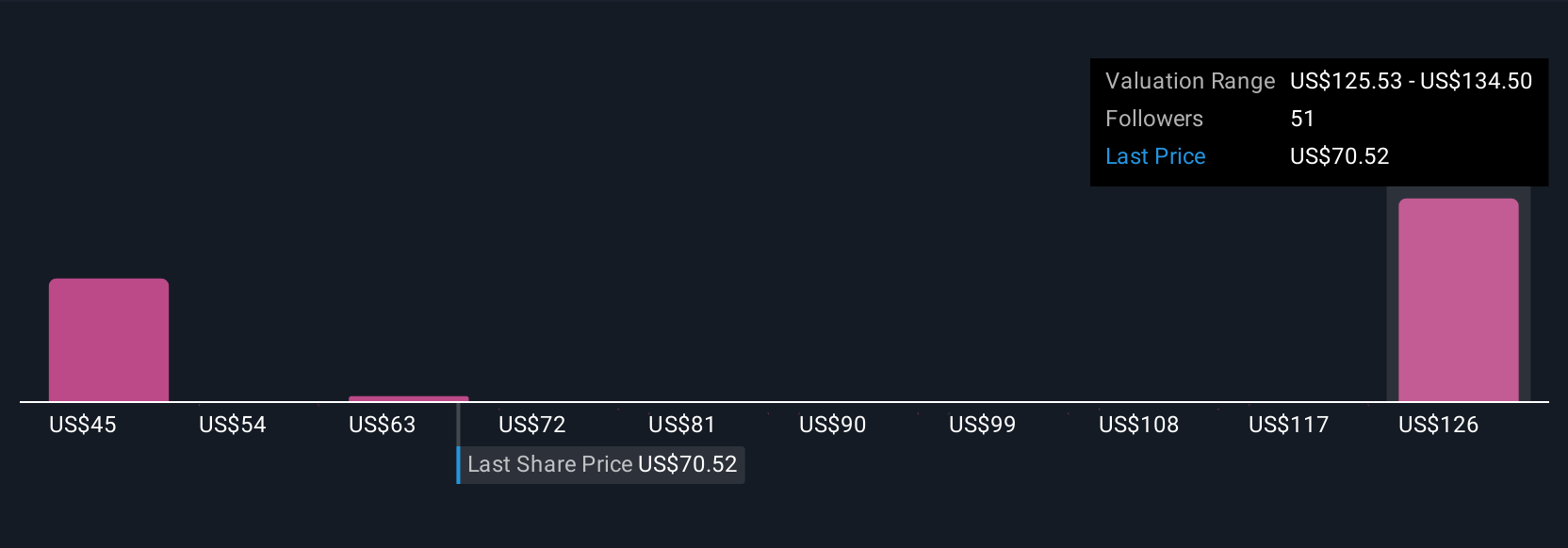

Uncover how Corcept Therapeutics' forecasts yield a $134.50 fair value, a 86% upside to its current price.

Exploring Other Perspectives

Ten fair value estimates from the Simply Wall St Community cluster between US$44.83 and US$134.50 per share, showing a spread of opinions on Corcept’s outlook. Yet your own perspective may shift as you consider persistent risks from heavy Korlym dependence and how they may affect future performance, explore several alternative viewpoints to see why market views diverge this widely.

Explore 10 other fair value estimates on Corcept Therapeutics - why the stock might be worth as much as 86% more than the current price!

Build Your Own Corcept Therapeutics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Corcept Therapeutics research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Corcept Therapeutics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Corcept Therapeutics' overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10