Cellebrite (CLBT) Is Up 10.6% After Return to Profitability and CEO Appointment Has the Bull Case Changed?

- Cellebrite DI reported its second quarter 2025 results, posting US$113.28 million in revenue, a return to net profitability, and appointed Thomas E. Hogan as permanent CEO after serving in an interim capacity.

- The shift to sustained profitability, higher full-year revenue guidance, and confirmed executive leadership mark a significant moment in Cellebrite’s recent transformation.

- We’ll assess how the company’s return to net profitability and leadership stability may reshape Cellebrite’s investment outlook.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

Cellebrite DI Investment Narrative Recap

To own a stake in Cellebrite DI, you need to believe that accelerating demand for digital investigation tools will translate into ongoing subscription revenue growth and strong recurring cash flows. The company’s return to net profitability and upgraded full-year revenue guidance provide a potential catalyst for sentiment, but over-reliance on U.S. federal government contracts remains the biggest risk to consistent growth; although management’s recent results are encouraging, the impact on addressing contract delays or customer concentration is not yet material.

Among recent announcements, Cellebrite’s confirmed guidance for full-year 2025 revenue between US$465 million and US$475 million gives investors a concrete view into the company’s short-term growth trajectory. This is relevant given that visibility into government contract timing remains limited, meaning actual results may still fluctuate around these projections.

By contrast, investors should not lose sight of the ongoing federal procurement delays that continue to affect Cellebrite’s revenue visibility and near-term ARR performance...

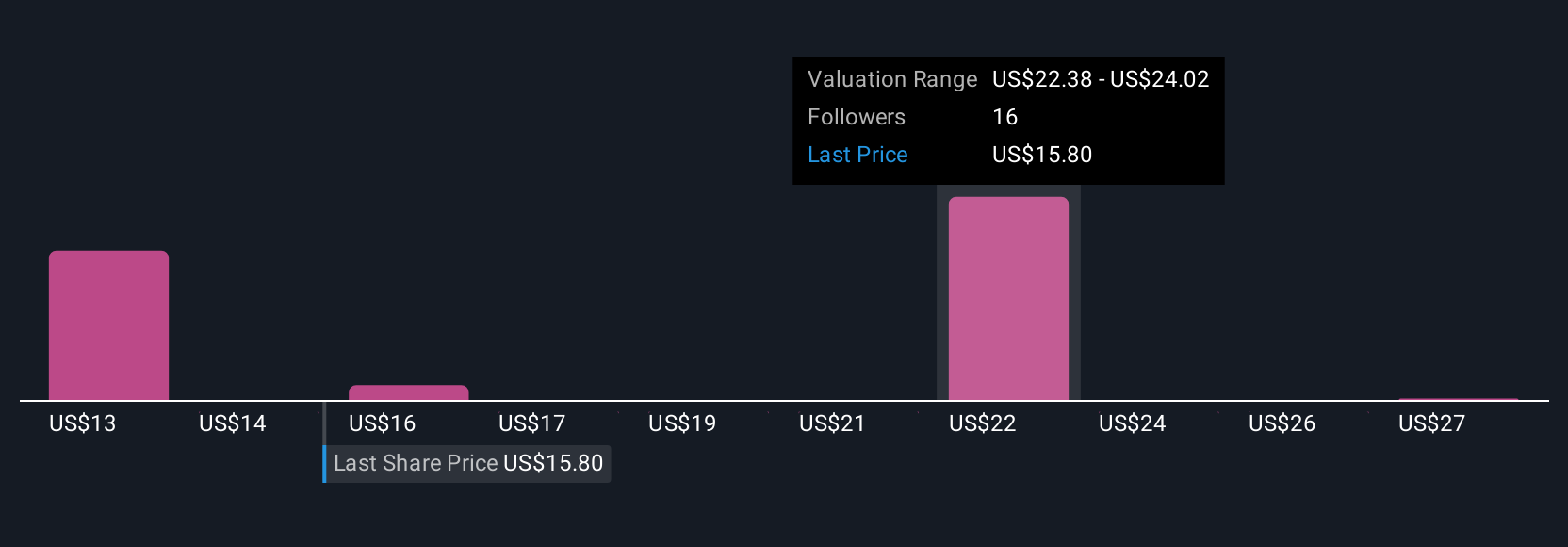

Read the full narrative on Cellebrite DI (it's free!)

Cellebrite DI's narrative projects $676.2 million revenue and $127.6 million earnings by 2028. This requires 15.7% yearly revenue growth and a $278.5 million increase in earnings from -$150.9 million currently.

Uncover how Cellebrite DI's forecasts yield a $23.00 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Five Simply Wall St Community estimates place Cellebrite’s fair value between US$12.75 and US$28.93 per share. While recent profitability and revenue momentum provide optimism, persistent risks from client concentration mean opinions will continue to vary widely.

Explore 5 other fair value estimates on Cellebrite DI - why the stock might be worth as much as 89% more than the current price!

Build Your Own Cellebrite DI Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cellebrite DI research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cellebrite DI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cellebrite DI's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10